This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

At the same time, financial institutions face increasing pressure to streamline investment accounting, enhance compliance, and reduce operational riskall while ensuring leadership has timely and accurate financial data to drive decision-making. WATCH Investment accounting compliance risks U.S.

That’s an unfortunate but in some ways impressive record, considering that most BEC/EAC fraud relies on what the FBI referred to as “the oldest trick in the con artist’s handbook: deception.”. The size and scope of the problem has been steadily rising since FBI’s 2017 Internet Crime Report.

As the leadership at community banks and credit unions consider whether expanding CRE lending is for them, there are some basics of CRE that are worth remembering. Real estate is a notoriously cyclical market with fluctuations that can leave loans backed by real estate under-collateralized in the event of an economic downturn.

The second seemed to be something to do with that indispensable handbook on the future of the industry, “ Identity is the New Money “ But what did they mean? The first showed @dgwbirch looking at some sort of chart that seemed to be something to do with tokenisation. And who had put them under his door? ” “Well,” said S.,

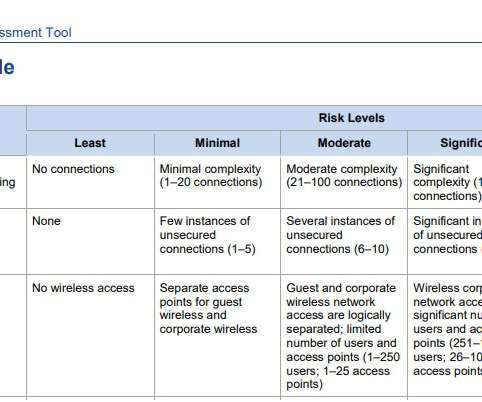

This was revised in 2017, and this consistent framework is intended to be able to help leadership and the board assess their preparedness and risk over time. It is part of a multipart blog series on financial regulations and how to manage them architecturally, geared towards IT leadership.

influence: The Psychology of Persuasion Fascism: A Warning Narconomics: How To Run a Drug Cartel Fear: Trump in the White House Never Split the Difference: Negotiating as if Your Life Depended on It The Servant: A Simple Story About the True Essence of Leadership How To Be A Stoic: Ancient Wisdom for Modern Living Crushing It!:

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content