This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

How to prevent internal fraud at your bank or credit union Of the many fraud risks banks and credit unions face, one of the most costly comes from within the institution itself. ACFE reported that 5% of an organizations revenue is lost to internal fraud each year, with an estimated $3.1 billion in total losses.

Wire fraud is the second highest fraud scam impacting financial institutions As fraudsters continue to refine their tactics, financial institutions must remain vigilant to protect both their clients and employees from evolving wire fraud schemes. Understanding wire fraud is the first step to preventing it.

To support debit card operations, a bank gets charged a myriad of transaction charges and maintenance fees from the card rails (Visa, Mastercard, Discover, etc.), Materials, training, and fraud also contribute to bank expenses. the network (Interlink, Pulse, Shazam, etc.) and the bank’s processor (usually their core).

By being proactive, banks can safeguard themselves from regulatory penalties and ensure their operations align with evolving compliance standards. Provide for program continuity despite operations, management, employee composition, or structure changes. Provide timely updates in response to changes in regulations.

Artificial intelligence (AI) is transforming fraud prevention AI offers financial institutions a way to reduce false positives, detect fraud faster, and improve suspicious activity monitoring. Staying on top of fraud is a full-time job. Let our Advisory Services team help when you need it.

A couple of weeks ago, we delved into the origination and operating costs of manufacturing commercial loans ( HERE ). In addition, this cost segment includes the cost of pursuing fraud and negative balance management. In this article, we delve into deposit profitability and highlight the cost structure of deposits. Interest Cost.

Takeaway 2 It's important to review resources on how to prepare for FedNow and also look internally to create a plan for your unique financial institution. Fraud detection and AML systems: Ensure these systems are integrated and operational at your institution to stay on top of financial crime.

But in a new PYMNTS discussion between Karen Webster and Fang Yu, CTO and co-founder of DataVisor , the two of them step further into that world than is often the case, offering not only the latest information about the digital fraudster mindset, but the latest guidance about how to defeat such criminals. Criminal Rings. Criminal Patience.

The basics of counterfeit check detection for banks and credit unions Check fraud is surging and technology advances aren't helping. The ABA Banking Journal reports that check fraud could reach a staggering $24 billion in losses in the U.S. this year, making up 60% of all attempted fraud.

Transaction monitoring in financial institutions Financial institutions operate in an environment where even the slightest data discrepancies can create outsized risks. Staying on top of fraud is a full-time job. This could put your institution at regulatory and reputational risk. What is transaction monitoring?

With this regulatory risk and associated operational complexities, there is plenty for financial institutions to consider before diving into cannabis lending. Abrigos new fraud detection software for banks and credit unions finds more fraud faster. But what about lending? billion year-over-year in 2024, totaling $31.4

The only question is how banks can ensure that they are employing the best strategies to apply them. I n How To Put AI In Your 2021 Business Plan Playbook , PYMNTS and Brighterion collaborate to provide a blueprint of how financial institutions (FIs) can incorporate AI into their consumer credit strategies.

Prevent fraud when adopting FedNow Credit unions can prevent fraud as they connect to FedNow. Use this guide to understand available tools and the steps AML and fraud teams should take. You might also like this FedNow implementation guide with details on appropriate AML/CFT and fraud considerations.

He and Nitendra Rajput , Mastercard’s vice president of product development and head of the company’s “AI Garage,” said that in many cases, AI is the only way to scale up sufficiently to meet the challenges the company faces with fraud and other business issues. “It Fighting Fraud in a Post-Pandemic World.

Telecommunications companies face a number of challenges in their day-to-day operations, however. Onboarding these customers can be a tedious challenge prone to fraud and consumer frustrations, and the industry faces the ever-looming threat of SIM swap fraud. SIM Swap Fraud Plagues Smartphone Users.

Stay up-to-date on AI fraud trends to protect your clientele Emerging AI fraud schemes reveal holes in financial institution's defenses. Takeaway 2 Improving security questions is a good step to take to avoid text-to-speech AI fraud schemes. Here are several suggestions for tightening security.

Key topics covered in this post: Requirements for Regulation E compliance How to avoid fines and reputational harm What is Regulation E? This increased scrutiny can divert resources away from core operations and impact overall efficiency.

Roughly 300 people signed up for a corresponding “masterclass” for the market in January, which taught them how to set up eWallets and explore the margin-trading strategies available. For this reason, it’s difficult to ascertain exactly how much trading is done.

In the old days, forged checks were the biggest problems that bank fraud departments had to manage. Today, financial institutions (FIs) face a barrage of cyberattacks from hackers operating around the world, continuously shifting their tactics. Yet, few FIs leverage this technology in their anti-fraud efforts — only 5.5

The most popular financial crime blogs in 2023 Check fraud, the SAFER Banking Act, and BSA exam topics were among Abrigo's top blogs on AML/CFT and fraud this year. You might also like this infographic on the true costs of fraud at financial institutions. Here are Abrigo’s 10 top AML and fraud blogs in 2023.

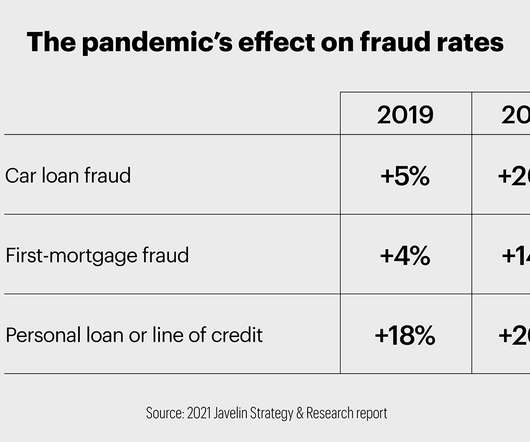

Measuring the cost of fraud losses. The true cost of fraud goes beyond the initial reported fraud losses Would you like other articles like this in your inbox? Takeaway 1 Fraud scams made worse by the pandemic continue to be successful, while crypto-scams are emerging. That equates to $35 billion annually.

Internet bank fraud is here to stay; learn how to detect and stop it. Every type of fraud has something unique it leverages to dupe unsuspecting citizens. Learn what is different about internet bank fraud. Takeaway 1 It is important to monitor fraud effectively and consistently.

“Once a business solves its digital transaction processing issues, they need to start considering how to efficiently and effectively go global. Noting that some countries are able to operate more normally now than the U.S., The world economy won’t wait for the U.S. to recover.”. The world economy won’t wait for the U.S. to recover.

consumers, for instance, want the right to know where their personal data is and how it’s being used, according to recent surveys. Meanwhile, to help along some of the companies that are still confused about how to comply with GDPR and PSD2, the European Data Protection Board (EDPB) has issued regulatory guidance on the topic.

But newer technologies on the market are making it more difficult for everyone to get on the same page about how to use the tool. APIs can certainly be used for a virtually limitless list of use-cases, but NACHA’s Industry Group will be examining how to standardize APIs for financial services providers to enhance faster payment capabilities.

The phenomenon of payments fraud is not a modern one — far from it. But as RL Prasad, SVP of payment system risk at Visa , told Karen Webster in a recent conversation, what is new today is the who and the how of fraud, particularly in a digital world.

Here’s a test: What’s fraud? Those questions also speak to the seemingly impossible tension in the world of payments and new card accounts: how to onboard and authenticate consumers as quickly and seamlessly as possible, while also protecting them and the institution from fraud. Fraud Getting Worse. Bad Timing.

Avoid fraud losses from pig butchering scams FinCrime professionals looking to prevent pig butchering scams in the age of cryptocurrency can follow these steps to tighten security. Takeaway 1 Investment fraud schemes known as pig butchering scams contributed to $3.3 billion in fraud losses in 2022. billion in 2021.

Most-read blogs on financial crime in 2022 Synthetic ID fraud, AML quality control, and SAR writing topics were among Abrigo's top blogs on AML/CFT and fraud this year. . Takeaway 1 AML/CFT and fraud professionals often keep up to date on industry trends by reading Abrigo's blog. The blogs your FinCrime peers are reading.

The holidays aren't always so cheery as the risk of fraud plagues consumers and retailers alike. With the pandemic accelerating a surge in eCommerce volumes, online fraud threats are at their peak, and everything from chargeback fraud to online product scams are dampening the holiday spirit. Corporate-Facing Fraud.

One day — maybe one that has already happened for some PYMNTS readers — we might look back with fondness and nostalgia on that time when chargebacks stood as the main worry merchants and other organizations faced when it came to fraud and risk. That’s where Kevin Lee comes in. Changing Scope. The stakes could hardly be higher. Insult Rate.

How offering FedNow instant payments affects fraud & AML/CFT compliance What financial crime staff can do to prepare fraud and AML functions for implementing the FedNow Service for instant payments. Would you like other articles on fraud and AML/CFT compliance in your inbox? Instant payments service What is FedNow?

Consumers are using mobile apps’ order-ahead features and loyalty perks more often during the COVID-19 pandemic, yet chargeback fraud — also known as friendly fraud — is unfortunately also rising. Mobile ordering is at the center of business operations for Blaze Pizza and many fast casual dining chains today.

That’s where the persistence of manual fraud review process can be a problem, said Carl Tucker, vice president of risk solutions at CyberSource , a Visa solution, in a recent conversation with PYMNTS. There is no such thing as manual fraud review on a burrito sale because there is no context in which it could ever be usefully applied.

But those illegal marketplaces — often called the “Dark Web” — also present a juicy opportunity for those fighting fraud to detect and even preempt criminal activities than cost businesses revenue and, often, parts of their brand reputation. As he sees it, “credit card fraud is the slush fund for much worse stuff.”.

But reaching a broader range of consumers, accommodating their payment preferences, and satisfying regulatory and tax issues in unfamiliar territory introduces a host of new operational challenges for these companies. The ultimate goal,” he told PYMNTS, “is the highest acceptance rate with the lowest fraud possible.”.

You might also like this webinar: "Detecting PPP Fraud: Optimizing Your AML Solution". Takeaway 1 To prevent the kind of fraud that plagued the Paycheck Protection Program in 2020, the SBA has put new measures in place that have created challenges. PPP fraud-prevention challenges arise. New Guidance Out. mail, Craig said.

But success cannot come without stumbles, and as Akli Adjaoute, CEO of Brighterion (a Mastercard company) discusses with Karen Webster, the lessons learned by AI failure – and how those shortcomings and mistakes could lead to future gains in customer service, fraud prevention and revenue growth. Data Concerns.

However, digital platforms face a major barrier in delivering these experiences: poor fraud detection. For digital platforms, fraud represents a two-headed beast. As largely online operations, they are tempting targets for fraudsters and hackers — therefore, robust anti-fraud systems are vital. About the Playbook.

They face the challenge of offering customers a smooth onboarding process while also remaining rigorous in know your customer (KYC) efforts, taking care to remain compliant with local anti-money laundering (AML) regulations that aim to keep criminals from using legitimate operations to move money illegally. In the U.K.,

As more customers moved online, fraudsters took advantage of new and increasingly inventive opportunities to commit remote authentication fraud. These types of scams fall under the broad term of remote authentication fraud, and they’re increasingly common—and inventive. Examples of remote authentication fraud. New account fraud.

The creation of digital IDs also has the beneficial effect of helping governments and companies combat financial fraud and money laundering activities. But, in an interview with Karen Webster, Zac Cohen, chief operating officer at Trulioo , cautioned against a “one-size-fits-all” approach to the digital identity space. The Micro Level.

Jurisdiction is always a few steps behind, though — who is really going to bust down the door at a server farm in Russia to arrest the operator? In a way, the world has entered a new era of fraud (and fraud prevention). He described the current era as “Fraud 3.0.”. What does that mean in real terms?

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content