This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

On the liability side of SVB’s $173B in deposits at the end of 2022, approximately 97% were uninsured and above the $250k in FDIC protection threshold. Equally important is the bank’s securities duration, as shown in the graph below. Approximately 56% of the bank’s securities had repricing greater than 15 years.

Each step of back-end loan processingfinancial spreading, risk assessment, document gatheringrequires significant effort just to make incremental progress. Among large banks, 42% currently use financial technology in small business lending, compared to 30% of small banks, according to the FDIC. The results?

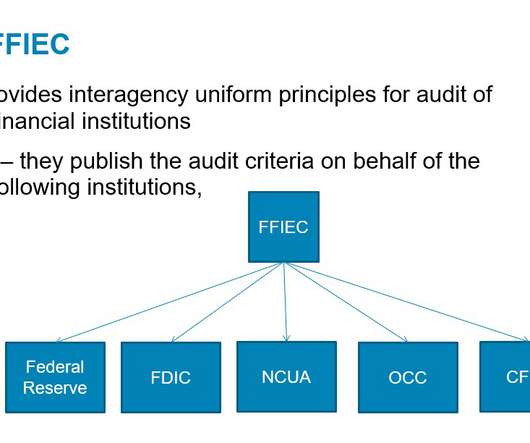

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. RiskManagement. AI may be used to augment riskmanagement and control practices.

Payment system types, trends, and fraud risks Understanding how payment systems function, the different types in use, and the associated risks is critical for financial institutions to be able to balance innovation with security. Payment systems are at the heart of modern banking, enabling secure and efficient money transfers.

A rather small bank, as of the end of its first quarter, the bank reported $139 million in total assets and $130 million in total deposits in its FDIC Call Report. Mr. Herndon named the Federal Deposit Insurance Corporation (“FDIC”) as receiver, allowing the FDIC to take control of the Heartland Tri-State’s operations.

But the slew of banking regulatory requirements for third party riskmanagement is proving to be complex, all-consuming and expensive for both institutions and the third parties involved. In a nutshell, institutions are liable for risk events of their third and extended parties and ecosystems. " www.fdic.gov.

Account for the details before your FDIC bank acquisition Consider these tips for assessing your institution and a to-be-acquired institution for a smooth integration You might also like this webinar, "Valuation and purchase accounting: Navigating the changing M&A landscape."

The FDIC has issued an “Advisory to FDIC-insured institutions Regarding Deposit Insurance and Dealings with Crypto Companies ” to address the agency’s concerns regarding misrepresentations about FDIC deposit insurance by certain crypto companies. The first portion of the advisory addresses risks and concerns.

With the assistance of the FDIC, Fulton Financial acquired certain assets, debt and deposits of Republic Bank. Even more stark was the bank’s securities repricing. We believe that such simple steps in riskmanagement may help avoid the bank failures we have seen and may continue to see.

– These are the exact words (with a couple of expletives, that I cannot quote here) – a senior fund administrator from a large investment firm uttered when we were presenting about environment aware financial riskmanagement. How does it impact me?

CRE loan growth at community banks has been outpacing noncommunity banks, both in the quarter and over the last year, according to the FDIC’s latest Quarterly Banking Profile. . “CRE Loans for life insurance companies increased 5%, and government-sponsored entity (GSE) originations fell 1%.

Steps such as multi-factor authentication have proven to be highly effective and are viewed as minimum security features for banks seeking cyber insurance. Some insurance carriers even offer discounts for banks that have additional layers of security, such as multi-factor authentication or end-point detection and remediation.

While we wrote about the root cause of the failure of Silicon Valley Bank (SVB) HERE , the lessons of the current banking crisis go beyond interest rate riskmanagement. While interest rate risk caused the most significant impact on value, several other factors contributed to the terminality of each bank that was closed.

Takeaway 2 Client fraud education at financial institutions should include takeaways that explain how to protect themselves from phishing and tips for staying secure online. While fraud detection software and robust security measures are essential, educating clients on fraud prevention is equally important.

As regulators described “practices generally considered consistent with safety-and-soundness standards,” they revised loan review guidance to reflect the broader importance of credit review to riskmanagement. Lending & Credit Risk. Credit RiskManagement. Credit Risk Regulation. Member Business Lending.

As the FDIC said recently: Exceptions to policy should be few in number and properly justified, approved, and tracked. Abrigo’s credit risk software automates loan administration processes like managing ticklers and tracking loan document and credit exceptions. Get details in "A guide to implementing credit policy."

As an example, the governor of New York State recently directed his Department of Financial Services to conduct targeted cyber security preparedness assessments for all state-chartered banks and other banks “based” in the state. Offload some of the regulatory burden related to security, technology and business continuity/disaster recovery.

The FDIC approved a final rule to increase initial base deposit insurance assessment rates by 2 basis points until the Deposit Insurance Fund (DIF) achieves the FDIC’s long-term goal of a reserve ratio of 2% of insured deposits. The FDIC’s long-term goal for the reserve ratio of insured deposits. Source: FDIC.

percent annual percentage yield (APY), an optional auto-deposit, no fees or minimums, and security as “Affirm Savings is FDIC-insured and accounts are held by our bank partner, Cross River Bank, member FDIC,’” a statement said. The account comes with 1.30

In 2008, there were 7,061 FDIC-insured commercial banks in the U.S. Mergers become a more viable option for smaller banks struggling to secure more deposits. Lending & Credit Risk. Portfolio Risk & CECL. Cyber Complications for Vendor RiskManagement. Attain growth through M&A, new partners.

During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp. The change is intended to improve security, integration, reporting features, and validation to improve accuracy. Lending & Credit Risk. Risk Ratings.

During Abrigo’s recent ThinkBIG Conference, credit underwriting and loan portfolio riskmanagement trainer and consultant Michael Wear , CRC , of 39 Acres Corp. The change is intended to improve security, integration, reporting features, and validation to improve accuracy. Lending & Credit Risk. Risk Ratings.

The OCC, FDIC, and Federal Reserve Board have issued a guide that is intended to assist community banks in conducting due diligence when considering relationships with financial technology (fintech) companies (Guide). Riskmanagement policies, processes, and controls. Information security program and information systems.

according to FFIEC and FDIC data. Additionally, community financial institutions are more likely to leverage relationship lending to help smaller businesses obtain loans that they might not be able to secure with larger institutions based solely on their financial information. Digitalization.

The following steps are expected of FIs: Maintain an information security program and risk assessment, Monitor Internet traffic to your website in order to detect an attack (establish a baseline so you can easily discern an increase in activity). Ensure adherence to appropriate patch management policy and procedures.

The Fed, FDIC, and OCC have issued a “ Statement on Reference Rates for Loans ” that addresses replacement rates for the London Inter-Bank Offered Rate (LIBOR). The agencies stress that banks should include fallback language that provides for the use of a “robust fallback rate” if the initial reference rate is discontinued.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. Using Data to Acquire, Engage, and Retain Banking Customers,” and “Customer Identity: Balancing Security and Seamless Banking Experiences.”

Saving money by conducting inside riskmanagement and compliance reviews. As a group, community banks spend substantial funds hiring outside consultants to help with various management functions, and a substantial share of dollars are spent to help oversee their riskmanagement and compliance activities.

Already, community banks have a leg up over digital-platform lenders in funding stability; the new lenders cannot match the security of a traditional depository’s core deposit base. Marketplace-driven digital-platform lenders are also structured so that credit risk is held by the investor funding the deal.

This leads to many generations of installed technology sets with diverse hardware and software systems, all that need to be tracked and managed, secured, and audited. Regular external examination is a necessary challenge to ensure hygiene of these systems are maintained amidst a backdrop of increasing cyber risk. In the U.S.

But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent riskmanagement practices. Using FDIC data for 2021, we calculated a lender score out of 100 for each community bank. Security Bank Midwest. Security Bank. By Ed Avis.

We have investigated the matter thoroughly, addressed the cause and, as a precaution, have implemented additional security measures,” Macy’s said in an emailed statement. Macy’s was able to confirm that social security numbers were not accessed — but that data like birthdays and addresses might have been.

Previewing an easier-to-use format of the FFIEC’s IT security assessment. Bad news: In its original form, it’s awkward to use—and may become part of those dreaded IT security exams. Risk levels have a five-point range. For example: Who manages each piece? How is it secured? By Ellen Ryan.

Previewing an easier-to-use format of the FFIEC’s IT security assessment. Bad news: In its original form, it’s awkward to use—and may become part of those dreaded IT security exams. Risk levels have a five-point range. For example: Who manages each piece? How is it secured? By Ellen Ryan.

One of the biggest problems with FinTech companies is that many of them exploit existing banking infrastructure—including debit, credit and ACH networks—and access traditional checking and saving accounts, yet face minimal regulation when it comes to data security and privacy. These insights emulate relationship banking.

To obtain supervisory non-objection, a bank must demonstrate in writing that it understands any relevant compliance obligations, including under the Bank Secrecy Act, federal securities laws, the Commodity Exchange Act, and consumer protection laws.

Both the Securities and Exchange Commission (SEC) and the Department of Justice (DOJ) have officially ended a two-year investigation of LendingClub, its subsidiary LC Advisors (LCA), its founder and former CEO Renaud Laplanche and its former CFO Carrie Dolan. On Friday (Sept. The DOJ Finding.

And quite frankly, I did not know there were so many tranches to mortgage-backed securities. According to the FDIC, the causes of the 2008-09 financial crisis lay partly in the housing boom and bust of the mid-2000s; partly in the degree to which the U.S. We took a serious reputational hit. credit default swaps anyone?). Good times.

So we want our checking accounts to be FDIC insured. IB: Community bankers are the world’s best riskmanagers. How should they balance innovation with their need to managerisk? Linkner: People think it’s either take no risk or innovate. I think taking no risk and not innovating is hugely risky.

In 2005, the federal prudential regulators—including the Board of Governors of the Federal Reserve System (Federal Reserve), Federal Deposit Insurance Corporation (FDIC), and Office of the Comptroller of the Currency (OCC)—issued Interagency Guidance on Response Programs for Unauthorized Access to Customer Information and Customer Notice.

Consumer lending compliance — like other aspects of enterprise riskmanagement at financial institutions — saw a huge impact from the COVID-19 pandemic. Numerous regulatory resources go into detail, including fair lending videos from the FDIC and examination procedures published on the Consumer Financial Protection Bureau’s website.

The Federal Reserve, FDIC, and OCC should finalize the interagency guidance for banks on managingrisks associated with third-party relationships that was proposed in July 2021. This includes IDIs acting as lenders in bank/fintech partnerships.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content