This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Vendor management is risky business. The FDIC issued a consent order against Discover Bank last year for lacking oversight into third-party risk management and a compliance vendor management program. Leadership should divulge to the board if it has concerns about any vendor hitting its promises. Reporting .

In addition, he noted, a recent consent order from the FDIC required an institution with assets below $1 billion to ‘establish satisfactory quality control procedures over the alert clearing and investigation process. Streamline case management processes. One of the largest areas for improvement in AML programs is case management.

Meet Model Risk Management Expectations Updates to the FDIC Risk Management Manual should steer institutions toward a model that manages risk and drives growth. Takeaway 1 Aside from meeting examiner expectations, proper model risk management can protect your institution from unnecessary risk. . FDIC Update.

This month, the Federal Deposit Insurance Corporation (FDIC) launches it new Banker Engagement Site (BES) through FDIC connect. Chronology of Compliance Engagement In the pre-personal computer age , FDIC examiners would simply show up at a bank, often by surprise, and start requesting documents from bank executives.

The abrupt collapse of Silicon Valley Bank (SVB) is a stunning example of bank leadership not understanding interest rate risk, running into trouble with an inverted yield curve, and ignoring the impact of a severe monetary correction on long-duration assets. That combination made their liabilities very sensitive to safety.

In various press releases, the Federal Deposit Insurance Corporation (FDIC) has highlighted that an estimated $16.3 Our unparalleled financial services expertise , combined with digital leadership across platforms and business needs, empowers the largest organizations to overcome complex challenges and foster compliant growth.

– These are the exact words (with a couple of expletives, that I cannot quote here) – a senior fund administrator from a large investment firm uttered when we were presenting about environment aware financial risk management. How does it impact me?

A report by the FDIC Office of the Inspector General found the agency failed to sustain corrective actions, leading to a persistent environment of sexual harassment, distrust of management and fear of retaliation.

Twenty years ago there were 14,000 FDIC-insured financial institutions. I think the answer to move our industry forward by establishing an accountability culture is to identify a few, transparent metrics that are consistent with strategy that hold managers accountable for continuous improvement. Today that number is cut in half.

FinCEN issued an advisory in 2014 highlighting the importance of a strong culture of compliance for senior management, leadership, and owners within financial institutions. This includes compliance from top, to middle, to frontline leadership. Leadership must actively support and understand compliance efforts.

Cross River Bank recently found itself in hot water with the FDIC when the agency declared that the bank engaged in unsafe or unsound banking practices in relation to its compliance with fair lending laws and regulations, specifically the Equal Credit Opportunity Act and the Truth-in-Lending Act. In effect, Cross River is in time out.

The FDIC designated SVB as systemically important. They provide white-label payments and depository services (think Paypal, Chime) and deploy that funding into specialized lending programs such as lending to wealth management firms, commercial fleet leasing, and real estate bridge lending. Nasdaq: TBBK) Founded in 2000, this $8.1

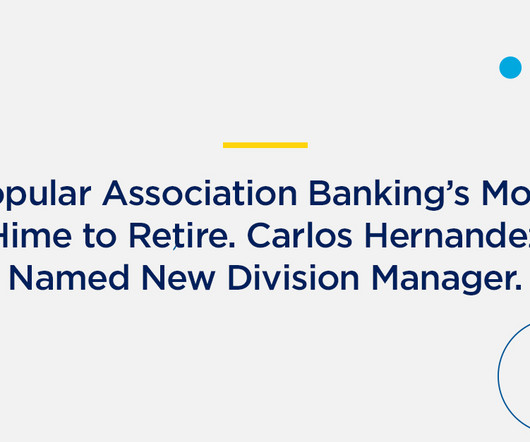

Molly Hime, a long-time Division Manager for Popular Association Banking (PAB), a division of Popular Bank , has announced her retirement, effective December 31, 2023. Under her leadership, the team has quadrupled in size and has originated more than $5 Billion in association loans as well as more than $1.6 Billion in deposits. “It

Effective fraud risk management includes detection and fraud monitoring that should consider customer or member history and behavior. These events are a great way to show leadership and support to the community while having face time with customers, members, and prospects and maximizing time spent.

Although one might argue that First Citizens BancShares of Raleigh is a SIFI as it climbed to the 19th largest in the country with its Silicon Valley Bridge Bank acquisition from the FDIC, and that the FDIC designated SVB as systemically important. Nasdaq: TBBK) Founded in 2000, this $7.5 NasdaqGS: FCNC.A) In 1935, R.P.

Concerns about successors to today’s executive leadership teams dominated many presentations. The FDIC Approved This Ad How many times did we hear a speaker admonish the audience to “be sure and sign up for the FDIC notification list.” While the mood felt upbeat and optimistic (maybe it was the sunny and mid-70s weather?),

Irvine Sprague, Former FDIC Director So Gonzo Bankers … how many of us have been hesitant lately to check our iPhone each morning to see what trouble may have hit the fan in the financial world during a few restless hours of slumber? With the current situation, updates from leadership should be coming out at least weekly.

The second part measures cybersecurity maturity levels within five domains: cyber risk management and oversight; threat intelligence and collaboration; cybersecurity controls; external dependency management; and cyber incident management and resilience. For example: Who manages each piece? How is it secured?

The second part measures cybersecurity maturity levels within five domains: cyber risk management and oversight; threat intelligence and collaboration; cybersecurity controls; external dependency management; and cyber incident management and resilience. For example: Who manages each piece? How is it secured?

Prior to the issuance of the two new reports, the Bureau’s most recent report on overdrafts was issued in August 2017 under the leadership of former Director Cordray. Two earlier reports were issued in June 2013 and July 2014 , also under former Director Cordray.

He exemplifies the best of next generation bank leadership, with eyes wide open to the next iteration of banking in our rapidly changing environment. 2/ @Schornack The primary asset of the organization was Flagship Bank Minnesota, a Member FDIC and Equal Housing Lender with two locations in the Twin Cities Metro Area. million in 2020.

According to the FDIC, the banking industry has roughly $2.5 So Gonzo bankers, as the industry kicks into strategic planning for 2025, leadership should consider the following questions: Human Capital What strategies are we undertaking to develop skills that drive value but are hard to replicate? trillion of capital today.

My 30 year career started in merchant e-commerce technology, with numerous product management/leadership/launch roles before moving over to product-innovation research some fifteen years ago. I have a lot to learn! I can’t get enough of innovation and digital strategy. Impossible? Definitely not. I’d like to hear from you.

While current FCC leadership has tried to address some of the other issues implicated in the 2018 decision (e.g., Stakeholders point to the need for reforms to address currency transactions and suspicious activity reporting as well as a manageable approach to identifying beneficial owners of accounts.

I can think of no reason why a bank would claim the mantel of brand leadership if they must routinely price up deposits or reduce loan yields or structures to get new customers. But they may not be in their operating account or some special purpose savings accounts where they want the FDIC insurance and efficient transaction processing.

But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent risk management practices. Using FDIC data for 2021, we calculated a lender score out of 100 for each community bank. By Ed Avis. Methodology. Lee’s Summit, Mo. Asset size: $738 million.

According to FDIC Data Calls as outlined in the Forbes , in the 4th Quarter of 2014, traditional banks’ commercial loan portfolios saw a 3.1% Kyle Enger, known for his thought leadership in the world of relationship banking on the West Coast said it best, “Traditional banks have to embrace digital lending in their hometowns to compete.”.

Yet his steady leadership is paired with a willingness to challenge the status quo cautiously to keep up with an evolving marketplace—a quality that appealed to the bank’s board when it promoted him from loan officer to bank president 25 years ago. FDIC Advisory Committee on Community Banking, member. Thoughtful action.

Thankfully for bank and credit union executives, lenders, risk managers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing.

In 1979, George Gleason, a 25-year-old attorney, purchased controlling interest and assumed active management of the bank as Chairman of the Board and Chief Executive Officer. Collectively, the management team built an Arkansas franchise rivaling the largest banks in the state. The company moved its headquarters to Little Rock in 1995.

But when it comes to a tactic that plays rope-a-dope with the facts about something, say as serious as whether or not China hacked into the FDIC, then it is not at all cool. Top as in the very top: the FDIC chairman, his chief of staff, and the General Counsel. ” According to the store manager sales jumped 75 percent.

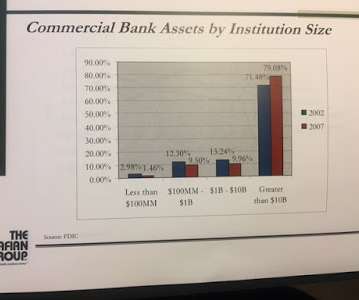

When I made that speech in 2008, there were approximately 8,500 FDIC-insured financial institutions and today that is around 5,000, a 40% decline. Banks and savings banks with greater than $10 billion in total assets control 86% of all FDIC-insured assets and 85% of deposits for the most recent quarter. It was a pretty alarming slide.

You might also like this webinar: "Fortify Your Loan Policy to Effectively Manage Credit Risk." The data is intended to help the CFPB enforce fair lending laws and could also be used by the government and small business lenders to identify the needs of businesses, said Michelle Lucci, Abrigo Regulatory Compliance Manager. CRE Lending.

Facebook leadership underestimated the role that platform governance plays in keeping platforms alive and thriving – and it may be too little, much too late to turn things around. And that is a bank – one with FDIC insurance and safeguards that keep their money safe. The scariest thing for Facebook is the people who use it.

Big announcements like JP Morgan Chase’s to hike the pay of 22,000 workers and build 400 new branches certainly had bankers inspired to show some level of investment and even civic leadership from the tax break. In addition to a historic tax cut, bankers were equally excited by the shifting winds and tone of the regulatory environment.

We previously reported that Paul Atkins would be on the landing team for the CFPB as well as the landing teams for the FDIC and OCC. Jordan is currently President and CEO of a government relations firm that specializes in strategic business development and President of the National Black Republican Leadership Council.

Inside the FDIC: Thirty Years of Bank Failures, Bailouts, and Regulatory Battles 2015 Louis D. Manias, Panics, and Crashes: A History of Financial Crises 2005 John Jay Knox Knox, John Jay A History of Banking in the United States 2017 Timothy Koch Koch, Timothy Bank Management (8th ed.) Giannini: Banker of America 1994 Richard X.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content