This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

.” SNC (pronounced like the candy bar but without the “ers”) stands for the Shared National Credit Program, which, since 1977, has assessed risk in the largest and most complex credits shared by multiple regulated financial institutions. Loan reviews are completed in the first and third calendar quarters each year.

The FDIC released a manual on Formal and Informal Enforcement Actions. The FDIC released its manual on Formal and Informal Enforcement Actions. For the first time, the FDIC released its manual on Formal and Informal Enforcement Actions to provide greater transparency to those processes. Key Takeaways.

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. Office of the Comptroller of the Currency (OCC). Cybersecurity.

This month, the Federal Deposit Insurance Corporation (FDIC) launches it new Banker Engagement Site (BES) through FDIC connect. Already reviewed by Perficient, BES provides a secure and efficient portal to exchange documents, information, and communications for consumer compliance and Community Reinvestment Act (CRA) examinations.

In various press releases, the Federal Deposit Insurance Corporation (FDIC) has highlighted that an estimated $16.3 Despite this proactive approach, federal banking regulators either neglected to review the same documents or did so without taking necessary action before the bank failed.

The FDIC has announced that it has entered into a settlement of the lawsuit filed against it and the OCC in 2014 by a trade group and several payday lenders challenging “Operation Choke Point” — a federal enforcement initiative involving the FDIC, OCC and other federal agencies. In July 2017, the D.C.

Regulators expect an institution to maintain a quality control program for AML activities, said Josh Hawkins, Director of Abrigo’s Financial Crimes Unit. Before MidCountry Bank implemented BAM+ AML software , it was using folders on the network, grabbing screenshots, managing Excel documents, and writing lengthy reports for due diligence.

The first decision a community bank must make in choosing a hedging program is if they will subject their commercial customers to ISDA documents. Most community banks do not have a large universe of customers and prospects that would embrace complex and esoteric documentation.

To that end, and as reported by BuzzFeed , documents submitted by banks to the U.S. The documents, officially known as suspicious activity reports (SARs for short) show that the banks had filed more than 2,000 reports across the past 17 years. In one example, reported on Monday (Sept. billion in fines.

Meet Model Risk Management Expectations Updates to the FDIC Risk Management Manual should steer institutions toward a model that manages risk and drives growth. FDIC Update. Last April, the FDIC released an Interagency Statement titled Model Risk Management (MRM) for Bank Models and Systems Supporting BSA/AML Compliance.

Earlier this year, the Office of the Comptroller of the Currency (OCC), the Board of Governors of the Federal Reserve System (Fed), and the Federal Deposit Insurance Corporation (FDIC) unveiled a proposed rule that would reshape the landscape for certain financial institutions. Learn More: U.S.

On July 25, 2022, the FDIC issued Financial Institution Letter (FIL)-34-2022 announcing updates to Chapters 1 and 4 of its Formal and Informal Enforcement Actions Manual (Manual). The Manual includes updates to the minimum standards for the FDIC’s termination of cease-and-desist and consent orders.

This document was also written for examiners and recognizes the exam burden for financial institutions. The guidance emphasizes a risk-focused approach to examinations and refocuses the regulators to scope each exam according to the unique financial institution, not to use a one-size-fits-all approach. 6 Critical Areas. Calibration.

The better prepared, the less likely they are to run afoul of the continually shifting regulations. Regulators and industry consultants agree that community banks are generally doing a great job handling their regulatory oversight and requirements. Be aware of existing or emerging risk concerns. in Kent, Ohio.

The Scaled CECL Allowance for Losses Estimator (SCALE) tool was unveiled during an “Ask the Fed” webinar , where regulators described the Excel spreadsheet-based option using estimated loss rates from peers as a “ starting point ” in the calculation. NCUA officials were not included in the SC ALE webinar. “The

Takeaway 2 Regulators say management should periodically validate the loss estimation process for the allowance for credit losses (ACL) and any changes to it. Regulators have noted such risks can involve financial losses, poor business and strategic decision-making, or damage to a bank’s reputation.

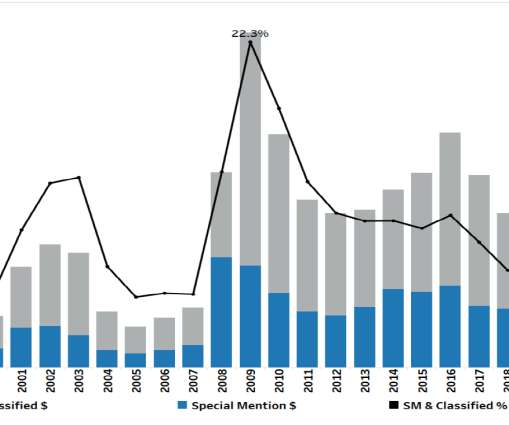

Ashbaugh’s presentation begins with a quick summary of why regulators care about HVCRE. That 13% represented 80% of the losses to the FDIC insurance fund. The regulators want to make sure you have all your ducks in a row, that you have more capital applied to those loans, and you have processes to identify those loans”.

Takeaway 1 Signs point to increased loan modifications and loan workouts, and regulators have urged financial institutions to work prudently with borrowers. . Meanwhile, regulators are focusing fresh attention on prudent credit risk management of loans, especially CRE, and loan modifications in general. CRE loan accommodations.

Many Chief Appraisers are dealing with FDIC auditors camped out in their office. The regulators are digging deep, very deep. The demands for meticulous documentation, clear communication trails and absolute compliance with regulatory standards can be overwhelming.

Independent Loan Review Systems in Banking Banking regulators have outlined expectations for effective, independent loan review and credit risk review. . The change reflects regulators’ expectations that financial institutions will develop loan review or credit review systems tailored to their specific risks and circumstances.

Navigating interest rate management in today's environment As regulators focus on interest rate risk management, read about what financial institutions can do to be ready for a rate drop. You might also like this on-demand webinar, "Navigating uncertain times: Strategies for effective risk management and compliance."

We have been following closely efforts by state regulators, state legislatures and the courts to restrict, or in some cases prohibit, bank model lending programs, so the recent guidance from the Vermont Department of Financial Regulation (“Department”) is welcome news.

Some CECL consultants can provide financial institutions with the model and initial allowance calculation, including documentation of the decision and backtesting. It can also reduce the time spent on documenting decisions and report writing. Prepare documentation—policies and procedures—as you go. CECL Regulation.

Recently, the federal banking regulators issued four new sets of examination procedures. The booklet contains examination procedures regarding supervision of OCC-regulated banks and savings associations related to Section 5 of the Federal Trade Commission Act (“UDAP”) and Sections 1031 and 1036 of the Dodd-Frank Act (“UDAAP”).

19) announcement, the company said the application is with the Federal Deposit Insurance Corporation (FDIC). Regulators had said a refiling would be permitted. Regulators had said a refiling would be permitted. In its Wednesday (Dec. The application is for a special industrial loan company license.

On fire were documents requested by the Texas Department of Banking (TDB). She hid them from the Board and regulators with assistance from unnamed co-conspirators." When the TDB shut them down and the FDIC investigators came in, they had to occupy the church next door because of the smell from the fire. Well, not actually Pat.

As the FDIC said recently: Exceptions to policy should be few in number and properly justified, approved, and tracked. 3 categories of credit exceptions I would divide exceptions into three categories: structural credit exceptions, account management exceptions, and documentation exceptions. and property tax payments.

The CFPB, OCC, Federal Reserve, FDIC, and NCUA have issued a proposed rule on the role of supervisory guidance. The proposed rule would codify the Statement, with clarifying changes, as an appendix to a new subpart added to the regulations of each agency.

The DBO’s press release stated that it issued a subpoena to LoanMart requesting financial information, emails, and other documents “relating to the genesis and parameters” of its arrangement with CCBank. Thus, both the OCC and FDIC have adopted regulations rejecting the Second Circuit’s Madden decision.

Community banks and the entire banking industry face downside risks from inflation, rising market interest rates, and continued geopolitical uncertainty, the FDIC said recently in its quarterly report. Abrigo Solutions Make better decisions amid uncertainty Respond quickly and efficiently to the needs of customers.

And while the points of friction are myriad — and have been documented, in all their colorful wonder, across the pages of PYMNTS in 2016 — there seems to be one thing that everyone involved in the debate agrees on, and that is The Pew Charitable Trusts’ numbers. And that the CFPB can fix — narrowly.

Following a pattern established under former Director Cordray, the CFPB used relatively neutral language in its formal documents and more aggressive language in its press release, leaving the most alarming comments for the Director to personally deliver.

We get the disclosure back faster” when borrowers digitally sign documents exchanged by email, Webster notes. Community banks and their customers don’t need to be concerned about the legality of digitally signed documents. Sending documents to a consumer’s personal email is the first safeguard.

s cybersecurity practices has accused the agency of accessing internal documents from the FDIC's inspector general. A House committee probing the Federal Deposit Insurance Corp.'s

Newly unsealed court documents make clear that regulators forced banks to terminate relationships with payday lenders and other lawful businesses, setting a dangerous precedent.

The FDIC , Federal Reserve Board and Comptroller of the Currency are proposing a rule to implement a rural property appraisal exemption under the Economic Growth, Regulatory Relief, and Consumer Protection Act (the Act) and also increase the appraisal exemption based on transaction value from $250,000 to $400,000.

The exemption based on a transaction value of $400,000 or less is available for residential real estate transactions, which is defined as a real estate-related financial transaction that is secured by a single 1-to-4 family residential property.

According to the complaint, in 2020 and 2021, OppFi provided documents to the DFPI in response to the DFPI’s request for information relating to its partnership with the Bank. While non-bank participants have been the focus of these state attacks, bank participants could also face increased scrutiny from their regulators.

The CID requests the production of documents and answers to written questions related to our Venmo service. Venmo also finds itself in the company of digital and mobile-based financial services firms that caught the officially eye of regulators last week. We are cooperating with the FTC in connection with the CID.”.

The Plan for Prosperity is a flexible, living document that can be adapted to a rapidly changing regulatory and legislative environment to maximize its influence and likelihood of enactment. FDIC Assessment Rules. Here’s an outline of the key activities ICBA’s advocacy team in Washington, D.C., Washington Policy Summit.

ED also stated that it “will monitor compliance and take corrective action to enforce these regulations when necessary.”. The cash management rules generally require IHEs to review college banking agreements to ensure that the terms offered to students “are not inconsistent with the best financial interests of students opening them.”

The agencies are the Comptroller of the Currency, Farm Credit Administration, FDIC, Federal Reserve Board, and National Credit Union Administration (Agencies). The Agencies note that they plan to publish in the Federal Register a final document based on the new proposed Q&As and the Q&As proposed in July of 2020.

The OCC describes the underwriting standards and loan documentation policies and procedures that the OCC expects a bank to have. Previously, Acting Comptroller of the Currency Brian Brooks indicated that the OCC expected to partner with the FDIC in developing the OCC’s “true lender” rule.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content