Fed, FDIC, OCC update guidance on third-party risk management

Payments Dive

JUNE 8, 2023

The guidance is aimed at helping banks address the operational, compliance and strategic risks of third-party tie-ups, such as those with fintech firms.

FDIC Operations Risk Management

FDIC Operations Risk Management

Payments Dive

JUNE 8, 2023

The guidance is aimed at helping banks address the operational, compliance and strategic risks of third-party tie-ups, such as those with fintech firms.

Abrigo

MAY 20, 2022

Meet Model Risk Management Expectations Updates to the FDIC Risk Management Manual should steer institutions toward a model that manages risk and drives growth. Takeaway 1 Aside from meeting examiner expectations, proper model risk management can protect your institution from unnecessary risk. .

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

Abrigo

FEBRUARY 25, 2025

Back-end processes for small business loan approval in some financial institutions operate in an automation desertand it shows. Without the water of automation, applications trudge along the financial analysis, risk assessment, pricing, and other processing steps like a traveler slogging through dunes. The results?

Gonzobanker

OCTOBER 31, 2024

Vendor management is risky business. The FDIC issued a consent order against Discover Bank last year for lacking oversight into third-party risk management and a compliance vendor management program. Institutions often outgrow their vendors’ ability to provide hardware to keep operations running smoothly.

Perficient

APRIL 2, 2021

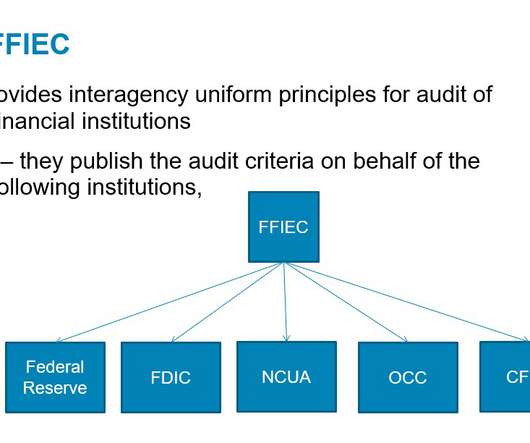

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. Risk Management. AI may be used to augment risk management and control practices.

Abrigo

MARCH 31, 2017

Commercial real estate lending continues to receive regulatory scrutiny and reminders for financial institutions to practice solid risk management. FDIC officials in March outlined several types of weaknesses in loan underwriting, administration and oversight practices that are emerging at some banks with CRE portfolios.

Perficient

AUGUST 16, 2023

A rather small bank, as of the end of its first quarter, the bank reported $139 million in total assets and $130 million in total deposits in its FDIC Call Report. Heartland Tri-State began operations in 1985 under the name First National Bank of Elkhart. bank to fail this year.

Expert insights. Personalized for you.

Let's personalize your content