This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Regulators expect an institution to maintain a quality control program for AML activities, said Josh Hawkins, Director of Abrigo’s Financial Crimes Unit. Simply hiring more staff isn’t always the best solution or one that is necessarily welcomed by leadership, especially given pressures to restrain non-interest income expenses.

The gen AI consultant can talk intelligently about leadership, bank performance, financial structuring, marketing, lending, legal, compliance, and deposits. Because of the newness in the technology and the newness of bankers dealing with technology, caution should always be exercised.

Start with these seven key takeaways: Recognize phishing attempts: Clients should understand common tactics used in phishing and exercise caution with emails by checking the sender’s address for anything unusual. What should a financial institution’s fraud education program include?

It’s very hard for regulated banks and credit unions to gain any meaningful efficiencies under $1 billion in assets. An exercise Cornerstone likes to conduct: Take a look at the top 20% of the bank’s headcount and review comp and bonus in descending order. It appears nothing else matters but the urgency to get big and get there fast.

Technology Stack: Flask, SQLAlchemy, Bootstrap, ForeignKeys, Jinja | APIs Used: Used data from “California regulations of possibly harmful products”, which was a CSV file. More About Christina Babaya’s Bright Paths Project: Comparing Cosmetic Products by Ingredients. Bright Paths Project: Welcome to Stock Market.

By 2017, 1 st Alliance’s compliance department began to raise concerns to company leadership, including the individual defendants, that SCs were engaging in activities that would require licensing. The duties performed by the SCs/HLCs required them to hold a mortgage originator license in every state in which 1 st Alliance operated.

They may be looking for a dance partner or hiding from a regulator. However, a lack of solid earnings trends leads to bad things when shareholders, board members and regulators begin to express their concerns and potentially disrupt the direction of the institution. 25% 140 banks will have capital levels that have fallen below 8%.

In our blog post about the survey , we commented that the CFPB’s current leadership would likely attempt to use the survey to justify the CFPB’s current regulatory focus and lay the groundwork for future enforcement and rulemaking priorities.

He also recommends not updating the resiliency document as only a “table-top exercise.” Grandstrand, who specializes in bank regulation, notes that it’s important to distinguish between shareholder meetings at the holding company level and at the bank level, as different statutes and regulations may apply. Quick Stat.

The Taskforce was charged with examining the existing legal and regulatory environment for consumers and financial services providers and making recommendations to the Bureau’s leadership for improving consumer financial laws and regulations. The report consists of two volumes. Equal access to credit.

Although issued under Director Kraninger’s leadership, the Winter 2019 Supervisory Highlights covers examinations generally completed between June and November 2018 when Mick Mulvaney was Acting Director. It represents the CFPB’s second Supervisory Highlights covering supervisory activities conducted under Mr. Mulvaney’s leadership.

The Consumer Finance Protection Bureau suffered a major blow in Federal Appeals Court yesterday when a three judge panel ruled that parts of its leadership structure are unconstitutional. Most likely, most experts agree, the CFPB will appeal the ruling — probably exercising its option of asking the D.C.

Because it had ruled that the CFPB’s leadership structure was constitutional, the Ninth Circuit had not previously considered the CFPB’s argument that former Acting Director Mulvaney’s ratification of the CID issued to Seila Law cured any constitutional deficiency. All American Check Cashing.

He exemplifies the best of next generation bank leadership, with eyes wide open to the next iteration of banking in our rapidly changing environment. It covers all the CAMELS components the regulators grade banks on. One of my tweeps (Twitter friends), is Andy Schornack, CEO of Flagship Bank Minnesota, based in Wayzata.

Data leaders know that they are solving business problems and need to prescribe the data required to solve the problem, rather than hope that some Big Data Exercise will help find nuggets of greatness. (As As I noted in the Information Age article, this will be even more important under Europe’s GDPR regulation.).

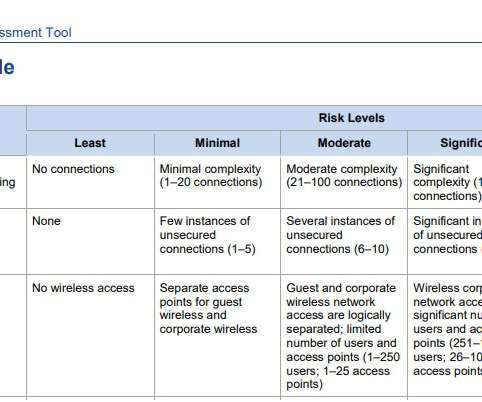

As these have attacks have evolved, regulatory bodies have updated their regulations to account for the increasing threat of cyber risk. This was revised in 2017, and this consistent framework is intended to be able to help leadership and the board assess their preparedness and risk over time.

Under my leadership, the FDIC’s oversight responsibilities will be exercised based on our laws and our regulations, not personal or political beliefs,” she concluded. As we’ve noted in earlier posts on this , litigation is currently pending in the D.C.

It’s almost as bad as saying it’s the “Year of The Sloth” – since, let’s face it, pigs are not typically prized for their wisdom, energy, vision or leadership qualities across the animal kingdom. Wearables – watches, shoes and clothing – can alert users to the need to replace them while providing tips on diet and exercise.

Cybersecurity advice for financial institution leaders CISA’s “Shields Up” program also offers advice for corporate leadership, and much of that advice applies to financial institution governance. Exercise continuity plans Know your plan of action should a system experience downtime due to a DDoS attack. BSA Rules and Regulation.

Key takeaways regarding the implications of a blue wave scenario include the following: Chris Willis commented that the CFPB’s approach to the exercise of its authorities is likely to reflect criticism by Democrats that the CFPB has been lax in its approach to industry under Director Kraninger’s leadership. (In

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content