This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The FDIC released a manual on Formal and Informal Enforcement Actions. The FDIC released its manual on Formal and Informal Enforcement Actions. For the first time, the FDIC released its manual on Formal and Informal Enforcement Actions to provide greater transparency to those processes. Key Takeaways.

Since that blog was published, the FDIC has issued an update on its Restoration Plan for the Deposit Insurance Fund (DIF). The Federal Deposit Insurance Act (FDI Act) requires the FDIC Board to adopt a restoration plan when the DIF’s reserve ratio—the ratio of the fund balance relative to insured deposits—falls below 1.35

FDIC) is considering nixing its quarterly reports of banks in an attempt to modernize the way data is handled. To do so, the FDIC is going about a new competition among 20 data and technology firms to try and find the best way to move forward, WSJ reported. Recently, the FDIC also eased up the Volcker Rule.

Introduction A quick summary of the new official digital sign requirement of the FDIC is that effective January 1, 2025, this logo: must be replaced by this logo: For readers who missed part 1 of this series or want to reread the original blog can find it here. 12 CFR § 328.5(a). Answer: No. 12 CFR § 328.5(d). 12 CFR § 328.5(d).

They often must consult paper files as well as information housed in separate digital systems. The speed advantage may be due to large banks greater use of automated lending technology, the FDIC said, although large banks increased reliance on hard credit-scoring information may also play a role. The results?

Banking Trends from the FDIC's 2Q Report Net interest margin reached a new record low, but positive signs emerged in lending. Summary of the Latest FDIC Quarterly Profile. FDIC) released the latest Quarterly Banking Profile recently, and it has some helpful information on industry trends. Banking Data. Learn More.

Federal Deposit Insurance Corporation (FDIC. Now however, the agencies have extended the comment period on the Request For Information on financial institutions’ use of artificial intelligence (AI) until July 1, 2021. Readers may submit responsive information and other comments, identified by Docket No.

The Federal Deposit Insurance Corporation ( FDIC ) is setting new regulations for FinTechs and industrial banks that will enhance transparency and establish record-keeping requirements, the agency said on Tuesday (March 17). The agency’s requirements also ask for particular record-keeping and mandate the reporting of information. .

This month, the Federal Deposit Insurance Corporation (FDIC) launches it new Banker Engagement Site (BES) through FDIC connect. Already reviewed by Perficient, BES provides a secure and efficient portal to exchange documents, information, and communications for consumer compliance and Community Reinvestment Act (CRA) examinations.

Lenders and credit analysts must organize into one cohesive credit memo the following: borrower information, financial ratios, any global cash flow analysis, the assigned risk rating, proposed loan pricing, and terms of the proposed loan. Focus on relevant repayment and credit risk information Whats relevant in a credit memo?

The Federal Deposit Insurance Corporation (FDIC) recently issued a notice of proposed rulemaking (NPR) and request for information (RFI) addressing “False Advertising, Misrepresentation of Insured Status and Misuse of the FDIC’s Name or Logo”.

Smart leaders use performance scorecards to keep the board informed. The FDIC issued a consent order against Discover Bank last year for lacking oversight into third-party risk management and a compliance vendor management program. But with so much information being gathered within an institution, what should CEOs share?

The Federal Deposit Insurance Corporation (FDIC) announced that it is has issued a request for public comments related to small-dollar lending by financial institutions. ” Recent research from the FDIC shows 20 percent of U.S. With that in mind, the FDIC suggests that in 2017, 14.8 million (or nearly 13 percent) of U.S.

The FDIC has announced that it has entered into a settlement of the lawsuit filed against it and the OCC in 2014 by a trade group and several payday lenders challenging “Operation Choke Point” — a federal enforcement initiative involving the FDIC, OCC and other federal agencies. In July 2017, the D.C.

In an internal FDIC document obtained by The Washington Post , it was revealed that the data of 44,000 FDIC customers was breached by an employee who left the agency in February. The memo was distributed on March 18 by FDIC Chief Information Officer and Chief Privacy Officer Lawrence Gross Jr.

House lawmakers aren’t letting up on the Federal Deposit Insurance Corporation (FDIC) when it comes to how the banking regulator handled notifications following a slew of recent data breaches. In a joint letter to FDIC Chairman Martin Gruenberg, seen by WSJ , Rep. Lamar Smith (R-TX) and Rep. Earlier this month, a U.S.

congressional subcommittee spent time yesterday (May 12) during a hearing where the FDIC was questioned about a string of data breaches, including two recent incidents that involved 10,000 sensitive and private data records to be downloaded from workers onto storage devices before they left the agency.

The Washington Post reported that the FDIC is disclosing to Congress the presence of at least five major data breaches that occurred sometime between now and Oct. Though details are still scarce, the FDIC noted that each case was not of the run-of-the-mill hacking variety.

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. This involves the use of AI to inform credit decisions to enhance or supplement existing techniques.

In addition, he noted, a recent consent order from the FDIC required an institution with assets below $1 billion to ‘establish satisfactory quality control procedures over the alert clearing and investigation process. Abrigo Advisors expect this emphasis on quality control will be a theme during exams —even at smaller institutions.

Account for the details before your FDIC bank acquisition Consider these tips for assessing your institution and a to-be-acquired institution for a smooth integration You might also like this webinar, "Valuation and purchase accounting: Navigating the changing M&A landscape."

The agency's request for information seeks comment on the idea of the FDIC partnering with a standards-setting organization to develop best practices for technology firms, among other things.

A rather small bank, as of the end of its first quarter, the bank reported $139 million in total assets and $130 million in total deposits in its FDIC Call Report. Mr. Shan Hanes, who served as the bank’s President and CEO until its closure, joined the firm in 1993 as an agricultural loan officer and Informational Technology Officer.

Takeaway 3 Researchers studied the timing and frequency of on-site inspections by bank staff or third-party inspectors, the contents of the reports, and how the banks used the information in the reports. More construction loan monitoring ultimately decreases loan default, according to a new FDIC Center for Financial Research working paper.

The FDIC has issued a request for information that seeks comment on how the FDIC can make its communications with insured depository institutions (IDIs) “more effective, streamlined, and clear.” The RFI contains specific questions on which the FDIC seeks input that address three topics: efficiency, ease of access, and content.

The Federal Deposit Insurance Corporation has announced that it is launching a new Banker Engagement Site (BES) this month through FDIC connect to serve as the primary tool for exchanging examination planning and other information for consumer compliance and Community Reinvestment Act (CRA) activities. (The

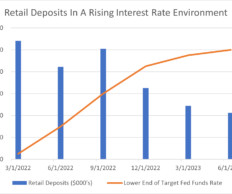

Retail Deposits Defined The FDIC classifies retail deposits as demand or term deposits placed within an FDIC-supervised institution by a retail customer or counterparty, excluding brokered deposits. Make Perficient your go-to partner for informed decision-making in the face of changing interest rates.

FDIC officials in March outlined several types of weaknesses in loan underwriting, administration and oversight practices that are emerging at some banks with CRE portfolios. Eberley, director of the FDIC's Division of Risk Management Supervision wrote in the publication.

On July 25, 2022, the FDIC issued Financial Institution Letter (FIL)-34-2022 announcing updates to Chapters 1 and 4 of its Formal and Informal Enforcement Actions Manual (Manual). The Manual includes updates to the minimum standards for the FDIC’s termination of cease-and-desist and consent orders.

Democratic Senators Elizabeth Warren and Doug Jones have sent a letter to the CFPB, Federal Reserve, OCC, and FDIC expressing concern that fintech and traditional lenders using algorithms in their underwriting processes are engaging in unlawful discrimination. Such algorithms are often referred to as “artificial intelligence.”).

Apple Bank for Savings was accused of failing to comply with the Bank Secrecy Act, according to the Federal Deposit Insurance Corporation (FDIC) per WSJ. The bank was recently fined in a separate charge that it failed to comply with a 2015 request by the FDIC to improve its AML compliance.

The American Bankers Association (ABA) has issued a new white paper , “Effective Agency Guidance: Examining Bank Regulators’ Guidance Practices,” that is intended to help agencies issue guidance that complies with legal requirements while providing useful advice and information to regulated entities.

The Federal Deposit Insurance Corporation (the “FDIC”) has published a request for information in the Federal Register (the “RFI”) seeking comment on approaches it uses, or is considering using, to analyze the effects of its regulatory actions and rulemaking.

The FDIC issued a new Financial Institution Letter ( FIL-23-2021 ) last week in which it announced that, to facilitate implementation of the final rule, it has added a Brokered Deposits webpage to the Banker Resource Center on its website.

Hispanic immigrants have access to actual banking services, the release states, citing an FDIC survey. Hispanic immigrants access digital banking services, according to a press release. Less than half of U.S. Welcome Technologies is using Green Dot’s Banking-as-a-Service technology to create and optimize the features.

The FDIC’s settlement with Umpqua Bank announced yesterday involved collection practices connected with commercial equipment financing offered by the bank’s wholly-owned subsidiary. Disclosing information about the customers’ debts to third parties. ” For more information and to register, click here. . . million CMP.

The FDIC is offering a fresh take on how a bank’s board of directors should understand and manage risk. The regulator’s April edition of Supervisory Insights provides what the FDIC called a “refresher” on its Pocket Guide for Directors, the 1988 booklet outlining the basic duties and responsibilities of a bank’s board of directors.

Earlier this year, the Office of the Comptroller of the Currency (OCC), the Board of Governors of the Federal Reserve System (Fed), and the Federal Deposit Insurance Corporation (FDIC) unveiled a proposed rule that would reshape the landscape for certain financial institutions. Email: Send your comments to regulationshelpdesk@gsa.gov.

On May 31, the Federal Deposit Insurance Corporation (FDIC) reported to the public what many banks already knew and had been experiencing for the past year – that deposits are declining in the American banking sector. There has almost been $1.2 Trillion removed from the banking system over the past year.

On April 2, 2019, the FDIC issued Financial Institution Letter FIL-19-2019 (the “Letter”) to remind financial institutions about certain contractual provisions and other requirements pertaining to technology service provider contracts. Defining key terms in the contracts relevant to business continuity and/or incident response.As

A group of 13 state attorneys general and the District of Columbia AG have sent a letter to the FDIC commenting on the agency’s request for information on small-dollar lending. They recommend that “the FDIC discourage banks from entering into these relationships in any guidance it issues on small-dollar lending.”.

The FDIC has issued new supervisory guidance (FIL-40-2022) on multiple non-sufficient funds (NSF) fees arising from the re-presentment of the same unpaid transaction. In the guidance, the FDIC addresses potential risks arising from multiple re-presentment NSF fees, risk mitigation practices, and the FDIC’s supervisory approach. .

The FDIC has issued a final rule setting forth the conditions it will impose and the commitments it will require to approve a deposit insurance application from an industrial bank or industrial loan company (collectively, ILC) whose parent company is not subject to consolidated supervision by the Federal Reserve Board (FRB).

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content