This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Understanding the drivers of banking consolidation is imperative when managing bank performance. In 1985, there were 14,417 FDIC banking charters. Germain Depository Institutions Act of 1982 enabled thrifts to offer money market accounts and expand lending powers, fostering competition with banks.

In the wake of regional bank failures, one potential answer to equity shorting and bank runs is having the FDIC increase deposit insurance. private and public lending markets are the world’s envy, with a wide availability of financing options for many capital seekers across the entire capital stack. economy needs.

Meet Model Risk Management Expectations Updates to the FDIC Risk Management Manual should steer institutions toward a model that manages risk and drives growth. Takeaway 1 Aside from meeting examiner expectations, proper model risk management can protect your institution from unnecessary risk. . FDIC Update.

Navigating interest rate management in today's environment As regulators focus on interest rate risk management, read about what financial institutions can do to be ready for a rate drop. You might also like this on-demand webinar, "Navigating uncertain times: Strategies for effective risk management and compliance."

Add FDIC Chairman Martin J. The FDIC said that the percentage of loans and securities with maturities of three or more years hit the highest percentage in the 18 years of data records, rising to 34.6 Community banks have grown their share of longer-term assets even more quickly than the rest of the industry, according to the FDIC.

Seeking additional arrows in their quiver against large bank failures, on October 14, 2022, the Federal Reserve Board (FRB) and Federal Deposit Insurance Corporation (FDIC) published an Advance Notice of Proposed Rulemaking (ANPR). Both the FRB and FDIC will accept comments and answers for 60 days after publication in the Federal Register.

Managing loan workouts and modifications Tips for preparing your bank or credit union to handle an increased volume of problem loans while ensuring prudent credit risk management. Takeaway 2 Meanwhile, banks and credit unions will likely see a beefed-up regulatory emphasis on credit risk management practices, especially tied to CRE. .

Many banks offer money market accounts (MMAs). You may be wondering how this type of account fits into your money management plans. Use the guide below to find out what a money market account is, how its different from a traditional checking account, and how you can select the best account to achieve your financial goals.

The insight here is that if you price and market the product correctly, instant payments will not only start to cannibalize other payment channels such as cash, checks, and wires, but it will also have a set of other attributes impacting bank performance. The intensity color within the cell represents the degree of dominance of that category.

On the liability side of SVB’s $173B in deposits at the end of 2022, approximately 97% were uninsured and above the $250k in FDIC protection threshold. Based on the bank’s own filing, and like many banks, SVB did not deploy hedging instruments to manage its securities duration risk.

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. Risk Management. AI may be used to augment risk management and control practices. Credit Decisions.

ALM | 4 minute read Key Takeaways Many financial institutions view asset/liability management as a "check-the-box" regulatory exercise. An extreme focus on using ALM to manage the risk of rising rates means some FIs overlook using ALM to grow earnings and capital, putting them at risk of underperformance. ALM seen as checking the box.

Commercial real estate lending continues to receive regulatory scrutiny and reminders for financial institutions to practice solid risk management. FDIC officials in March outlined several types of weaknesses in loan underwriting, administration and oversight practices that are emerging at some banks with CRE portfolios.

CFIs are poised to regain the small business lending market Community Financial Institutions can leverage technology to improve customer experience and regain the small business lending market. Today, CFIs are uniquely positioned to regain the market. Changing Lending Environment. Small businesses are turning to small lenders.

You might also like this webinar, "How to manage a high-performing construction loan portfolio." More construction loan monitoring ultimately decreases loan default, according to a new FDIC Center for Financial Research working paper. On-site inspections. Bank monitoring in construction lending.

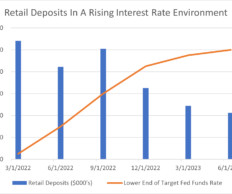

In our previous article, “ Transaction Accounts: Analyzing Deposit Stickiness in the Current Interest Rate Environment ,” Perficient’s Financial Services Risk Management and Regulatory Capabilities Center of Excellence (CoE) explored the sharp decline in transaction account balances over an 18-month period. Contact us today!

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. A hedge should have a neutral outcome regardless of how the market moves (within defined bands).

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. A hedge should have a neutral outcome regardless of how the market moves (within defined bands).

It’s free and makes managing small business finances easy, even for those with little finance and accounting knowledge.”. The company also noted that deposits are FDIC insured for a maximum of $250,000.

is set to see its first new community bank in decades, as the Federal Deposit Insurance Corporation (FDIC) lent its approval for MOXY Bank to launch in Washington, D.C. MOXY Bank, for example, aims to introduce corporate treasury management services, as well as offerings for small business (SMB) owners. Bloomberg listed Casey G.

The FDIC has issued an “Advisory to FDIC-insured institutions Regarding Deposit Insurance and Dealings with Crypto Companies ” to address the agency’s concerns regarding misrepresentations about FDIC deposit insurance by certain crypto companies. The FDIC identifies two issues that can create customer confusion.

On May 31, the Federal Deposit Insurance Corporation (FDIC) reported to the public what many banks already knew and had been experiencing for the past year – that deposits are declining in the American banking sector. There has almost been $1.2 Trillion removed from the banking system over the past year.

We’re proud to offer financial market infrastructure that supports an open, digital financial future.”. while enabling Revolut to control “the user experience” and manage its “customer relationships.” Paxos will hold crypto assets for Revolut’s users in the U.S., Revolut made its U.S.

That marketing material was removed from the page over the weekend, as were tweets promoting it at the launch — the FinTech is now calling the offering a cash management service, reported Bloomberg. The executives told Bloomberg they are working with regulators and are in the process of overhauling the marketing material related to it.

We compared and contrasted the two strategies and sized the market for community banks. Second, community banks should use FDIC-insured institutions as hedge providers, and the hedges must be structured as qualified financial contracts (QFC). We also shared a table that summarized the two strategies.

If managing loan pricing is a college-level course, deposit pricing is a master’s. Given the complexity, managing analyzed checking, however, is a PhD. We covered the basics of account analysis in Part 1 ( HERE ), and in this article, we highlight best practices for managing an analyzed transaction account. level effort.

While we wrote about the root cause of the failure of Silicon Valley Bank (SVB) HERE , the lessons of the current banking crisis go beyond interest rate risk management. Previously, if banks were able to borrow against these securities, it would be at 98% of the market value or less, depending on the investment type.

The OCC and FDIC issued proposed rules this week intended to eliminate the uncertainty created by the Second Circuit’s decision in Madden v. Comments on the FDIC’s proposal must be submitted no later than 60 days after the date the proposal is published in the Federal Register. Midland Funding. 85 [or 12 U.S.C

Key Takeaways The FDIC issued an advisory to FIs encouraging safe and sound lending practices in today's ag lending environment. FDIC) issued an advisory to financial institutions encouraging exceptionally safe and sound lending practices in agricultural lending. On January 28, the Federal Deposit Insurance Corp.

On August 19, 2022, the FDIC issued cease and desist letters to five crypto companies, alleging they made false and misleading statements about FDIC deposit insurance and demanding immediate corrective action. According to the FDIC’s press release , “[b]ased upon evidence collected., Part 328, Subpart B.

Mitigating market risk comes from proper customer selection, structuring the loan as to not acerbate a bank’s risk, pricing the relationship correctly taking into account cost and risk through the loan lifetime, actively managing that customer (monitoring credit, building deposit balances, increasing engagement, enhancing fee income, etc.)

A change in market interest rates seems to be an example where a bank’s NIM may change, and all other variables remain the same. Historically short-term interest rates have decreased because the Federal Reserve is managing slowing economic activity. During economic contractions nonaccrual loans increase and NIM decreases.

Robinhood , the investment app that upended its market by elimination of commissions on stock trades is bringing its brand of disruption to the United Kingdom. Robinhood made money and picked up business without focusing on the rules,” said Tyler Gellasch, executive director of trade association Healthy Markets Association in a statement. “As

In recent years, the community banks market share has been diminishing markedly as bank consolidation has occurred. FDIC-reporting institutions to include banks and savings institutions. The share of the loan market held by community banks has declined more rapidly (proportionately) than the number of charters.

FDIC) is looking to modernize bank reporting. FDIC Looks To Modernize Bank Reporting. A Merchant’s How-To For Managing The Contactless Payments Surge And SCA Requirements. Plus, the Federal Deposit Insurance Corp. Wirecard Forces ‘Radical’ Reboot Of German Accounting Regs. The Federal Deposit Insurance Corp.

“At Joust, we understand the growing market of self-employed workers, freelancers and small businesses, and their need for an all-in-one banking solution –especially one that gives them the same benefits enjoyed by major corporations. The bank combines an FDIC-insured account and a merchant account and accepts a variety of payments.

Would you like other articles on asset/liability management in your inbox? Takeaway 1 Regulators stress sound risk management practices that include the ability to identify and measure interest rate risk (IRR). FDIC) noted in its 2021 Risk Review.

On September 7, 2023, the FDIC released its banking profile. This quarterly publication provides a comprehensive financial results summary for all FDIC-insured institutions (4,645 commercial banks and savings institutions insured by the FDIC). Rising market interest rates. While banks under $10B in assets comprise 97.8%

FDIC-insured “Problem Banks” list has been increasing over the past two years. We aim to explain the reason for this spike in the percentage of unprofitable community banks so that bankers can better manage their business model. Bank ROE is now a problem.

Real Estate Market Outlook. MBA Vice President for CRE Research Jamie Woodwell said in a news release that low interest rates gave CRE markets a boost last year. “In With global bond yields expected to remain extremely low and equity markets likely weaker and more volatile, the stable, solid returns of U.S.

With the assistance of the FDIC, Fulton Financial acquired certain assets, debt and deposits of Republic Bank. Also, interest rates are not high by historical comparison (especially when eliminating the pandemic monetary response), and bank managers’ job is to manage uncertatiny (also called risk).

In this article, we highlight the details of these digital wallets and provide bankers with five marketing campaigns to bring these deposits back on balance sheet. Banks should have campaigns ready to go and then launch an email campaign marketing the bank’s safety, soundness, control, and liquidity.

Robinhood Markets, coming off a new $280 million funding round backed by Sequoia Capital, has seen its value and services expand during the coronavirus pandemic, according to a Reuters report. More market turmoil has also driven people’s interest. The company, launched in 2013, is now valued at $8.3

Avert Risk The OCC’s October 2012 Supervisory Guidance notes that financial institutions that perform stress testing “have the ability to minimize the impact of negative market developments more effectively” than those that do not have a stress testing process in place.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content