This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Each step of back-end loan processingfinancial spreading, risk assessment, document gatheringrequires significant effort just to make incremental progress. Among large banks, 42% currently use financial technology in small business lending, compared to 30% of small banks, according to the FDIC. The results?

The lender needs to put forth an accurate and complete picture of the borrowernot only for the borrowers sake, but also for the financial institutions riskmanagement. Kirby cited FDIC statistics showing nearly three-quarters of community banks require three or more levels of approval, regardless of the loan size.

Banking Trends from the FDIC's 2Q Report Net interest margin reached a new record low, but positive signs emerged in lending. Summary of the Latest FDIC Quarterly Profile. FDIC) released the latest Quarterly Banking Profile recently, and it has some helpful information on industry trends. Portfolio Risk & CECL.

Reduce approval layers According to the FDIC, 73% of banks have at least three levels of approval for small business loans. Leverage automation: smarter loan decisioning through technology The key to faster, more efficient loan decisioning is automation. Simplify underwriting criteria and eliminate unnecessary documentation.

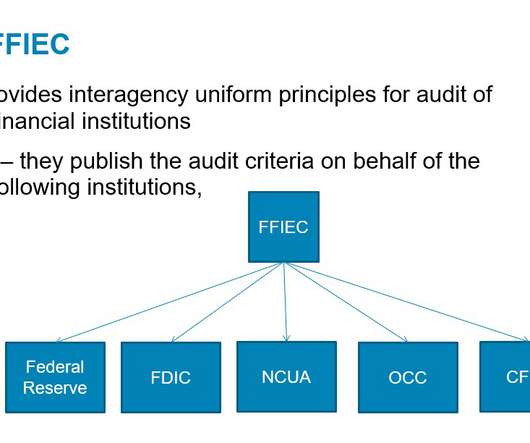

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. RiskManagement. AI may be used to augment riskmanagement and control practices.

Vendor management is risky business. The FDIC issued a consent order against Discover Bank last year for lacking oversight into third-party riskmanagement and a compliance vendor management program. Smart leaders use performance scorecards to keep the board informed.

Perficient provides riskmanagement to more than 500 financial services organizations, many of whom have multiple bank regulators. Often an organization will have a state-charted non-member bank, which has the FDIC as its primary federal regulator. Introduction It’s not you. It’s the guidance.

Banking technology decisions now affect future growth With the possibility of a recession, community financial institutions may consider a delay or cut in technology spending. Takeaway 2 According to Forrester data, firms pursuing technology-driven innovation grow three to four times faster than industry averages.

A rather small bank, as of the end of its first quarter, the bank reported $139 million in total assets and $130 million in total deposits in its FDIC Call Report. Mr. Shan Hanes, who served as the bank’s President and CEO until its closure, joined the firm in 1993 as an agricultural loan officer and Informational Technology Officer.

The FDIC is offering a fresh take on how a bank’s board of directors should understand and managerisk. The core principles for directors have not changed materially since 1988, the FDIC said. Riskmanagement culture What exactly is a riskmanagement culture? Evaluating riskmanagement.

Last week, the OCC, Federal Reserve Board, and FDIC issued proposed guidance for banking organizations on managingrisks associated with third-party relationships, including those with financial technology-focused entities such as bank/fintech sponsorship arrangements. On August 6, 2021 from 12:00 p.m. to 1:00 p.m.

The Federal Reserve, FDIC, and OCC have released final interagency guidance for their respective supervised banking organizations on managingrisks associated with third-party relationships, including relationships with financial technology-focused entities such as bank/fintech sponsorship arrangements.

Financial institutions are responsible for not only facilitating payments but also managing risksincluding fraud, compliance, and operational challenges. Consumer Financial Protection Bureau (CFPB) Regulates consumer payment protections under Reg E and related laws.

Key Takeaways The FDIC issued an advisory to FIs encouraging safe and sound lending practices in today's ag lending environment. Technology has been a key resource for both ag borrowers and ag lenders seeking efficiency, growth, and profitability. Leverage technology to mitigate risk and gain efficiency. Learn More.

The Federal Reserve, FDIC, and OCC have released proposed guidance for banking organizations on managingrisks associated with third-party relationships, including relationships with financial technology-focused entities such as bank/fintech sponsorship arrangements. Ongoing monitoring. Termination.

according to FFIEC and FDIC data. Technology is an obstacle and an opportunity. One key area that can be both an obstacle and an opportunity for community banks is technology, the Federal Reserve Bank of Kansas City says. Additionally, technology isn’t just reserved for the biggest banks anymore. Digitalization.

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Many financial institutions implemented or upgraded technology to help them offer PPP loans during the pandemic. Looking to Increase SBA Loan Origination? Want other articles like this on SBA loan origination in your inbox?

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Many financial institutions implemented or upgraded technology to help them offer PPP loans during the pandemic. Looking to Increase Loans through the SBA? Would you like others articles like this in your inbox?

Due to new and emerging technologies, changing regulations, and ever-evolving customer expectations, banks and credit unions across the country are taking an assortment of different strategies to achieve their growth goals in 2020. In 2008, there were 7,061 FDIC-insured commercial banks in the U.S. Lending & Credit Risk.

FDIC-reporting institutions to include banks and savings institutions. We feel that the community bank industry consolidation is not explained by scale, regulation, or access to technology or employees. Community Bank Consolidation As of Q3/24 there were approximately 4.5k The number of U.S.

Fraud schemes, evolving with technology, are more sophisticated and more complex to detect. Fraudsters have adjusted their tactics as technology has changed. Effective fraud riskmanagement includes detection and fraud monitoring that should consider customer or member history and behavior.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. So far, episode topics include cover loan pricing in a rising-rate environment, cannabis-related banking , and technology implementation.

The OCC, FDIC, and Federal Reserve Board have issued a guide that is intended to assist community banks in conducting due diligence when considering relationships with financial technology (fintech) companies (Guide). Riskmanagement policies, processes, and controls. Legal and regulatory compliance.

Today, a proper IT riskmanagement infrastructure has a direct impact on the character and value of a financial institution which places an unprecedented value on key IT employees. As our economy strengthens, this concern for the future roles of CIOs, CTOs, CISOs, and Heads of Technology grows.

Saving money by conducting inside riskmanagement and compliance reviews. As a group, community banks spend substantial funds hiring outside consultants to help with various management functions, and a substantial share of dollars are spent to help oversee their riskmanagement and compliance activities.

In what could be an important step towards needed regulatory updating to accommodate the growing use of artificial intelligence (AI) by financial institutions, the CFPB, FDIC, OCC, Federal Reserve Board, and NCUA issued a request for information (RFI) regarding financial institutions’ use of AI, including machine learning (ML).

As a key provider of technology for mission-critical financial system infrastructures across the globe, Cisco is held to the highest levels of scrutiny in the financial services regulatory audit chain. A key challenge is managing iterations of infrastructure in global financial enterprises which have spanned 50+ years of digitization.

Community banks cannot afford to ignore the staggering pace of lending adoption by both individuals and businesses using digital-only platforms from various nonbank technology-based specialty lending firms. Marketplace-driven digital-platform lenders are also structured so that credit risk is held by the investor funding the deal.

Regardless of the name, nonbank technology firms are wedging themselves between community banks and their customers by offering a slew of traditional and nontraditional banking products. FinTech customers have no idea they are exposing themselves to identity and financial risk. By Kelly Pike. Siphoning customers.

Heated competition for bank funding is an increasingly important focus for community bank leaders, according to an annual survey released today by the Federal Reserve, the FDIC and the Conference of State Bank Supervisors. The post Survey Finds Cost of Funds Top of Mind for Community Bankers appeared first on ABA Banking Journal.

“I spend 30 to 40 percent of my day looking at those monitoring tools to keep up with cybersecurity threats, though some of that is multitasking,” says Mike Hamilton, vice president, information technology at the $250 million-asset First State Bank in Huntington, W.Va. Risk levels have a five-point range.

“I spend 30 to 40 percent of my day looking at those monitoring tools to keep up with cybersecurity threats, though some of that is multitasking,” says Mike Hamilton, vice president, information technology at the $250 million-asset First State Bank in Huntington, W.Va. Risk levels have a five-point range.

But allowing branches to operate at losses takes resources away from areas that need immediate resources, such as technology acquisition and deployment. So they worry about other things that go beyond the fact that their branch in that market has little chance of being profitable. Idea : Develop objective analyses for entering markets.

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. The DOJ Finding. Attorney Alex Tse.

To remind readers, in 2006 the OCC, Federal Reserve, and FDIC issued joint interagency Guidance on Concentrations in Commercial Real Estate Lending. Risk mitigants tend to lag growth, especially fast growth. And success is the great mollifier to riskmanagers that wish to take away the punch bowl when the party's rockin'.

According to the FDIC, the causes of the 2008-09 financial crisis lay partly in the housing boom and bust of the mid-2000s; partly in the degree to which the U.S. According to the FDIC, the causes of the 2008-09 financial crisis lay partly in the housing boom and bust of the mid-2000s; partly in the degree to which the U.S.

But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent riskmanagement practices. Using FDIC data for 2021, we calculated a lender score out of 100 for each community bank. Rowland; and EVP and chief technology officer Mike Beattie.

As a four-time technology entrepreneur, Linkner has walked the innovation walk. As a New York Times bestselling author on business creativity and technology innovation, he’s now talking about the walk. So we want our checking accounts to be FDIC insured. We don’t want to have missteps in technology.

Going forward, US payments players have reason for concern, as consumers and merchants could be wooed by technology-first options with fewer middlemen. Virtually all US private sector wage earners receive wages into bank accounts, according to the Global Findex database, which are insured by the FDIC and offer an easy way to earn interest.

That Order directed the Secretary of the Treasury to issue a report assessing how the entry of large technology firms and other non-banks into consumer finance markets has affected competition. The report was issued in response to President Biden’s July 2021 Executive Order on promoting competition.

The letter was conditioned on Upstart’s agreement to a model riskmanagement and compliance plan that required it to analyze and address risks to consumers, and assess the real-world impact of alternative data and machine learning. Both task forces held their first meetings in June.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content