This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Meet Model RiskManagement Expectations Updates to the FDICRiskManagement Manual should steer institutions toward a model that managesrisk and drives growth. Takeaway 1 Aside from meeting examiner expectations, proper model riskmanagement can protect your institution from unnecessary risk. .

On the liability side of SVB’s $173B in deposits at the end of 2022, approximately 97% were uninsured and above the $250k in FDIC protection threshold. in adjustment (9.2%) for interest rate risk movement. That fact makes the bank’s deposits less sticky and subject to outflow at any sign of insolvency.

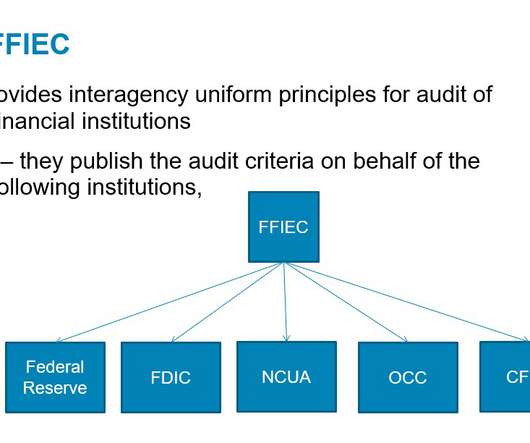

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. RiskManagement. AI may be used to augment riskmanagement and control practices.

Commercial real estate lending continues to receive regulatory scrutiny and reminders for financial institutions to practice solid riskmanagement. FDIC officials in March outlined several types of weaknesses in loan underwriting, administration and oversight practices that are emerging at some banks with CRE portfolios.

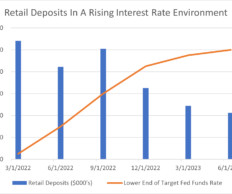

In our previous article, “ Transaction Accounts: Analyzing Deposit Stickiness in the Current Interest Rate Environment ,” Perficient’s Financial Services RiskManagement and Regulatory Capabilities Center of Excellence (CoE) explored the sharp decline in transaction account balances over an 18-month period.

More construction loan monitoring ultimately decreases loan default, according to a new FDIC Center for Financial Research working paper. While it doesn't necessarily reflect the views of the FDIC, the paper includes preliminary findings from research by FDIC staff and an FDIC Visiting Scholar. On-site inspections.

The FDIC has issued an “Advisory to FDIC-insured institutions Regarding Deposit Insurance and Dealings with Crypto Companies ” to address the agency’s concerns regarding misrepresentations about FDIC deposit insurance by certain crypto companies. The first portion of the advisory addresses risks and concerns.

We witness over and over how some banks get themselves in deeper trouble booking derivatives on their books that are bets on market interest rate movements. A hedge should have a neutral outcome regardless of how the market moves (within defined bands).

We witness over and over how some banks get themselves in deeper trouble booking derivatives on their books that are bets on market interest rate movements. A hedge should have a neutral outcome regardless of how the market moves (within defined bands).

Managing loan workouts and modifications Tips for preparing your bank or credit union to handle an increased volume of problem loans while ensuring prudent credit riskmanagement. You might also like this video, "A look at credit risk in a rising-rate environment." CRE loan accommodations.

Takeaway 3 Updates on interest rate forecasting and best practices for managing CRE risk were among the most-read blogs. Abrigo's most popular riskmanagement blogs over the last 12 months cover topics that continue to catch the attention of professionals and regulators. Which credit areas need routine "maintenance"?

Measuring Interest Rate Risk Can Vary by Institution Interest rate risk measurement plays a key role in ensuring an institution's safety and soundness. Would you like other articles on asset/liability management in your inbox? FDIC) noted in its 2021 Risk Review.

Navigating interest rate management in today's environment As regulators focus on interest rate riskmanagement, read about what financial institutions can do to be ready for a rate drop. You might also like this on-demand webinar, "Navigating uncertain times: Strategies for effective riskmanagement and compliance."

Key Takeaways The FDIC issued an advisory to FIs encouraging safe and sound lending practices in today's ag lending environment. FDIC) issued an advisory to financial institutions encouraging exceptionally safe and sound lending practices in agricultural lending. On January 28, the Federal Deposit Insurance Corp.

On August 19, 2022, the FDIC issued cease and desist letters to five crypto companies, alleging they made false and misleading statements about FDIC deposit insurance and demanding immediate corrective action. According to the FDIC’s press release , “[b]ased upon evidence collected., Part 328, Subpart B.

With the assistance of the FDIC, Fulton Financial acquired certain assets, debt and deposits of Republic Bank. However, that faster growth was not unusual and reflects the bank’s higher growth markets. The bank’s failure is largely the result of a lapse in prudent management of interest rate and duration risks.

Real Estate Market Outlook. MBA Vice President for CRE Research Jamie Woodwell said in a news release that low interest rates gave CRE markets a boost last year. “In With global bond yields expected to remain extremely low and equity markets likely weaker and more volatile, the stable, solid returns of U.S.

We compared and contrasted the two strategies and sized the market for community banks. Second, community banks should use FDIC-insured institutions as hedge providers, and the hedges must be structured as qualified financial contracts (QFC). We also shared a table that summarized the two strategies.

Bankers since the financial crisis have become accustomed to seeing language like the following: “The FDIC is re-emphasizing the importance of prudent interest rate risk oversight and riskmanagement processes to ensure FDIC-supervised institutions are prepared for a period of rising interest rates.” Learn More.

In recent years, the community banks market share has been diminishing markedly as bank consolidation has occurred. FDIC-reporting institutions to include banks and savings institutions. The share of the loan market held by community banks has declined more rapidly (proportionately) than the number of charters.

Two ways in which stress testing results can be used to an institution's advantage is to avert risk and improve the risk rating process. Appraised values for properties are then adjusted by the amount of average decline in the market. In addition to preventative benefits, stress testing may provide advantages in recovery.

Takeaway 2 The severely adverse scenario from regulators presents a very severe global recession combined with severe stress in the CRE market and the corporate debt market. Prudent stress testing as a riskmanagement tool helps the enterprise see where the potential pitfalls are in their plans.

While we wrote about the root cause of the failure of Silicon Valley Bank (SVB) HERE , the lessons of the current banking crisis go beyond interest rate riskmanagement. While interest rate risk caused the most significant impact on value, several other factors contributed to the terminality of each bank that was closed.

Noninterest income associated with the housing markets such as securitization, trading, and real estate slowed significantly during the financial crisis and beyond. Noninterest income drove 20% of community banks' net operating revenue in 2019, down from 22% in 2012, according to a recent FDIC study. Portfolio Risk & CECL.

It’s also critical for reinforcing that management and the board of directors are able to receive accurate and timely updates about the health and performance of the financial institution’s portfolio. Lending & Credit Risk. Credit RiskManagement. Credit Risk Regulation. Lending & Credit Risk.

B y marketing that your financial institution offers SBA loan origination, you provide additional products that expand opportunities to businesses. During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp.

B y marketing that your financial institution offers SBA loans, you provide additional products that expand opportunities to businesses. During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp.

Community banks’ use of swaps (banks’ primary tool to hedge interest rate risk on loans) has increased substantially over the last ten years. The market expects the current inverted yield curve to remain through much of 2024 (based on long-term interest rates and the expected rate cuts in 2024). Only 304 banks (or 6.7%

Looking to mergers and acquisitions, institutions can expand into new areas of business or geographic markets. In 2008, there were 7,061 FDIC-insured commercial banks in the U.S. Lending & Credit Risk. Portfolio Risk & CECL. Cyber Complications for Vendor RiskManagement. Learn More. Asset/Liability.

As the FDIC said recently: Exceptions to policy should be few in number and properly justified, approved, and tracked. Abrigo’s credit risk software automates loan administration processes like managing ticklers and tracking loan document and credit exceptions. Get details in "A guide to implementing credit policy."

That alternative method of paying for purchases “on credit” got a boost with news this week that Visa Installments , a new point-of-sale (POS) credit solution, is being rolled out in pilot markets across the U.S. This follows a pilot rollout in Russia last month. The account comes with 1.30

according to FFIEC and FDIC data. Acquisitions allow organizations to spread costs across a larger asset base, recognize synergies within business lines, reduce staff, and consolidate branches in overlapping markets. Even though community banks make up a small share of total assets and deposits, 13.5% Background on Community Banking.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. or largely focused on the domestic banking market. We have webinars , whitepapers , and other resources to make your job easier.

The OCC, FDIC, and Federal Reserve Board have issued a guide that is intended to assist community banks in conducting due diligence when considering relationships with financial technology (fintech) companies (Guide). Financial condition and competitive market environment and client base. Legal and regulatory compliance.

The Fed, FDIC, and OCC have issued a “ Statement on Reference Rates for Loans ” that addresses replacement rates for the London Inter-Bank Offered Rate (LIBOR). The Committee is a group of private-market participants convened to ensure a successful transition from LIBOR.).

Experts have highlighted numerous lessons from Southwest’s experience, many of which can benefit bank and credit union executives, regardless of their institution size, as they manage competing priorities for spending and growth initiatives on banking solutions.

As David Barr, spokesperson for the FDIC, points out, “a vast majority of community banks remain well-rated and exhibit satisfactory corporate governance programs and compliance management systems.”. Be aware of existing or emerging risk concerns. Toney Bland, Office of the Comptroller of the Currency. in Kent, Ohio.

Today, a proper IT riskmanagement infrastructure has a direct impact on the character and value of a financial institution which places an unprecedented value on key IT employees. I would be remiss to discuss outsourcing today without mentioning vendor management.

The CFPB, Federal Reserve Board, FDIC NCUA, OCC, in conjunction with the state bank and state credit union regulators, jointly issued a statement on managing the transition away from LIBOR (Joint Statement). Fallback language.

a few agencies include the Federal Reserve (FRB), the Federal Deposit Insurance Corporation (FDIC), the National Credit Union Administration (NCUA), the Office of the Comptroller (OCC), and the Consumer Financial Protection Bureau (CFPB). Common RiskManagement Topics: Architecture, Data, IT. Infrastructure Management.

A bank with $100 million or more in total assets would be presumed to hold such a market position but could attempt to rebut the presumption by submitting written materials to the OCC demonstrating it does not hold either market position. Comments on the proposal are due by January 4, 2021.

Irvine Sprague, Former FDIC Director So Gonzo Bankers … how many of us have been hesitant lately to check our iPhone each morning to see what trouble may have hit the fan in the financial world during a few restless hours of slumber? It’s a good time to surround the executive team with a diversity of smart advisors and capital market players.

President’s Working Group on Financial Markets, which delineated perceived risks associated with the increased use of stablecoins and highlighted three concerns: risks to rules governing anti-money laundering (“AML”) compliance, risks to market integrity, and general prudential risks.

Obviously these local lenders took notice when the Federal Reserve, the FDIC and the Office of the Comptroller of the Currency recently issued a joint statement pointing out increased risks in CRE lending. The warning in December cited both growing concentrations of CRE loans and “an easing of CRE underwriting standards.”.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content