This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

There are countless potential benefits to adopting the technology,” said animal safety company Neogen CEO John Adent. A blockchain system can also attack fraud in the food business. Blockchain can serve to optimize the entire supply chains of many of the markets that Neogen serves.”.

As noted by Nexus, about 33 percent of firms said they will use blockchain to combat fraud, while 11 percent will use blockchain to help cut costs, and 10 percent see blockchain as useful in supply chain management. As reported in July via whitepaper, the U.K.

This is the fifth in my series on five keys to using AI and machine learning in fraud detection. For continual performance improvement, fraud detection professionals should consider adaptive technologies designed to sharpen responses, particularly on marginal decisions. What Do You Need Besides the 5 Keys? But that’s not enough.

Getting there is a long road with many twists and turns, with guidance provided not only by back-end technology but also by updated rules from organizations with a governing role across the payments industry. The rule change is the subject of a recent whitepaper published by GIACT. New NACHA Rule.

Russia’s FinTech Association and 14 of the nation’s largest banks collaborated on the development of Masterchain, reports noted, citing a whitepaper. Using Masterchain will reduce operating costs by up to five times, the whitepaper claims, and will accelerate contract processing.

There certainly is room for improvement, according to the whitepaper, as middle market companies, which are defined as those with annual sales below $500 million, spend an estimated $7.8 Firms have tread cautiously with respect to electronic payments, with costs dominating the argument against transitioning.

As most operations have shifted to a digital-first world due to the coronavirus pandemic, institutions have had to adjust and adapt new technologies to stay competitive and thrive during these times. We understand the trust you put in us when you use our BSA/AML and fraud software and we make the same investment in your program’s success.

The retail merchant marketplace is an ever-changing landscape — and new technologies and evolving consumer preferences are forcing the space to change faster than ever before. In its latest whitepaper, titled “Omni-Channel Payments for Merchants: Myth or Reality?,”

Between account takeovers, business logic abuse, loyalty and reward points fraud and other cybersecurity attack methods, companies are not only suffering financial damages but brand image damages too. Here are a few of the top things every eTailer should know about fraud in 2017. Card Not Present Fraud Is A Big Threat.

As you know, we’ve been looking at blockchain for quite a while, understanding the technology standards, doing pilots with banks and filing a number of patents. That nervousness is not entirely misplaced, Lambert noted, because cryptocurrencies and blockchain technology are innovative and extremely new.

The recent fascination with artificial intelligence and machine learning has made some of us ( naturally intelligent) humans confused about the role that these technologies play in the broader field of fraud analytics. Fraud analytics is an umbrella term covering a lot of technologies — let’s look at the two big categories.

The recent fascination with artificial intelligence and machine learning has made some of us ( naturally intelligent) humans confused about the role that these technologies play in the broader field of fraud analytics. In the fraud management space, BI can be thought of as a descriptive performance reporter. Source: FICO Blog.

Recently, IDC published a whitepaper, sponsored by IBM, outlining the ten hard realities that FIs and payments services providers must overcome to benefit from modernization, and how they can turn these perceived threats into opportunities. Change in technology and organization required. Payments modernization has arrived.

But the global adoption of such schemes, alongside the problems suffered by early adopters, has turned the focus to real-time payments fraud. As discussed in my earlier post , real-time payments make multiple types of fraud more attractive and enable the fast movement and laundering of criminal proceeds. Who Is Liable?

FICO has just released an interactive infographic on European card fraud trends since 2006, showing that card fraud in the 19 countries studied has hit a new high of €1.8 In the UK, card fraud also a hit a new high in 2016, £618 million, though the rise was less than the rise from 2014 to 2015. CNP Fraud Takes Over.

Artificial intelligence and machine learning are particularly interesting, with their ability to enhance data and analytics capabilities for customer services, compliance and client onboarding and payment processes and fraud detection services, among others.

Smart Card Technology Can Increase Security, Decrease Payment Vulnerability, Reduce Fraud and Improve Workflow for the Healthcare Industry PRINCETON JUNCTION, N.J. Press Release] – At the same time as the.

Before getting started, CSPs should determine who “own”’ and is accountable for subscription fraud. Is it the fraud team? Also, is there a clear and agreed fraud risk appetite that has exec sponsorship and is agreed by all stakeholders? In part, this is due to the ever-changing nature of fraud. Credit risk?

The Secure Technology Alliance has released a whitepaper, which shows that cards with dynamic security code features might prevent card-not-present (CNP) fraud.

As my colleague TJ Horan says in his post , the worlds of fraud and compliance are moving closer together. The objectives of the fraud department are different from those of the compliance team and traditionally they have come at the thorny issue of accurately identifying and understanding their customers from different angles.

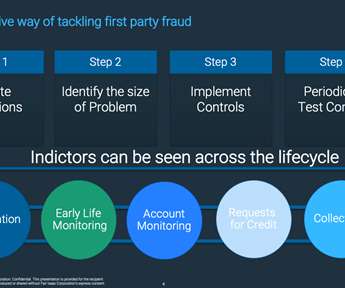

What Is First-Party Fraud? From banks to telcos to debt collection agencies, what looks like unrecoverable bad debt may in fact be first-party fraud. For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. by Matt Cox.

Fraud management and AML compliance are both about tackling financial crime, but often they are managed by different teams, each with their own processes and technology. When it comes to the technology to support financial crime specialists, we estimate that there is an overlap in their requirements of around 85%.

For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. Perhaps surprisingly, consumers sometimes use their own personal information to commit fraud. Both of these crimes are first-party fraud.

Globally, the European ATM Security Team reported a 19% increase in ATM-related fraud attacks from 2014 to 2015. Earlier this year, FICO reported a six-fold increase in US ATM fraud from 2014 to 2015. To learn more about this technology, see our whitepaper Putting a Wide-Angle Lens on Fraud.

Recently, IDC published a whitepaper, sponsored by IBM, outlining the ten hard realities that FIs and payments services providers must overcome to benefit from modernization, and how they can turn these perceived threats into opportunities. Change in technology and organization required. Payments modernization has arrived.

Digital banking channels are increasingly popular, and behavioral profiling of customers is vital in preventing new types of fraud. The open banking revolution makes understanding each customer’s behavior even more important in preventing fraud by considering all the aspects of transactions. Understanding Recurring Behavior.

The data revolution is one of the biggest technology changes facing banks at the moment, and efforts to effectively harness data should be at the forefront of any financial institution’s strategy. But let’s not underestimate the potential that technology brings forth. The benefits of being data-driven.

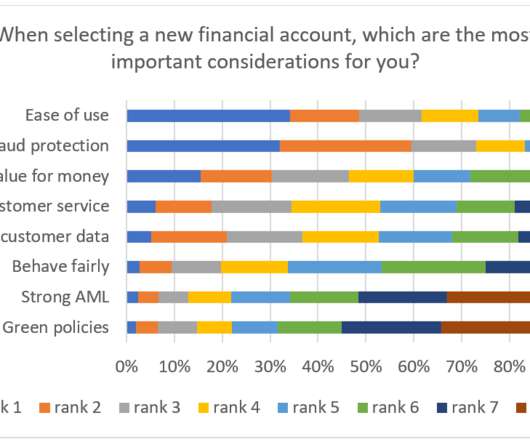

Top 5 Surprises from FICO’s Fraud and Digital Banking Survey. Our survey found that good fraud protection is paramount for customers - even though they themselves may exaggerate income or claims. A report released by the FTC in February 2022 indicates a 71% increase in fraud in 2021, which cost consumers roughly $5.8 FICO Admin.

If history is even a rough guide to the future, you can bet that some of the case studies, technology and techniques gained from what promises to be a major operational effort will make their way into the payments and commerce mainstream — which, of course, has its own daily issues with data breaches, hackers, fraud and authentication.

Launched in November 2017 , IBM Cloud Private (ICP) aims to provide users with the right mix of private and public cloud technologies. It leverages open source technologies like containers, Kubernetes, Helm and Cloud Foundry to deliver the benefits of public cloud but with the control of private.

In my previous post , I described how fraud analytics for open banking work. Following an introduction to behavioral analytics , this post focuses on how the data refined through behavioral profiles are combined in an unsupervised machine learning model to produce a score indicative of fraud or non-fraud. Learn More.

Meanwhile, technology changes continued at a breakneck pace, with generative AI the biggest topic around management tables. The specifics are unclear, but bankers recognized that this will be an absolute game-changing technology in future years, and delivery will change in ways we can’t even conjure yet.

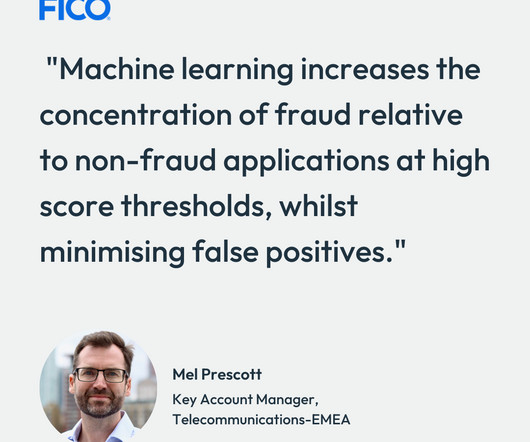

So it’s not surprising to find machine learning being advocated as the answer for payment service providers looking to manage fraud in the world of PSD2. Why does PSD2 make machine learning more important than ever in the fight against fraud? Actually, the use of machine learning to fight fraud has a long and successful pedigree.

Luckily, Decision Management (DM) technology has been invented and has come a long way since AC/DC released this epic anthem in 1975. The reduction of onboarding timelines from days to minutes is only the start of the benefits, those additional benefits including: Increased accuracy in detecting merchant fraud and default.

FICO machine learning capabilities have been around for more than 25 years, initially in fraud and credit risk, and extending to other operational and customer lifecycle use cases. Tools like Blaze Advisor and Decision Modeler are built for this approach; however, even the best technologies alone aren’t enough.

JP Morgan’s fine highlights the broader problem that many global banks had been facing, which was ignoring the warning signings of fraud and money laundering. This tool demonstrates AI’s transformative benefits in anti-money laundering (AML) and fraud detection. billion in 2014. This post originally appeared on the SIIA blog.

Now, it’s true that some companies — including some very big names across many important sectors of the economy — are taking measured steps and experimenting with blockchain tech — aka distributed ledger technology (DLT) — in the support of use cases that address tough problems. All you need for proof is to just follow the smart money.

With acceptance of biometrics becoming mainstream, and the need for fraud protection ever front of mind, how can banks use biometrics in order to be more effective and efficient? Fraud—do you need to change your approach to thwart a change or increase in attacks. Intelligent Orchestration of Multi-Factor Authentication.

In October 2021, using its authority under Section 1022 of the Consumer Financial Protection Act (CFPA) to send market monitoring orders, the CFPB requested information from six large technology platforms offering payment services. He identified “preparing for real-time payments” as the CFPB’s “primary focus” in the payments arena.

FICO leverages machine learning (ML) in solutions ranging from fraud detection to marketing. To learn more about FICO’s research in the use of artificial intelligence and machine learning for credit scoring models in the financial services industry, please refer to the following whitepaper: [link]. . by Can Arkali.

Cordray referenced an April 2020 whitepaper he co-authored that outlined immediate actions the CFPB could take to address the pandemic.) Chopra “his own person” and expects him to take the CFPB in new directions. He expects Mr. Chopra to vigorously pursue ways for the CFPB to support consumers financially injured by the pandemic.

The key success factor will be to be able to capture the application data in a digitally innovative way and to decision the applications almost instantly with low friction but with an adequate KYC, AML and application fraud control. For more information, see our whitepaper on “Can Alternative Data Expand Credit Access?”.

The technology available in most smartphones allows quality photographs of documents to be taken to validate identity. If the device profile has also changed, you know there is a potential SIM swap fraud and prevent access or invoke step-up authentication. If the associated device profile hasn’t changed, you can trust the SIM card.

Banks are not experts in IT, so now they can leverage plug-and-play technology functionality. Corezoid is advocating for a “process focused” view of bank technology, by use of APIs. Download our latest whitepaper that discusses what it really takes to develop a successful Fintech startup. Maria Gurina (Bus.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content