This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Meet Model RiskManagement Expectations Updates to the FDICRiskManagement Manual should steer institutions toward a model that managesrisk and drives growth. Takeaway 1 Aside from meeting examiner expectations, proper model riskmanagement can protect your institution from unnecessary risk. .

The guidance is aimed at helping banks address the operational, compliance and strategic risks of third-party tie-ups, such as those with fintech firms.

Each step of back-end loan processingfinancial spreading, risk assessment, document gatheringrequires significant effort just to make incremental progress. Among large banks, 42% currently use financial technology in small business lending, compared to 30% of small banks, according to the FDIC. The results?

On the liability side of SVB’s $173B in deposits at the end of 2022, approximately 97% were uninsured and above the $250k in FDIC protection threshold. The post Silicon Valley Bank Failure – Lessons in Interest Rate RiskManagement appeared first on SouthState Correspondent Division.

Banking Trends from the FDIC's 2Q Report Net interest margin reached a new record low, but positive signs emerged in lending. Summary of the Latest FDIC Quarterly Profile. FDIC) released the latest Quarterly Banking Profile recently, and it has some helpful information on industry trends. Portfolio Risk & CECL.

The lender needs to put forth an accurate and complete picture of the borrowernot only for the borrowers sake, but also for the financial institutions riskmanagement. Kirby cited FDIC statistics showing nearly three-quarters of community banks require three or more levels of approval, regardless of the loan size.

A segmentation strategy, though, is a great place to start to nail down an effective and efficient process – not only will it serve a substantial purpose for the ALLL, but also as a larger riskmanagement tool. The goal is for the segmentation to be granular enough for the pools to show those similar loan characteristics.

Reduce approval layers According to the FDIC, 73% of banks have at least three levels of approval for small business loans. Simplify underwriting criteria and eliminate unnecessary documentation. 62% even require board approval. Removing excessive approval layers can significantly speed up loan decisioning.

Vendor management is risky business. The FDIC issued a consent order against Discover Bank last year for lacking oversight into third-party riskmanagement and a compliance vendor management program. Smart leaders use performance scorecards to keep the board informed.

In a recent Sageworks webinar Robert Ashbaugh, senior riskmanagement consultant at Sageworks, discusses High Volatility Commercial Real Estate (HVCRE) lending best practices. That 13% represented 80% of the losses to the FDIC insurance fund. How did we get here?

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. RiskManagement. AI may be used to augment riskmanagement and control practices.

Commercial real estate lending continues to receive regulatory scrutiny and reminders for financial institutions to practice solid riskmanagement. FDIC officials in March outlined several types of weaknesses in loan underwriting, administration and oversight practices that are emerging at some banks with CRE portfolios.

In various press releases, the Federal Deposit Insurance Corporation (FDIC) has highlighted that an estimated $16.3 billion of the total cost incurred from the failures of Silicon Valley Bank (SVB) and Signature Bank was designated for safeguarding uninsured depositors. Commencing with the first quarterly assessment period of 2024 (i.e.,

But the slew of banking regulatory requirements for third party riskmanagement is proving to be complex, all-consuming and expensive for both institutions and the third parties involved. In a nutshell, institutions are liable for risk events of their third and extended parties and ecosystems. " www.fdic.gov.

A rather small bank, as of the end of its first quarter, the bank reported $139 million in total assets and $130 million in total deposits in its FDIC Call Report. Mr. Herndon named the Federal Deposit Insurance Corporation (“FDIC”) as receiver, allowing the FDIC to take control of the Heartland Tri-State’s operations.

But the slew of banking regulatory requirements for third party riskmanagement is proving to be complex, all-consuming and expensive for both institutions and the third parties involved. In a nutshell, institutions are liable for risk events of their third and extended parties and ecosystems. ” www.fdic.gov.

FDIC) and the Treasury Department are looking to see if American Express Co. Representatives of the Fed, FDIC and Treasury inspectors general offices would not comment on the matter, the paper reported. Officials at the Federal Reserve, the Federal Deposit Insurance Corp. 7), citing unnamed sources. “We

Perficient provides riskmanagement to more than 500 financial services organizations, many of whom have multiple bank regulators. Often an organization will have a state-charted non-member bank, which has the FDIC as its primary federal regulator. Introduction It’s not you. It’s the guidance.

The FDIC is offering a fresh take on how a bank’s board of directors should understand and managerisk. The core principles for directors have not changed materially since 1988, the FDIC said. Riskmanagement culture What exactly is a riskmanagement culture? Evaluating riskmanagement.

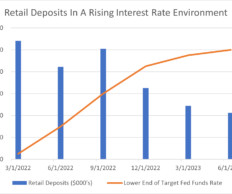

In our previous article, “ Transaction Accounts: Analyzing Deposit Stickiness in the Current Interest Rate Environment ,” Perficient’s Financial Services RiskManagement and Regulatory Capabilities Center of Excellence (CoE) explored the sharp decline in transaction account balances over an 18-month period.

More construction loan monitoring ultimately decreases loan default, according to a new FDIC Center for Financial Research working paper. While it doesn't necessarily reflect the views of the FDIC, the paper includes preliminary findings from research by FDIC staff and an FDIC Visiting Scholar. On-site inspections.

Last week, the OCC, Federal Reserve Board, and FDIC issued proposed guidance for banking organizations on managingrisks associated with third-party relationships, including those with financial technology-focused entities such as bank/fintech sponsorship arrangements. On August 6, 2021 from 12:00 p.m. to 1:00 p.m.

The Federal Reserve, FDIC, and OCC have released final interagency guidance for their respective supervised banking organizations on managingrisks associated with third-party relationships, including relationships with financial technology-focused entities such as bank/fintech sponsorship arrangements. Continue Reading

The FDIC has defined community banks in their December 2020 Community Banking Report that either exclude or include the following criteria: Seems complicated. But the FDIC did confess that a community bank was not easily defined. A big bank makes riskmanagement decisions at headquarters in a location far, far away.

Account for the details before your FDIC bank acquisition Consider these tips for assessing your institution and a to-be-acquired institution for a smooth integration You might also like this webinar, "Valuation and purchase accounting: Navigating the changing M&A landscape."

The FDIC has issued an “Advisory to FDIC-insured institutions Regarding Deposit Insurance and Dealings with Crypto Companies ” to address the agency’s concerns regarding misrepresentations about FDIC deposit insurance by certain crypto companies. The first portion of the advisory addresses risks and concerns.

Total deposits in FDIC-insured banks increased by a record $1.2 billion between January and March, data shows RiskManagement Covid19 PPP The Economy Feature Feature3 Fair Lending.

Applying model riskmanagement to CECL What's involved in CECL model validation? Learn what banks, credit unions, and others subject to CECL accounting can expect from this riskmanagement process. Model validation is a crucial aspect of model riskmanagement.

Managing loan workouts and modifications Tips for preparing your bank or credit union to handle an increased volume of problem loans while ensuring prudent credit riskmanagement. You might also like this video, "A look at credit risk in a rising-rate environment." CRE loan accommodations.

and Texas banking regulators issued consent orders against Industry State Bank, Fayetteville Bank, and Citizens State Bank requiring major overhauls of their management, capital, and risk controls. The Federal Deposit Insurance Corp.

Takeaway 3 Updates on interest rate forecasting and best practices for managing CRE risk were among the most-read blogs. Abrigo's most popular riskmanagement blogs over the last 12 months cover topics that continue to catch the attention of professionals and regulators. Which credit areas need routine "maintenance"?

This being the first blog post in a series of blogs by Perficient’s Financial Services RiskManagement and Regulatory Capabilities Center of Excellence (CoE), we will be investigating the deposit structures of non-client banks over time.

Second, the hedge provider must be an FDIC insured institution and structure its hedges as a qualified financial contract (QFC). We see substantial risk to community banks in dealing with non-FDIC hedge providers or those that do not offer QFC protection – think Lehman Brothers.

Second, the hedge provider must be an FDIC insured institution and structure its hedges as a qualified financial contract (QFC). We see substantial risk to community banks in dealing with non-FDIC hedge providers or those that do not offer QFC protection – think Lehman Brothers.

Office of the Comptroller of the Currency (OCC) & Federal Deposit Insurance Corporation (FDIC) Supervise banks and credit unions for compliance and riskmanagement related to payment systems. Consumer Financial Protection Bureau (CFPB) Regulates consumer payment protections under Reg E and related laws.

The Federal Reserve, FDIC, and OCC have released proposed guidance for banking organizations on managingrisks associated with third-party relationships, including relationships with financial technology-focused entities such as bank/fintech sponsorship arrangements. Ongoing monitoring. Termination.

Key Takeaways The FDIC issued an advisory to FIs encouraging safe and sound lending practices in today's ag lending environment. FDIC) issued an advisory to financial institutions encouraging exceptionally safe and sound lending practices in agricultural lending. On January 28, the Federal Deposit Insurance Corp.

On August 19, 2022, the FDIC issued cease and desist letters to five crypto companies, alleging they made false and misleading statements about FDIC deposit insurance and demanding immediate corrective action. According to the FDIC’s press release , “[b]ased upon evidence collected., Part 328, Subpart B.

– These are the exact words (with a couple of expletives, that I cannot quote here) – a senior fund administrator from a large investment firm uttered when we were presenting about environment aware financial riskmanagement. How does it impact me?

Second, community banks should use FDIC-insured institutions as hedge providers, and the hedges must be structured as qualified financial contracts (QFC). We see substantial risk to community banks in dealing with non-FDIC hedge providers or those not offering QFC protection – think Lehman Brothers.

Bankers since the financial crisis have become accustomed to seeing language like the following: “The FDIC is re-emphasizing the importance of prudent interest rate risk oversight and riskmanagement processes to ensure FDIC-supervised institutions are prepared for a period of rising interest rates.” Learn More.

Measuring Interest Rate Risk Can Vary by Institution Interest rate risk measurement plays a key role in ensuring an institution's safety and soundness. Would you like other articles on asset/liability management in your inbox? FDIC) noted in its 2021 Risk Review. Credit RiskManagement. Learn More.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content