This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

So far in this blog series, I’ve talked about how COVID-19 is amplifying banks’ need for innovation and the key technology trends that will shape the near future. The post How to build future-ready banking operations beyond the pandemic appeared first on Accenture Banking Blog.

Innovation groups are a relatively recent, but an increasingly important, addition to traditional bank structures. Whatever the approach is, Read More.

It’s also a great time to think about innovation. I would like to talk about how Twilio Flex and other services from Twilio can provide some clear ways not only to manage these immediate concerns, but also to drive innovations in how you interact with your customers. We can help guide you through all this.

EXCLUSIVE- Bank Innovation has released the agenda for its seventh annual fintech conference, and it is completely overhauled to enhance the event experience for attendees.

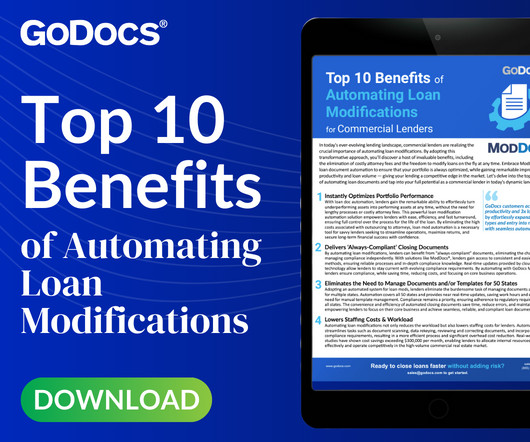

But with ModDocs®, you can enjoy an innovative solution that eliminates attorney fees, allows on-the-fly loan modifications, and ensures compliance. Learn how to generate compliant closing documents in minutes, streamline operations, and reduce risks.

The COVID-19 pandemic is accelerating the pace of digital innovation across the financial sector, and credit unions (CUs) are no exception. How Balancing Members’ Needs Improves End-To-End ATM Experiences. Developments From Around The CU Ecosystem. About The Tracker.

What makes the current developments so interesting and exciting is that “we're just seeing that they're at the end of the innovation growth cycle,” he explained. All of these new FinTechs and digital innovators are changing the landscape as the role of payments rapidly shifts in the broader financial services arena.

But the one thing that might work is taking a page from the innovation playbook that Netflix seems to have written and followed over the last 22 years. A combination of forces — Netflix’s own content and technology innovations and advances in hardware and software — helped them consistently attract more eyeballs.

The only question is how banks can ensure that they are employing the best strategies to apply them. I n How To Put AI In Your 2021 Business Plan Playbook , PYMNTS and Brighterion collaborate to provide a blueprint of how financial institutions (FIs) can incorporate AI into their consumer credit strategies.

With this regulatory risk and associated operational complexities, there is plenty for financial institutions to consider before diving into cannabis lending. Its a way to serve businesses that are often forced to operate outside traditional financial systems. Cannabis lending is more than just a potential revenue stream.

Intelligent Fulfillment Boosts Customer Service And Return On Inventory Investment or check out our recent webinar, How to Drive Better Customer Service With Intelligent Order Management. To learn more about the statistics behind these automated systems, download our commissioned study from Forrester Consulting, Get Supply Chain Right!

MAD services can cocreate with clients while supporting them in learning how to modernize capabilities with agile, DevOps, native cloud, and edge, including generative AI (genAI). According to the report, “tech execs and application development leaders implement MAD services to: Increase cocreation. … Improve customer experience.

The company also set up a multi-million-dollar subsidy program to reduce operating costs and capital risks for their merchants, in an effort to help them get back to work safely and efficiently. An Opportunity for Innovation . As the situation evolves, Wang told Webster, the innovative responses are doing the same.

Key topics covered in this post: Requirements for Regulation E compliance How to avoid fines and reputational harm What is Regulation E? This increased scrutiny can divert resources away from core operations and impact overall efficiency. Shared AML case management can improve coordination and information sharing.

It’s one thing to want to improve or innovate. What’s harder — and what really makes the difference — is figuring how, where and when to innovate, a task that must take into account various factors and even wildcards that keep popping up in the growing and global digital economy and its various ecosystems. B2B Payments.

Operations and engineering. Champions have preexisting knowledge of how to utilize Power Platform and aim to share their expertise and mentor makers. This, along with the role of operations and engineering, serves to help the makers by giving them the tools to make building applications easier and more consistent. Development.

How to close that gap has been an ongoing issue that’s led to friction between eateries and delivery platforms. But Robbins added that ghost kitchens were an early solution for closing the gap because of their lower operational costs. But Robbins said all of the technological innovations in the world can’t do the whole job. “I

Two hundred and seventy-four years later, those words are the perfect framework for understanding what will define the next decade of innovation in payments and any ecosystem that touches it. Sometimes those innovations disrupted old models and players; other times they made them better and more efficient. The Invisible Innovators .

But as of 2020, it is a subject upon which seasoned experts can disagree, in a world where traditional banks and FinTechs are operating in parallel in the market – and, in many cases, are offering similar services for consumers. But the FinTechs, Baird noted, are adapting and innovating around that issue.

In today’s rapidly advancing technology landscape, businesses face a profound revolution in operations, customer interactions, and innovative endeavors. Drive innovation with creative talent and practices.” Partnering with the right digital transformation service provider is vital to thrive in this digital age.

Most are encouraging employees to work from home while also moving their back-office operations online, and payments operations are no exception. For more on these and other news items from this space, download this month’s playbook. RLJ Financial On Managing B2B Spend With Virtual Cards.

“Once a business solves its digital transaction processing issues, they need to start considering how to efficiently and effectively go global. Noting that some countries are able to operate more normally now than the U.S., The world economy won’t wait for the U.S. to recover.”. The world economy won’t wait for the U.S. to recover.

Global pandemics may be rare, but crises of all sizes affect business operations in unforeseen ways. And, after employees are back, additional steps will be needed to optimize current operations and/or prepare for the next disruption. What is a Low-Code Application? Perficient’s Power Platform Hackathon. And wow us they did!

It’s an ongoing effort that has probably seen more failures than success stories, but that’s certainly not keeping people from betting on new innovations. That’s certainly part of the story in retail these days. Another part is the ongoing demise of physical locations, whether individual store locations or entire malls.

For inspiration in banking innovation, we often look to other industries. Instead of thinking traditionally, Gentle Monster pursued a strategy of innovation and creativity to become the hottest sunglass company globally, creating a company currently valued at $900 million. Honkook Kim and his Gentle Monster Brand is a perfect example.

How Power Platform Can Change How Your Business Operates. When businesses think of innovation, they often think of a new product that can generate new business or a new way to reach customers and facilitate relationship building. The ability to do those things is important, but it’s not all that innovation is about.

Director, Safety and Pharmacovigilance, and Prabha Ranganathan , Director, Clinical Data Warehousing and Analytics, hosted a webinar with Bio-IT World that discussed how to leverage AI and automation to improve case processing. The ROI directly relates to your current processes and the number of adverse event cases you have every year.

In a recent PYMNTS discussion with Karen Webster, Kohli dug deep into how financial institutions (FIs), FinTech firms and others need to find ways to work together to advance the cause of digital payments. Common Goal. The first part , released in March, focused on global payments and corporate responses to cross-border transactions.

Indeed, just as SMBs have fast-tracked their own digitization efforts, their financial technology partners have also found the current climate to be an opportunity to accelerate innovation and roll out new services to support their merchant and consumer users. Innovation On The Fast Track. The Bigger PayPal Picture.

Although CU members want innovation in member loyalty and rewards, most credit unions are not delivering these programs up to the desired standards. Credit union members’ high expectations when it comes to loyalty innovation do not necessarily make or break their banking relationships. Loyalty Innovation Strategies .

But, in an interview with Karen Webster, Zac Cohen, chief operating officer at Trulioo , cautioned against a “one-size-fits-all” approach to the digital identity space. Looking ahead, Cohen told Webster, “Innovations in digital identity represent the strategic difference that can help make or break companies over the next several years.

Scale, security, and innovation are all linked to better information technology design and implementation. SVA – larger banks consider shareholder value-added pricing, which takes into account operating profits produced over that bank’s cost of capital. Large banks that are not investing heavily in IT cannot compete effectively.

But as time passes and a new decade approaches – one that promises even higher levels of digital innovation and disruption – it’s becoming ever more clear that 5G mobile network technology will help power the so-called Industrial Revolution 4.0. Coal, steam and oil helped to fuel the industrial revolutions we read about in history books.

That included looking inwards to identify internal operating models and biases that may have inadvertently been impeding business goals and objectives. Innovative ideas come from groups with different perspectives. Identify initiatives that will drive operationalizing diversity and inclusion across the organization and customer base.

The Financial Crimes Enforcement Network (FinCEN) recently released proposed legislation that encourages innovation within AML/CFT programs, advocating for the integration of advanced technologies while maintaining compliance through human supervision.

These books span a range of banking topics but emphasize second-order thinking, productivity, building client relationships, and innovation. This fictional novel with an ugly cover is a fast-paced and entertaining story of a plant manager desperately trying to improve operational performance and his marriage.

How Customer Reviews Provide Lifeblood To Restaurant Operations. That focus has only grown amid the takeout- and delivery-only operational shifts due to COVID-19-related social-distancing efforts. Details gleaned online — including menus and reviews — carry a lot of weight when consumers are deciding where to dine.

Operational risk is rapidly becoming one of the most important threats to the financial system but is also one of the least well understood. But they are only one part of operational risk, which includes losses from any kind of business disruption or human error, including power outages or natural disasters.

Money tied up in the cash flow cycle is money that’s not working in the economy at large – it’s not helping businesses grow, expand operations or tap new customers. But digital technology and the ensuing innovations are likely to change those facts over time. As the late, great Tom Petty once sang, the waiting is the hardest part.

Banking and innovation doesn’t go together. Innovation creates risk and risk is unacceptable in a financial marketplace. So it’s interesting how we’ve spent the last five years talking about sandboxes, creativity and design in financial technologies. The idea is to innovate outside the markets. Something like that anyway.

In this episode, Brett King hosts thought leaders JoAnn Barefoot of Barefoot Innovation, Greg Cross of Soulmachines, and Tony Seba, Author of “Clean Disruption of Energy and Transportation” to talk about the AI-powered future and how to properly prepare for it. […].

It’s also opened up conversations about how professionals get paid. While there has been some innovation in wage payment mechanisms as more employers shift away from the paper check toward direct deposit and payroll cards, little has changed about the timing of those payments. ACH Innovation Breaks The Mold.

Artificial intelligence has a long way to go before it becomes a daily part of FI operations – but AI is coming one way or another. That much seems about as certain as anything can get.

The shift could drastically change how customers feel about having physical money stored in banks, according to the report. The BoE is among the global regulators looking at how to deal with digital currencies, which have become more of a clear prospect for the near future as the pandemic keeps people away from physical spaces.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content