This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

While the pace of the CFPB’s fair lending activities has slowed under its new leadership, significant fair lending developments are occurring elsewhere. In this week’s podcast, we discuss several of those developments and their broader implications.

McWilliams stated that the FDIC’s top priorities included: (1) reducing regulatory burden on community banks; (2) increasing the speed with which the FDIC reviews charter and deposit insurance applications; and (3) assisting banks to introduce new financial products that serve underserved communities.

On November 15, 2018, in response to a November 7, 2018 letter from Republican Senators , FDIC Chairman Jelena McWilliams announced that the FDIC has engaged outside counsel to investigate the Obama-era Operation Choke Point, under which the FDIC and other government agencies pressured banks not to do business with payday lenders.

The FDIC designated SVB as systemically important. They provide white-label payments and depository services (think Paypal, Chime) and deploy that funding into specialized lending programs such as lending to wealth management firms, commercial fleet leasing, and real estate bridge lending. NasdaqGS: FCNC.A) In 1935, R.P.

Chime said proceeds from the funding will go toward growing the business and launching additional lending and credit products. The company also plans to double its size to more than 200 employees and expand its leadership team. Chime noted in its press release that it began March with more than three million FDIC bank accounts.

The abrupt collapse of Silicon Valley Bank (SVB) is a stunning example of bank leadership not understanding interest rate risk, running into trouble with an inverted yield curve, and ignoring the impact of a severe monetary correction on long-duration assets.

The FDIC has issued its widely anticipated final rule resolving the uncertainty caused by the Second Circuit’s Madden v. The FDIC’s Notice of Proposed Rulemaking (“NPR”) was published the same week as an OCC proposed rule intended to address the same issue for national banks under Section 85. Midland Funding decision. to 1:00 p.m.

Cross River Bank recently found itself in hot water with the FDIC when the agency declared that the bank engaged in unsafe or unsound banking practices in relation to its compliance with fair lending laws and regulations, specifically the Equal Credit Opportunity Act and the Truth-in-Lending Act.

Here, we highlight some of last year’s most successful loan producers in the areas of agriculture, commercial and consumer/mortgage lending. Using FDIC data for 2021, we calculated a lender score out of 100 for each community bank. Ag lending in the South: Relationships matter. It also indirectly benefits our lending business.

It also meant the loss of financial advice, local civic leadership and an institution that brought needed customers to nearby businesses,” Powell said last week , according to reports. .” Now, Powell is also raising concerns about how bank industry consolidation could negatively impact the small business community.

Although one might argue that First Citizens BancShares of Raleigh is a SIFI as it climbed to the 19th largest in the country with its Silicon Valley Bridge Bank acquisition from the FDIC, and that the FDIC designated SVB as systemically important. It has not been all sunshine and rainbows for TBBK. NasdaqGS: FCNC.A) In 1935, R.P.

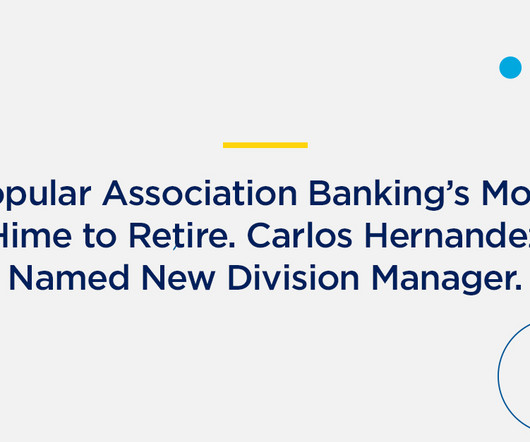

Under her leadership, the team has quadrupled in size and has originated more than $5 Billion in association loans as well as more than $1.6 PAB has provided banking and lending services to community associations since 1994. PAB has an active lending platform in over 30 states. Billion in deposits.

It represents the CFPB’s third rulemaking agenda under Director Kraninger’s leadership. Qualified Mortgage Definition under the Truth in Lending Act (Regulation Z). Other items listed in the agenda on which the CFPB expects to take action this year include: Business Lending Data (Regulation B).

My 30 year career started in merchant e-commerce technology, with numerous product management/leadership/launch roles before moving over to product-innovation research some fifteen years ago. I have a lot to learn! I can’t get enough of innovation and digital strategy. I’d like to hear from you.

Thoughtful lending and an open mind keep profits strong for incoming ICBA chairman Jack Hartings. in Coldwater, Ohio, and ICBA’s incoming chairman, held fast to his community bank’s conservative lending practices. To combat the decline in the bank’s loan-to-deposit ratio, Hartings actively sought out new opportunities in lending.

The rapid emergence of crowdfunding, alternative lending, and peer-to-peer transactions strongly indicates that small businesses are shifting away from the traditional banking environment. According to FDIC Data Calls as outlined in the Forbes , in the 4th Quarter of 2014, traditional banks’ commercial loan portfolios saw a 3.1%

Amid COVID, recession and industry transition, Democrat priorities like fair-lending and inclusion step up as fintech issues loom larger. The post What A Biden Presidency Will Mean to Banks & Credit Unions appeared first on The Financial Brand.

Sometimes 20 minutes, sometimes 50 minutes, this podcast digs into such topics as creating branch experiences that go hand-in-hand with digital ones, identifying risk, and consumer lending. Lending & Credit Risk. Lending & Credit Risk. keep me informed. Whitepaper. Asset Liability Modeling. Asset/Liability. CECL Models.

Financial institutions, fintech companies, and other small business lenders will need to begin collecting a wide array of small business lending data under the Consumer Financial Protection Board’s (CFPB) proposed small business lending data collection rule. The proposed rule , unveiled Sept. Controversial Provisions.

But when it comes to a tactic that plays rope-a-dope with the facts about something, say as serious as whether or not China hacked into the FDIC, then it is not at all cool. Top as in the very top: the FDIC chairman, his chief of staff, and the General Counsel. Lending Club Algorithms . Really, since when?).

It represents the CFPB’s fourth rulemaking agenda under Director Kraninger’s leadership. Other items listed in the agenda on which the CFPB expects to take action before the end of this year and next year include: Business Lending Data (Regulation B). The Bureau released the panel report today.

Big announcements like JP Morgan Chase’s to hike the pay of 22,000 workers and build 400 new branches certainly had bankers inspired to show some level of investment and even civic leadership from the tax break. In addition to a historic tax cut, bankers were equally excited by the shifting winds and tone of the regulatory environment.

In this wide-ranging conversation with two experienced reporters on the consumer finance industry, we discuss differences between the current CFPB and the Trump-era CFPB, including with regard to areas of regulatory and enforcement focus such as UDAAP, consumer access to financial information, small business issues, and fair lending.

The CFPB, under new leadership, should be directed “to aggressively protect consumers by enforcing the law.”. The new CFPB Director should restore the role and responsibilities of the Office of Fair Lending and Equal Opportunity. The DOJ, CFPB, and federal banking regulators should prioritize fair lending enforcement.

Key takeaways regarding the implications of a blue wave scenario include the following: Chris Willis commented that the CFPB’s approach to the exercise of its authorities is likely to reflect criticism by Democrats that the CFPB has been lax in its approach to industry under Director Kraninger’s leadership. (In

consumer lending market anticipated 2017 would be more of the same. This means that the future fate of controversial rulemaking, such as the CFPB’s arbitration and small dollar lending proposals that began under a Democratic administration, will be subject to the Republican Congress’ potential use of the CRA.

Inside the FDIC: Thirty Years of Bank Failures, Bailouts, and Regulatory Battles 2015 Louis D. Giannini: Banker of America 1994 Richard X. Bove Bove, Richard X. Guardians of Prosperity: Why America Needs Big Banks 2013 John F. Bovenzi Bovenzi, John F. Brandeis Brandeis, Louis D. Federal Deposit Insurance Corp. Gorton Gorton, Gary B.

Similar efforts, further crowding the legislative calendar, may be pursued if the CFPB moves forward with issuing its final small-dollar lending regulation. These changes in leadership will assist in the implementation of the President’s financial regulatory reform agenda. So where does that leave us?

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content