This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When it comes to deploying corporate resources in the battle against online fraud and account takeovers (ATOs), all too often, guiding principles fail to spot what’s really happening to a business in real time. The rule of thumb here is that after committing account takeover fraud, those fraudsters lie in wait before using the stolen account.

He added that payment service providers (PSPs) and payment operators have worked diligently “to create both critical mass and pan-European reach.” . A pan-European request to pay solution is considered “missing piece of the puzzle” for real-time payment services, according to an EBA whitepaper. “As

In a new PYMNTS interview, David Barnhardt, executive vice president of product at GIACT , which offers fraud detection and account validation tools, talks about an upcoming change by NACHA, national administrator of the ACH network, to make internet-initiated debit transactions (WEB debits) safer and more seamless. New NACHA Rule.

Late this month, a study from Nexus found that across 200 businesses surveyed, more than half of large and mid-sized companies queried are looking to adopt blockchain in an effort to mitigate operational risks in the wake of Brexit. As reported in July via whitepaper, the U.K.

Russia’s FinTech Association and 14 of the nation’s largest banks collaborated on the development of Masterchain, reports noted, citing a whitepaper. Using Masterchain will reduce operating costs by up to five times, the whitepaper claims, and will accelerate contract processing.

As most operations have shifted to a digital-first world due to the coronavirus pandemic, institutions have had to adjust and adapt new technologies to stay competitive and thrive during these times. We understand the trust you put in us when you use our BSA/AML and fraud software and we make the same investment in your program’s success.

The operator then purportedly moved to a laundering and reimbursement scam that led to the U.S. The whitepaper of Banana.Fund discussed a business development firm that helped burgeoning upstarts across the beginning phases and provided those who put up the early investments with transparency.

Between account takeovers, business logic abuse, loyalty and reward points fraud and other cybersecurity attack methods, companies are not only suffering financial damages but brand image damages too. Here are a few of the top things every eTailer should know about fraud in 2017. Card Not Present Fraud Is A Big Threat.

The recent fascination with artificial intelligence and machine learning has made some of us ( naturally intelligent) humans confused about the role that these technologies play in the broader field of fraud analytics. In this blog post, I explain their usage and particularly how they will operate in the open banking revolution.

The recent fascination with artificial intelligence and machine learning has made some of us ( naturally intelligent) humans confused about the role that these technologies play in the broader field of fraud analytics. In this blog post, I explain their usage and particularly how they will operate in the open banking revolution. .

Recently, IDC published a whitepaper, sponsored by IBM, outlining the ten hard realities that FIs and payments services providers must overcome to benefit from modernization, and how they can turn these perceived threats into opportunities. Cost savings are possible as operations become more efficient.

A new independent survey by research firm Ovum has found that banks in multiple regions plan to integrate their fraud and financial crime compliance systems and activities in response to new criminal threats and punishing fines — but not all at the same speed. said TJ Horan, vice president of fraud solutions at FICO. South Africa.

In a world where convergence is coming faster than any whitepaper can articulate, O’Connell said it’s more important than ever for payments players to ensure their payments networks are responsible, safe, secure and fair. When you have that consortium data, fraud becomes much easier to manage and stay ahead of,” O’Connell noted.

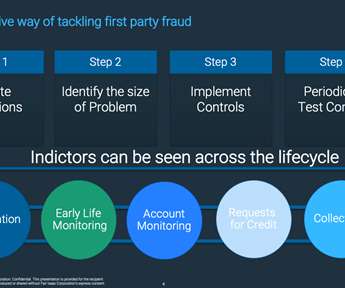

What Is First-Party Fraud? From banks to telcos to debt collection agencies, what looks like unrecoverable bad debt may in fact be first-party fraud. For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. by Matt Cox.

In 2016, corporate banking made up 38 percent of overall operating income across 20 of the world’s largest banks,” explained Patricia Hines, senior analyst at Celent, in a statement. Regardless of FinTechs and the solutions banks choose to deploy, Finastra and Celent emphasized the importance of integration.

Fraud management and AML compliance are both about tackling financial crime, but often they are managed by different teams, each with their own processes and technology. It’s also true that fraudsters do not operate in siloes when they transfer the money from their frauds into cash by laundering it through a network of money mules.

For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. Perhaps surprisingly, consumers sometimes use their own personal information to commit fraud. Both of these crimes are first-party fraud.

Recently, IDC published a whitepaper, sponsored by IBM, outlining the ten hard realities that FIs and payments services providers must overcome to benefit from modernization, and how they can turn these perceived threats into opportunities. Cost savings are possible as operations become more efficient.

The platform enables customizable, real-time scoring and evaluates thousands of transactions per hour in order to produce scores and decisions on fraud, credit, operations, and marketing in an instant and at scale via Web-based APIs. contact-form-7].

Digital banking channels are increasingly popular, and behavioral profiling of customers is vital in preventing new types of fraud. The open banking revolution makes understanding each customer’s behavior even more important in preventing fraud by considering all the aspects of transactions. Understanding Recurring Behavior.

This is a guest blog from Jonathan Williams , an expert in payments, identity and fraud prevention, working for advisory firm Mk2 Consulting. In July, the European Banking Authority (EBA) published their guidelines for reporting fraud under Payment Services Directive 2 (PSD2).

When it comes to fraud detection and prevention, for example, big data analytics tools can offer banks much better, real-time insight into potentially fraudulent transactions. A few key use cases for big data have been around for some time. But let’s not underestimate the potential that technology brings forth.

All of the speakers stressed the need for companies to identify potential sources of risk in their operations and attempt to address those risks in advance. Roddy discussed the emergency debt collection regulation issued by the Massachusetts AG and the possibility of state UDAP claims based on collection activities during the crisis.

In my previous post , I described how fraud analytics for open banking work. Following an introduction to behavioral analytics , this post focuses on how the data refined through behavioral profiles are combined in an unsupervised machine learning model to produce a score indicative of fraud or non-fraud. Learn More.

We project that by providing FCI clients access to a plethora of modern tools, we will help them scale their financial crime prevention operations and reduce IT-associated costs and hassles by extending existing cloud capabilities.

When today’s businesses create a list of must-haves in the race to alter and ultimately transform how they operate, machine learning is one of those checkbox necessities. This combination can literally reshape how businesses operate. What’s machine learning, and why is it needed?

This same process can be used across a very diverse set of business engagements, including new customer on-boarding or loyalty programs, detecting and mitigating fraud throughout your business, inventory or supply chain management, pricing and packaging, and frankly across virtually every business process application.

He indicated that Mr. Uejio’s prior experience at the CFPB has allowed him to become well-versed not only in operational issues such as personnel and budget but also as to policy issues. Cordray shared his thoughts on how each of them is likely to approach his new role at the CFPB.

JP Morgan’s fine highlights the broader problem that many global banks had been facing, which was ignoring the warning signings of fraud and money laundering. This tool demonstrates AI’s transformative benefits in anti-money laundering (AML) and fraud detection. This post originally appeared on the SIIA blog.

Mobile Operators and Coronavirus: Ideas To Help Slow The Spread. Mel Prescott noted several ways that mobile operators could use their network data to potentially help fight the virus. For more information on this topic, read our whitepaper on Agile Decisioning in an Unprecedented Downturn. #5.

These include falling consumer retention figures, as app transaction abandonment rates increase; the cost of developing and maintaining mobile apps; ensuring adequate security for accurate billing and fraud prevention; and meeting regulations such as PSD2.

Download our latest whitepaper that discusses what it really takes to develop a successful Fintech startup. This is a very sophisticated fraud detection technology! ^SR. Silver 6 operates as Software as a Service (SaaS), so that means no IT and no infrastructure required. ^SR. Showing really good dashboard on threats.

03:04 pm Experian Fraud & Identity – https://www.experian.com/decision-analytics/identity-and-fraud/fraud-and-identity.html – @Experian – Adam Fingersh – GM and SVP, Fraud and Identity Solutions & John Sarreal. operation of Russian-based company. Reminds me of Amex real time alerts.

Diana Chin (HR & Operations). Started talking about the challenge of having to change credit cards all the time (due to fraud). We are the global leaders in identity solutions while protecting FI’s and providers from compliance and fraud.” This is a very sophisticated fraud detection technology! ^SR. Virtual reality?

I like the idea but I am a bit concerned about the potential for fraud from both companies and investors. Addresses compliance, fraud experience and customer experience analytics. users fall victim to fraud.” Juvo makes it easy for mobile operators to find them. Download: 10 Reasons Why Fintech Startups Fail WhitePaper.

If history is even a rough guide to the future, you can bet that some of the case studies, technology and techniques gained from what promises to be a major operational effort will make their way into the payments and commerce mainstream — which, of course, has its own daily issues with data breaches, hackers, fraud and authentication.

Note for you damn haters: yes, it’s down from a frothy high of $66,0000, but look at the normalized return over the past 15 years since Satoshi Nakamoto’s whitepaper.) The Holy Crap Operational Risk Award – goes to the growing threat of ransomware with bank technology vendors. The poor payroll and benefits coordinator!

Companies are turning to accelerators, funds, and labs to try to find the next big thing that will reduce fraud, speed up transaction times, and catch on with consumers. DBS leaders expect to see more than 5,000 people actively innovating DBS’ services and operations at DAX each year. FIS Global — FIS Innovation Lab.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content