This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Meet Model RiskManagement Expectations Updates to the FDICRiskManagement Manual should steer institutions toward a model that managesrisk and drives growth. Takeaway 1 Aside from meeting examiner expectations, proper model riskmanagement can protect your institution from unnecessary risk. .

The guidance is aimed at helping banks address the operational, compliance and strategic risks of third-party tie-ups, such as those with fintech firms.

On the liability side of SVB’s $173B in deposits at the end of 2022, approximately 97% were uninsured and above the $250k in FDIC protection threshold. Based on the bank’s own filing, and like many banks, SVB did not deploy hedging instruments to manage its securities duration risk.

The lender needs to put forth an accurate and complete picture of the borrowernot only for the borrowers sake, but also for the financial institutions riskmanagement. Kirby cited FDIC statistics showing nearly three-quarters of community banks require three or more levels of approval, regardless of the loan size.

Vendor management is risky business. The FDIC issued a consent order against Discover Bank last year for lacking oversight into third-party riskmanagement and a compliance vendor management program. Does a relationship manager check in regularly with the institution—and not a month or two before renewal?

A segmentation strategy, though, is a great place to start to nail down an effective and efficient process – not only will it serve a substantial purpose for the ALLL, but also as a larger riskmanagement tool. The goal is for the segmentation to be granular enough for the pools to show those similar loan characteristics.

M anaging, not avoiding, small business lending A common reason banks hesitate to expand small business lending is the fear of risk. While its true that nearly half of small businesses fail within five years, risk avoidance isnt the solution. Kirby pointed out that fintech lenders frequently use these models to approve loans quickly.

Each step of back-end loan processingfinancial spreading, risk assessment, document gatheringrequires significant effort just to make incremental progress. Among large banks, 42% currently use financial technology in small business lending, compared to 30% of small banks, according to the FDIC. The results?

In a recent Sageworks webinar Robert Ashbaugh, senior riskmanagement consultant at Sageworks, discusses High Volatility Commercial Real Estate (HVCRE) lending best practices. That 13% represented 80% of the losses to the FDIC insurance fund. How did we get here?

Perficient provides riskmanagement to more than 500 financial services organizations, many of whom have multiple bank regulators. Often an organization will have a state-charted non-member bank, which has the FDIC as its primary federal regulator. Introduction It’s not you. It’s the guidance.

Banking Trends from the FDIC's 2Q Report Net interest margin reached a new record low, but positive signs emerged in lending. Summary of the Latest FDIC Quarterly Profile. FDIC) released the latest Quarterly Banking Profile recently, and it has some helpful information on industry trends. Portfolio Risk & CECL.

The FDIC is offering a fresh take on how a bank’s board of directors should understand and managerisk. The core principles for directors have not changed materially since 1988, the FDIC said. Riskmanagement culture What exactly is a riskmanagement culture? Evaluating riskmanagement.

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. RiskManagement. AI may be used to augment riskmanagement and control practices.

Managing loan workouts and modifications Tips for preparing your bank or credit union to handle an increased volume of problem loans while ensuring prudent credit riskmanagement. You might also like this video, "A look at credit risk in a rising-rate environment." Signs of increased activity ahead. Watch webinar.

But the slew of banking regulatory requirements for third party riskmanagement is proving to be complex, all-consuming and expensive for both institutions and the third parties involved. In a nutshell, institutions are liable for risk events of their third and extended parties and ecosystems. " www.fdic.gov.

Navigating interest rate management in today's environment As regulators focus on interest rate riskmanagement, read about what financial institutions can do to be ready for a rate drop. You might also like this on-demand webinar, "Navigating uncertain times: Strategies for effective riskmanagement and compliance."

Commercial real estate lending continues to receive regulatory scrutiny and reminders for financial institutions to practice solid riskmanagement. FDIC officials in March outlined several types of weaknesses in loan underwriting, administration and oversight practices that are emerging at some banks with CRE portfolios.

But the slew of banking regulatory requirements for third party riskmanagement is proving to be complex, all-consuming and expensive for both institutions and the third parties involved. In a nutshell, institutions are liable for risk events of their third and extended parties and ecosystems. ” www.fdic.gov.

In various press releases, the Federal Deposit Insurance Corporation (FDIC) has highlighted that an estimated $16.3 billion of the total cost incurred from the failures of Silicon Valley Bank (SVB) and Signature Bank was designated for safeguarding uninsured depositors. Commencing with the first quarterly assessment period of 2024 (i.e.,

ALM | 4 minute read Key Takeaways Many financial institutions view asset/liability management as a "check-the-box" regulatory exercise. An extreme focus on using ALM to manage the risk of rising rates means some FIs overlook using ALM to grow earnings and capital, putting them at risk of underperformance.

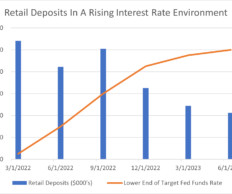

In our previous article, “ Transaction Accounts: Analyzing Deposit Stickiness in the Current Interest Rate Environment ,” Perficient’s Financial Services RiskManagement and Regulatory Capabilities Center of Excellence (CoE) explored the sharp decline in transaction account balances over an 18-month period. Contact us today!

A rather small bank, as of the end of its first quarter, the bank reported $139 million in total assets and $130 million in total deposits in its FDIC Call Report. Mr. Herndon named the Federal Deposit Insurance Corporation (“FDIC”) as receiver, allowing the FDIC to take control of the Heartland Tri-State’s operations.

FDIC) and the Treasury Department are looking to see if American Express Co. Representatives of the Fed, FDIC and Treasury inspectors general offices would not comment on the matter, the paper reported. Officials at the Federal Reserve, the Federal Deposit Insurance Corp. 7), citing unnamed sources. “We

Last week, the OCC, Federal Reserve Board, and FDIC issued proposed guidance for banking organizations on managingrisks associated with third-party relationships, including those with financial technology-focused entities such as bank/fintech sponsorship arrangements. On August 6, 2021 from 12:00 p.m. to 1:00 p.m.

The Federal Reserve, FDIC, and OCC have released final interagency guidance for their respective supervised banking organizations on managingrisks associated with third-party relationships, including relationships with financial technology-focused entities such as bank/fintech sponsorship arrangements. Continue Reading

You might also like this webinar, "How to manage a high-performing construction loan portfolio." More construction loan monitoring ultimately decreases loan default, according to a new FDIC Center for Financial Research working paper. On-site inspections. Bank monitoring in construction lending.

and Texas banking regulators issued consent orders against Industry State Bank, Fayetteville Bank, and Citizens State Bank requiring major overhauls of their management, capital, and risk controls. The Federal Deposit Insurance Corp.

Watch NOW Takeaway 1 Portfolio risk and accounting professionals often keep up to date on industry trends by reading Abrigo's blog. Takeaway 2 Management reports, probability of default, and model validation topics were found in the top blogs for risk professionals. The FASB’s description of proposed changes can be found here.

Applying model riskmanagement to CECL What's involved in CECL model validation? Learn what banks, credit unions, and others subject to CECL accounting can expect from this riskmanagement process. Model validation is a crucial aspect of model riskmanagement.

Account for the details before your FDIC bank acquisition Consider these tips for assessing your institution and a to-be-acquired institution for a smooth integration You might also like this webinar, "Valuation and purchase accounting: Navigating the changing M&A landscape."

The FDIC has defined community banks in their December 2020 Community Banking Report that either exclude or include the following criteria: Seems complicated. But the FDIC did confess that a community bank was not easily defined. A big bank makes riskmanagement decisions at headquarters in a location far, far away.

Financial institutions are responsible for not only facilitating payments but also managing risksincluding fraud, compliance, and operational challenges. Federal Reserve Manages ACH, FedNow, and interbank payments. Reduce loss and protect your customers with our sophisticated detection and fraud management software.

The Federal Reserve, FDIC, and OCC have released proposed guidance for banking organizations on managingrisks associated with third-party relationships, including relationships with financial technology-focused entities such as bank/fintech sponsorship arrangements. Due diligence and third-party selection. Contract negotiation.

Total deposits in FDIC-insured banks increased by a record $1.2 billion between January and March, data shows RiskManagement Covid19 PPP The Economy Feature Feature3 Fair Lending.

The FDIC has issued an “Advisory to FDIC-insured institutions Regarding Deposit Insurance and Dealings with Crypto Companies ” to address the agency’s concerns regarding misrepresentations about FDIC deposit insurance by certain crypto companies. The first portion of the advisory addresses risks and concerns.

This being the first blog post in a series of blogs by Perficient’s Financial Services RiskManagement and Regulatory Capabilities Center of Excellence (CoE), we will be investigating the deposit structures of non-client banks over time.

An inverted yield curve, continued bank failures, and the desire to managerisk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. Good hedging partners will pass on taking trades that generate revenue for the vendor but create more unforeseen risk.

An inverted yield curve, continued bank failures, and the desire to managerisk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. Good hedging partners will pass on taking trades that generate revenue for the vendor but create more unforeseen risk.

– These are the exact words (with a couple of expletives, that I cannot quote here) – a senior fund administrator from a large investment firm uttered when we were presenting about environment aware financial riskmanagement. How does it impact me?

Measuring Interest Rate Risk Can Vary by Institution Interest rate risk measurement plays a key role in ensuring an institution's safety and soundness. Would you like other articles on asset/liability management in your inbox? FDIC) noted in its 2021 Risk Review. Portfolio Risk & CECL. Asset/Liability.

With the assistance of the FDIC, Fulton Financial acquired certain assets, debt and deposits of Republic Bank. Also, interest rates are not high by historical comparison (especially when eliminating the pandemic monetary response), and bank managers’ job is to manage uncertatiny (also called risk).

The desire to avoid examiner scrutiny may tempt some financial institutions to set the bar high when it comes to credit and liquidity riskmanagement policy limits, but regulators are discouraging this approach. That means limits should be properly aligned with the true risk tolerance of your board and management.”

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content