This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

More than 140 bankers and industry experts from over 30 states gathered in Nashville, Tennessee last month for the 3rd annual RiskManagement Summit hosted by Sageworks. • How to Justify a Change in Your ALLL • Accounting for Purchased Loans • Documenting Qualitative Factors • Preparing Your ALLL for 2015.

Thousands of banks, credit unions, and accounting firms use our riskmanagement and lending solutions, contributing to this cooperative data model for banking intelligence. The real issue for many bank and credit union leaders is how to add incrementally to that portfolio in a profitable manner. Nearly all U.S.

Our intelligent fraud detection software and riskmanagement tools help fraud professionals in their fight against financial crime. Jay Blandford is Chief Executive Officer of Abrigo, a leading provider of riskmanagement, financial crime prevention, and lending software and services that help more than 2,500 U.S.

Key topics covered in this post: Regulatory focus Key questons for ALCOs Governance and concentration risks Expect the unexpected Regulators 'could not be more clear' Today’s regulatory climate is turning up the heat on financial institutions when it comes to liquidity and interest rate riskmanagement.

If an institution wasn’t fully prepared, however, it can nevertheless meet its goals using tailored asset/liability management (ALM) strategies. If the last time a study was performed was three years ago, the assumptions are not only outdated, but they also could be steering management in the wrong direction in strategic planning.

Learn more about how to recover market share with small business lending. Lending & Credit Risk. How to Win Small Business Loans This Year. Lending & Credit Risk. Portfolio Risk & CECL. Jump-Start Digital Transformation with Change Management. Credit RiskManagement. Learn More.

If anything is identified in the loan documents, engage with management and internal counsel to discuss how to document and strategize. Can you identify any smoking guns with respect to servicing, invoicing, documentation, or imperfections with collateral?

Does senior leadership do a good job of communicating its top priorities? Sageworks Senior RiskManagement Consultant Rob Ashbaugh said many financial institutions are focusing on portfolio growth in order to offset the profit-pinching effects of low interest rates and thin margins.

To conduct business, financial organizations must adhere to strict regulations about how to handle personal information and transactions. Creating a single, unified view of threats and how to defeat them across those lines can sometimes be very difficult. How the leadership is measured and compensated.

In the last article, we covered the basics of EOS ( HERE ), the Entrepreneurial Operating System, and how some banks use it to improve productivity. EOS is a comprehensive business system that empowers a leadership team to run a more successful bank. One of the framework’s strengths is the robust tool kit available to bankers.

Takeaway 2 Client fraud education at financial institutions should include takeaways that explain how to protect themselves from phishing and tips for staying secure online. Effective fraud riskmanagement includes detection and fraud monitoring that should consider customer or member history and behavior.

Meanwhile, bank and credit union customers are learning, by necessity, how to access their accounts, sign critical documents and close on loans without going to a branch. Identify and document how internal processes and procedures will be performed via manual and electronic means in the current environment and remotely.

Demand for effective cyber riskmanagement is so strong that the AICPA is developing common criteria for CPAs to use as they help clients evaluate their programs and efforts. A lot of us know how to protect the perimeter of our facilities, but it is people clicking and downloading that can pose the biggest threats.”

So far, bankers have taken comfort in the soundbite that “this crisis is different” because of the strong capital levels and riskmanagement rigor that has developed since the Great Recession. The winners of the next normal will come from the clear leadership that starts to rally right now. Ready … break! “In

The banking industry needs to evolve, and at the heart of that evolution is fresh leadership to shake up the mold. As the industry begins its revolution to rebuild and reassemble itself, it also needs to take a new look at leadership. A big part of this is moving from reactive to proactive talent management. Look back 25 years.

Enterprise RiskManagement – Bankers should expect that the regulatory pendulum will swing quickly to a highly strident tone. The slow, evolving maturity of a bank’s enterprise risk program needs to speed up fast. With the current situation, updates from leadership should be coming out at least weekly.

Additionally, individual and team accountability will be sky-high given the real-time dashboards that make this sales system visible to leadership. #2: The Enterprise@Service System This system may be connected to a bank’s CRM platform or built with service desk tools powered with robotic process automation.

Two of today’s hottest tech topics — cybersecurity insurance and artificial intelligence (AI) — were well represented at recent conferences in insurance and banking, respectively: Advisen Cyber Risks Insights Conference and Bank AI Expo. Advisen: Barbican Takes a Leadership Stance on Cybersecurity Insurance. Here’s my take.

How long is your to-do list? Like most other community bankers, you spent many long nights processing Paycheck Protection Program (PPP) loans, planning how to do business in a pandemic and much more throughout 2020 and 2021. will need to teach customers who are unfamiliar with technology on how to use—and trust—these digital channels.

You never know when you’ll get a text from your leadership about testifying in front of the Senate! Continuous and consistent details about the dangers of scams, how they’re perpetrated and how to prevent them will help consumers become a powerful line of defense against scammers. TJ holds a B.S. in computer science and a M.S.

Financial institutions standing in 2030 will have completed a significant and gut-wrenching transformation of their leadership talent. To overcome the struggle, banks need to build leadership teams that align with how a future “Smarter Bank” will operate. How did the team score? Where is there work to do?

However, in order to address this leadership mandate, CIOs must break through the tactical mindset and focus that consumes most hours of their day. Simply taking orders, fulfilling requests, managing outages, and measuring service levels—important responsibilities for sure—will not position the CIO nor the financial institution for success.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. Listen to the podcast episode, " How To Sleep Easier at Night About Capital and Risk Levels.". Lending & Credit Risk.

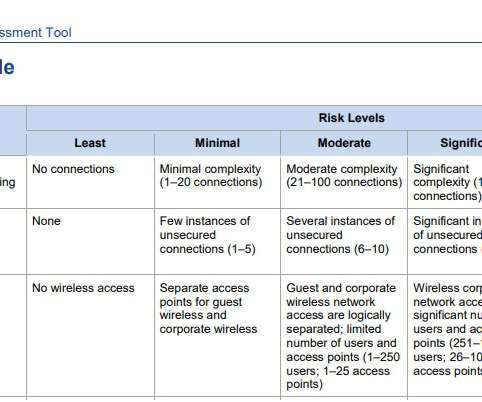

financial institutions, the FFIEC released new guidance and a Cybersecurity Assessment Tool for institutions to self assess their risks and determine their cybersecurity maturity. This was revised in 2017, and this consistent framework is intended to be able to help leadership and the board assess their preparedness and risk over time.

s Conservative Party leadership contest is only the latest geopolitical event sparking concerns among analysts over foreign exchange (FX) markets — and corporates’ ability to react to those changes. With Johnson named as new Prime Minister, analysts are again shifting their focus on the execution of Brexit and how FX markets will be impacted.

An early innovator in commercial workflow and analytics, upcoming CIOs could learn a ton from John on how to partner and engage constructively with lines of business. For more than 20 years, John has helped City National grow its niched commercial and private banking businesses with strategic technologies. ” – MX’s Kara Parkey.

Under Stuart’s leadership over the past 17 years, OnPoint has gone from under $2 billion in assets to knocking on the door of $10 billion, all while becoming the most recognized financial brand in the Portland market and achieving some of the industry’s best profitability in 2023. Also a big Gonzo thumbs up to Mantl’s Jeff Calnen.

Dave brings crowd-pleasing, almost scary enthusiasm and know-how to his technology and architecture sessions at demos without invoking a bunch of buzzword BS. Best Leadership Performance in a Core Conversion. An old adage that never gets old: it matters when leadership hangs out in the foxhole. Golden Cufflink Award.

Some 2,500 financial institutions have deployed the companys riskmanagement, financial crime prevention, and lending software. Jernigan Using our combined 30+ years of experience helping Abrigo clients implement, learn how to use, and make the most of software, we discussed what successful deployments have had in common.

Topics around identity, payments, card issuance/acquiring, leadership, and fraud were all more helpful than in years past. A common topic of sending banks was around how to better take advantage of The Clearing House’s new 5.0 . “Out” was the exuberance around banking-as-a-service (BaaS) and the giddiness of gen AI.

Since Richman and about 100 other bankers from LaSalle Bank in Chicago joined PrivateBancorp nearly a decade ago, the bank has grown to an $18 billion solid niche player with $10 billion in assets under management. Hats off to a decade of strong leadership and hard work. Gonzo Lifetime Leadership Award – John Glenn.

Since Richman and about 100 other bankers from LaSalle Bank in Chicago joined PrivateBancorp nearly a decade ago, the bank has grown to an $18 billion solid niche player with $10 billion in assets under management. Hats off to a decade of strong leadership and hard work. Gonzo Lifetime Leadership Award – John Glenn.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content