This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

These tactics cast a wide net of fraud over the fleet card industry – from issuers and acquirers to fleet managers, employers and employees themselves. Goldspink recently told PYMNTS that fleet card-related fraud goes far beyond skimmers at the POS.

Here, Machicao explains how his firm helped clients protect themselves from escalating fraud risks with the COVID-triggered wave of CNP payments. The payment and fraud landscape is almost unrecognizable today compared to just a few short months ago. The following is an excerpt from What Did You Change?

There’s another way, though, in which the fear of fraud bears down on the enterprise. A new report from Vesta Corporation finds fraud positions itself in the way of innovation and growth, even compliance. to understand how payments fraud is limiting corporates’ path to success. cents per every $100 transacted.

Receivable Savvy, an accounts receivable and order-to-cash management firm, wants suppliers to see Same Day ACH as an opportunity to bolster cash flow. The company, which provides education and resources for suppliers, recently released a new eBook to guide vendors on how to take advantage of Same Day ACH technology.

PYMNTS consulted 21 payments executives from across the industry to share their insights on the biggest takeaways from 2016 as part of the “Payments 2016, The Year Of…” eBook. At the transaction level, consumers began to feel like they were more protected from fraud with the introduction of the EMV chip card. Download the eBook.

During the webinar, McLaughlin explained that the two biggest challenges for audit firms lie within the tension of managing risk while creating more efficiency during the audit process. The goal is to do less work while managing an appropriate level of risk. The goal is to do less work while managing an appropriate level of risk.

A new independent survey by research firm Ovum has found that banks in multiple regions plan to integrate their fraud and financial crime compliance systems and activities in response to new criminal threats and punishing fines — but not all at the same speed. said TJ Horan, vice president of fraud solutions at FICO. South Africa.

PYMNTS consulted 21 payments executives from across the industry to share their insights on the biggest takeaways from 2016 as part of the “Payments 2016, The Year Of…” eBook. Here is the response from Steven Cole, Senior Product Manager, EMV, Vantiv … Payments 2016: The Year Of The Chip. Download the eBook.

FICO published our 2021 Digital Consumer Banking and Fraud Survey today that emphasizes consumer perspectives on customer experience and fraud prevention management. . US customers and their banks are familiar with different types of fraud including card, identity, and payment related frauds.

FICO published our 2021 Digital Consumer Banking and Fraud Survey today that emphasizes consumer perspectives on customer experience and fraud prevention management. . US customers and their banks are familiar with different types of fraud including card, identity, and payment related frauds.

We’ve created a platform that offers flexibility in order management and billing," he explains. We’ve created a platform that offers flexibility in order management and billing. Brian Bogosian, CEO of sticky.io, recounts the initiatives his firm has embraced to help merchants overcome their challenges.

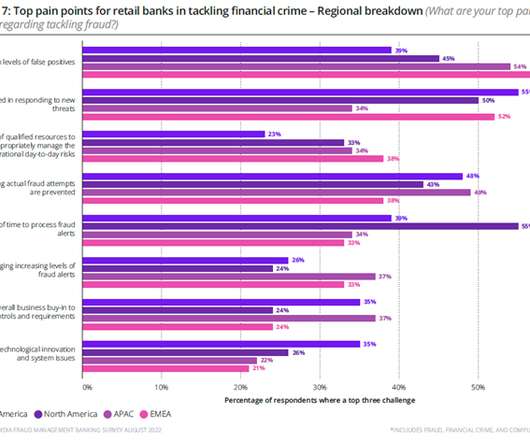

Enterprise Fraud Solution Buyers Want More Agility, More Data. Our recent global survey reveals the investment priorities and functionality requirements for enterprise-level fraud solution buyers. In August 2022, we commissioned a survey of 156 global executives and managers from retail banks and retail financial institutions.

The last few years have thrown up many challenges for banks and card providers as everything has shifted online, one of the primary challenges being fraud scams. But the online shift has also created opportunities for financial institutions to demonstrate their strong fraud controls in the digital space.

PYMNTS consulted 21 payments executives from across the industry to share their insights on the biggest takeaways from 2016 as part of the “Payments 2016, The Year Of…” eBook. FinTechs looking to displace FIs also, I believe, underestimated that change in how consumers manage, save and spend their money is evolutionary, not revolutionary.

Retailers are] seeing it not just as a process to be managed, but as an opportunity. As goes digital commerce, so goes fraud. The right platform will allow them to combine layers of security — like tokenization, biometric authentication, PINs and back-end fraudmanagement — to achieve the right balance of security and usability.

But as procurement become automated and accelerated, industry experts at eProcurement and spend management software company eRequester say it must also be transparent. In its eBook, eRequester said that procurement visibility is paramount to cutting back on those financial losses.

I’ve been writing recently about the results of our recent global consumer fraud survey. But like most things, it’s not as simple as it sounds, as large customer groups are likely to switch banks if they are dissatisfied with their response to a fraudmanagement incident (more on that in a moment). What’s a bank to do?

Strong Fraud Protection Could Draw More Customers - Survey. Fraud protection is now firmly on the radar for consumers and has risen substantially as a deciding factor - it could even be a competitive advantage for banks. In the UK, trade bodies have called for fraud levels to be considered a national security threat.

PYMNTS consulted 21 payments executives from across the industry to share their insights on the biggest takeaways from 2016 as part of the “Payments 2016, The Year Of…” eBook. Here is the response from Sarah Clark, general manager, identity, Mitek … Payments 2016: The Year Mobile, Biometrics And Trust Converged.

Consumer habits have shifted to online shopping for goods and services and the impact for merchant acquirers is the need for faster onboarding of new merchants and effective ongoing monitoring to minimise fraud and compliance risk. Digital automation can enable a process to underwrite a new merchant in just minutes rather than days.

UK consumer fraud attitudes. You can read more about all the UK survey results in our Digital Consumer Banking and Fraud Survey – UK Results Ebook . Banks also have the opportunity to improve fraud response efforts. Millennials are the least impressed. Millennials are the least impressed.

contributed by John Owens , senior vice president and general manager of Elan Financial Services. In addition, we developed an array of new DIY servicing capabilities, including enhanced functionality to facilitate payments, report fraud and send past-due notifications. The following is an excerpt from What Did You Change?

Here are a few examples of capabilities that enable our clients to manage unforeseen circumstances related to payments: Clearing options: Providing two or more local clearing options in each major region ensures redundancy if one bank partner is disrupted. Our clients’ payers have been the subject of different phishing and fraud attempts.

Increasing collaboration promises to help with that task, according to a recent PYMNTS interview with Director of Compliance and Interoperability Kevin Emery at UL , which helps other companies with identity management and security-related issues.

Last year we published a highly successful The 11 Commandments of Digital Banking eBook that introduced the 11 commandments: Digital lift-and-shift is not a strategy! In fact, thoughtfully designed points of friction can be extremely valuable for managing risk and making customers feel safe. Friction – not inherently good or evil.

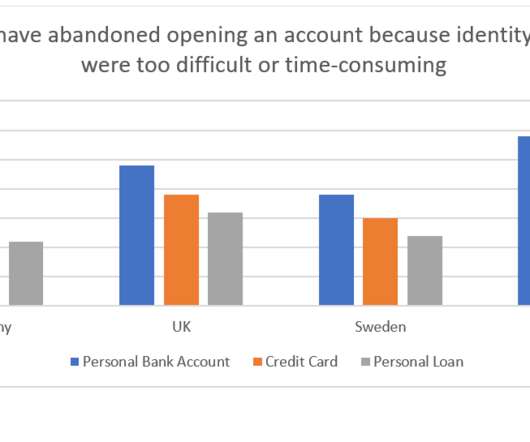

Identity verification, required to prevent fraud and meet eKYC regulatory requirements, can also be the one that introduces friction and causes customers to abandon applications. For more information on this survey, watch our webinar on Customer Identity Management – Are You Digital Enough for Your Customers ? by Sarah Rutherford.

The customer communication solutions that financial services partners provide must offer best-in-class technology, with easy implementation, ongoing management and ultimately tangible results. Digital communications options vary across the customer lifecycle, whether it’s for onboarding, account notifications, fraud alerts, or collections.

With ambitious goals to open up banking and decimate fraud, PSD2 has taken a long time to deliver, and we’re not quite there yet. For more information, see our ebook on the survey and www.fico.com/authentication. And perhaps more importantly, are their customers? by Sarah Rutherford.

Following the highly successful The 11 Commandments of Digital Banking eBook , we are publishing a series of 5 deeper dive blog posts that group the 11 Commandments below into common themes: Digital lift-and-shift is not a strategy! Make alerts to suspected fraud fast and appropriate. Friction – not inherently good or evil.

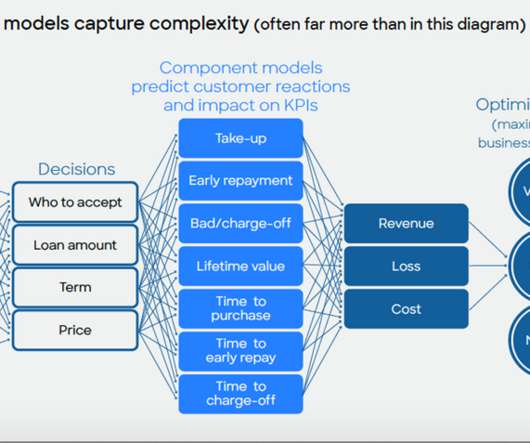

His insights on humanizing interactions come from his larger piece on digital banking called The 11 Commandments of Digital Banking eBook. Here is an excerpt of his top ranking post: Credit limit management is regarded as a key driver to profitable portfolios.

With ambitious goals to open up banking and decimate fraud, PSD2 has taken a long time to deliver, and we’re not quite there yet. For more information, see our ebook on the survey and www.fico.com/authentication. And perhaps more importantly, are their customers? by Sarah Rutherford.

Following the highly successful The 11 Commandments of Digital Banking eBook , we are kicking off a series of 5 deeper dive blog posts that group the 11 commandments below into common themes. Ensure that your fraud and risk management processes aren’t forcing them to visit. Digital lift-and-shift is not a strategy!

Following the highly successful The 11 Commandments of Digital Banking eBook , we are completing our series of 5 deeper dive blog posts that group the 11 Commandments below into common themes: Digital lift-and-shift is not a strategy! Everyone thinks they own the customer – from marketing and fraud, to servicing, product, and collections.

.” “We have not seen a direct effect [from Airbnb] in any of our hotels … We don’t feel it’s having any impact on our results or that it has hit our radar as of yet,” said Richard Jones, senior VP and COO of Hospitality Ventures Management Group, in 2014. Robo-advisors. But some finance professionals are not believers. ” 16.

.” “We have not seen a direct effect [from Airbnb] in any of our hotels … We don’t feel it’s having any impact on our results or that it has hit our radar as of yet,” said Richard Jones, senior VP and COO of Hospitality Ventures Management Group, in 2014. Robo-advisors. But some finance professionals are not believers. ” 14.

Twenty months of my absence have allowed the “professional” top managers to kill the company using the money of rich oligarchs. Note: Less than a month after the closure announcement, Vasupal was arrested for fraud in a bizarre case involving Stayzilla business dealings. Title: All Romance eBooks is Shutting Down.

Signed deal with Vision FCU to provide its money management app. Partnered with fellow Finovate alum NCR to launch new money management platform. Powered Homeownership Preservation Foundation’s digital money management app. Offered digital wealth management for BancAlliance Member Banks. Hired former Yodlee CFO.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content