This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Startup Varo Money has raised $45 million for its plans to become a full-fledged, “national bank,” the startup announced yesterday. The funds will go towards marketing its service as well as for laying “the foundation” to become a bank, company CEO Colin Walsh told TechCrunch.

Figure Pay, he said, with the ability to scan QR codes at checkout, is predicated on the concept of using a blockchain payment rail in lieu of interchange as the network is built out — and across a swath of merchants as large as Walmart and small as localized farmers’ markets (in a type of “barbell” approach) upon initial launch early next year.

Add FDIC Chairman Martin J. The FDIC said that the percentage of loans and securities with maturities of three or more years hit the highest percentage in the 18 years of data records, rising to 34.6 Community banks have grown their share of longer-term assets even more quickly than the rest of the industry, according to the FDIC.

The House committee held a hearing on the idea after Acting Comptroller of the Currency Brian Brooks in July proposed a new special purpose national banking charter for payments companies. FDIC), the states and the courts. However, the banking industry doesn’t like that one bit. “We

Meet Competitive Pressures : National and larger regional banks are specifically targeting better borrowers for five, seven, ten-year fixed-rate loans. We witness over and over how some banks get themselves in deeper trouble booking derivatives on their books that are bets on market interest rate movements.

Meet Competitive Pressures : National and larger regional banks are specifically targeting better borrowers for five, seven, ten-year fixed-rate loans. We witness over and over how some banks get themselves in deeper trouble booking derivatives on their books that are bets on market interest rate movements.

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. Office of the Comptroller of the Currency (OCC). Credit Decisions. Textual analysis.

is set to see its first new community bank in decades, as the Federal Deposit Insurance Corporation (FDIC) lent its approval for MOXY Bank to launch in Washington, D.C. The FDIC’s announcement said a private placement offering will raise at least $25 million for the bank ahead of its launch. . Bloomberg listed Casey G.

New York Venture Bank, a new financial institution (FI) created by big names in the financial services industry, has applied for a national bank charter. FDIC), the news report noted the new bank will begin with $100 million in capital. According to a Wednesday (Nov. Citing documents filed with the Federal Deposit Insurance Corp.

The plain language of the governing federal statute applies only to interest that an FDIC-insured state bank may charge. Allegedly, the FDIC’s rule represents an expansion of the FDIA’s preemption of state law interest rate caps by extending the preemption to assignees of loans originated by such banks.

The OCC and FDIC issued proposed rules this week intended to eliminate the uncertainty created by the Second Circuit’s decision in Madden v. Comments on the FDIC’s proposal must be submitted no later than 60 days after the date the proposal is published in the Federal Register. Midland Funding. 85 [or 12 U.S.C

And as reported by sites such as American Banker and National Law Review , a bipartisan group of senators is working on a bill that may reform the Bank Secrecy Act, which in turn may raise the threshold for reporting currency transaction reports to $30,000, from the current levels of $10,000. This would be the first boost in 25 years.

The FDIC has issued a final rule that establishes a new framework for analyzing whether deposits made through deposit arrangements qualify as “brokered deposits” and amends the methodology for calculating the interest rate restrictions that apply to less than well capitalized insured depository institutions (IDIs).

We compared and contrasted the two strategies and sized the market for community banks. Meet Competitive Pressures: National and larger regional banks are specifically targeting better borrowers for seven, ten, or 20-year fixed-rate loans. We also shared a table that summarized the two strategies.

Mitigating market risk comes from proper customer selection, structuring the loan as to not acerbate a bank’s risk, pricing the relationship correctly taking into account cost and risk through the loan lifetime, actively managing that customer (monitoring credit, building deposit balances, increasing engagement, enhancing fee income, etc.)

The remarks were made at a conference, focusing on the issue of “financial deserts,” involving the struggle for rural communities to feel the benefits of overall national economic strength and a declining unemployment rate. making it one of the nation’s first new community banks in years.

On Tuesday, the FDIC released a Notice of Proposed Rulemaking (NPR) that outlines anticipated revisions to its regulations regarding interest rate restrictions that apply to less than well capitalized insured depository institutions. Methodology for Calculating National Rate and Rate Cap. Process for Establishing a Local Rate Cap.

The FDIC’s issuance of the RFI signals that the FDIC intends to follow suit. A glaring regulatory impediment to small-dollar lending by FDIC-supervised institutions is the FDIC’ s November 2013 guidance on deposit advance products , which effectively precludes FDIC-supervised institutions from offering deposit advance products. (In

And in PYMNTS’ own coverage, the twin external forces of regulatory scrutiny and market pressures are pushing FIs to retool and strengthen their anti-money laundering (AML) efforts. In one example, reported on Monday (Sept. billion in fines. Much of those revamped efforts come, perhaps not surprisingly, through advanced technologies.

The average national yield of savings accounts is 0.10%, whereas Betterment’s annual yield is 2.69%. Like other FinTechs, Betterment will partner with FDIC-insured institutions since it doesn’t have a bank charter. By collaborating with FinTechs, banks can bring a solution to market faster and offer it themselves.

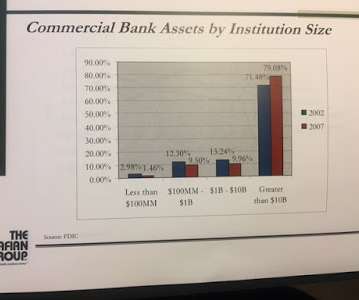

In recent years, the community banks market share has been diminishing markedly as bank consolidation has occurred. FDIC-reporting institutions to include banks and savings institutions. The share of the loan market held by community banks has declined more rapidly (proportionately) than the number of charters.

The market expects the current inverted yield curve to remain through much of 2024 (based on long-term interest rates and the expected rate cuts in 2024). This article will discuss how national, regional, and community banks may use loan hedging programs in 2024 to face earnings challenges. Only 304 banks (or 6.7%

Against that backdrop, there are, at present, no plans for the nation to issue a state-backed cryptocurrency, as the government has pointed toward continuing concerns over money laundering and cyber risks. Frankly, recent market movements have not given us any reason to be concerned,” she said. In the U.S., Banks are well capitalized.

The FDIC designated SVB as systemically important. I chose five years because banks that focus on year-over-year returns tend to cut strategic investments come budget time, which hurts their market position, earnings power, and future relevance more than those that make those investments. million in net income for an ROA of 0.73%.

Dunkleberg is the former dean of Temple’s School of Business and Management and has served as the Chief Economist for the National Federation of Independent Business since 1971. Bankers’ attitudes reflect conditions in capital markets and conditions in the economy, primarily the local economy served by each bank,” Dunkelberg and Scott wrote.

Percentage of Uninsured Deposits: At the time of failure, SVB had approximately 88% of their deposits above the FDIC-insured $250k limit and ran at 95% at the end of last year. Some form of this ratio will likely be applied to the national and regional banks, which means larger community banks will also be judged by this ratio.

percent APY, which is about 22 times higher than the average of national accounts. The bank will handle the funds and will offer FDIC protection up to $5 million. Although Credit Karma’s APY is high, it’s not the best on the market. It offers a savings rate of 2.03 Vio, an online bank, has an account that pays 2.42

The Commodity Futures Trading Commission ( CFTC ), Federal Deposit Insurance Corporation ( FDIC ), Office of the Comptroller of the Currency ( OCC ), and the Securities and Exchange Commission ( SEC ) have announced that they are joining the Global Financial Innovation Network ( GFIN ).

Noninterest income associated with the housing markets such as securitization, trading, and real estate slowed significantly during the financial crisis and beyond. To remain competitive, some of the nations’ largest banks have introduced new products. Community banks have seen less volatility in noninterest income over time.

Axos Bank parent company Axos Financial has rolled out out commercial banking operations across new markets in the U.S., “The nation’s two largest metropolitan areas are home to a majority of our commercial lending and banking clients,” said Greg Garrabrants, president and CEO of Axos, in a statement.

market is not like others across the globe. Regulatory efforts through the Office of the Comptroller of the Currency aim to connect FinTechs with the opportunity to apply for a national bank charter, an initiative that has been met with criticism and legal action. Bank participation is key to promoting open banking in the U.S.,

After moving alone in 2020 to reform its Community Reinvestment Act (CRA) regulation, the Office of the Comptroller of the Currency (OCC) has joined the Federal Deposit Insurance Corporation (FDIC) and Federal Reserve Board in issuing a joint notice of proposed rulemaking setting forth proposed amendments to their regulations implementing the CRA.

Four product variables impact profitability – rate, fees, marketing/brand, and companion products for a standard bank product such as a business savings account. This spheroid is asymmetrical as deposit performance is heavily influenced by ECR, hard interest, companion products, and marketing/brand.

Using FDIC data for 2021, we calculated a lender score out of 100 for each community bank. He sensed the family’s passion and liked their idea of starting with selling milk at farmers’ markets, roadside shops and small grocery stores. American Bank, National Association. Classic Bank, National Association. By Ed Avis.

A mid-2020 survey performed by Cornerstone Advisors showed that 51% of retail customers that opened a new bank account within the last three months did so at a large, national bank. When I made that speech in 2008, there were approximately 8,500 FDIC-insured financial institutions and today that is around 5,000, a 40% decline.

In a press release, the trade group said that in the past, the guidance has been to discourage these types of small-dollar loans; after the guidance was rescinded, banks weren’t sure whether they would be able to go back into the market. In any market, robust competition is a win for consumers.

Over the first half of 2014, these banks, with an approval rate of just under 60 percent, beat out large national banks (31 percent), large regional banks (45 percent) and online lenders (38 percent). Within this sector, small regional and community banks moved up to the second most popular source for applicants.

Of course, those more than beat the national average on checking accounts, which is currently at a 0.08 percent interest rate, while money market accounts return an average 0.21 In addition, Ally Bank and Barclays have high-yield offerings that earn 2.2

Banks of all sizes are hearing from many customers that they want exposure to the fast-growing but volatile cryptocurrency market. Vast Bank recently became the first nationally chartered, FDIC-insured bank to offer crypto banking.

With big banks pulling back from small and medium-sized business (SMB) lending in the wake of the global financial crisis, the market was ripe for someone else to fill the credit gap. The FDIC’s Advisory Committee on Community Banking offered a platform through which community bankers could highlight these challenges.

Brazos National Bank. Douglas National Bank. FSNB, National Association. Pioneer Trust Bank, National Association. AMG National Trust Bank. HNB National Bank. A: We strategically positioned ourselves to take advantage of the market. We were gaining more market share by calling on all the Realtors.

financial services firm, on Wednesday (July 25) sold its entire stake in 321 Crédito, a Portuguese consumer finance lender, to Banco CTT, the bank run by Portugal’s privatized national postal service. car loan market due to fears that consumers have taken on more debt than they can handle. Cabot Square Capital, a U.K. trillion U.S.

The Federal Reserve, OCC, FDIC, and NCUA have issued “ Interagency Lending Principles for Offering Responsible Small-Dollar Loans.” Marketing and customer disclosures that comply with applicable laws and regulations and provide information in a clear, conspicuous, accurate, and customer-friendly manner.”.

Takeaway 2 The severely adverse scenario from regulators presents a very severe global recession combined with severe stress in the CRE market and the corporate debt market. The Federal Reserve Board, OCC, and FDIC provided two hypothetical scenarios: baseline and severely adverse. Why financial institutions stress test.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content