This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Before the COVID-19 pandemic, retailers were already seeing enthusiasm from customers for more convenient ways to interact during the purchasing process. While some retailers have offered limited order pickup options for some time, this was often limited to certain verticals or a small sub-set of products. The Challenges.

As the United States experiences a coin shortage due to the pandemic, some brick-and-mortar retailers are forcing consumers to tell cashiers to “keep the change.”. Not only will those customers give the grocers some personal information in doing so, but they’ll presumably revisit the retailer in the future to spend their unused change.

“We are essentially taking glass doors that were probably underutilized and not asking the retailer for any additional physical space.”. From a business standpoint, we believe that things like sales lift are obviously a really important metric,” Dravenstott said, “and you don't hear that much in brick and mortar retail.

Artificial intelligence (AI) and machine learning (ML) are starting to play a bigger role in retail, foreshadowing what’s to come in the new decade of the 2020s. According to PYMNTS research , AI and ML are blurring the divide between online and in-store shopping, and bringing an all-new human element into retail. Role of Data.

Across the retail sector, organizations are facing a new challenge in the form of the empowered consumer. Armed with a world of information at their fingertips, consumers are looking for information that is tailored to them about what to buy, where to buy it, and where the best deals are.

Food retailers need to embrace a new term: digital traceability. If a shipment of avocados says it is fresh until May 1, the retailer can check its proof of provenance, and doesn’t have to take the word of the supplier as that company promises fresh goods to its consumers. And it could be one of the killer apps for blockchain. “We

Retail keeps embracing numerous new technologies, and biometrics is not only one of them, but an area of recent growth and development, including via some of the biggest names in commerce. Take Amazon, which continues to expand its brick-and-mortar retail footprint, and the technology underlying those stores. Larger Trends.

The National Retail Federation ’s annual convention may have come and gone but the sentiments, strategies and lessons learned from facing nearly a year of pandemic-led changes by some of the world’s largest merchants are going nowhere fast — especially when it comes to their embrace of increased digitalization. Stores As Social Centers.

Now there are signals that a physical retail rebound is forming up. presidential election in the rearview mirror and 2021 right around the corner, a new shift is underway: the slow but certain move back to shopping inside retail stores — an experience that people still crave for the experiential joy it brings. With the U.S.

Physical brick-and-mortar retail was suffering long before the pandemic. Highlights include grocery, retail and contactless, he said. In addition, retailers are searching for more flexible fulfillment options spanning online pickup in store, pickup curbside, and a number of variants of that continuum of reaching end customers.

We developed an accuracy-based framework to have agents crawl various bank websites and rate the website on a scale from 0 to 100 with 100 signifying the fact that the website contained enough information to evaluate various transaction, savings and money market accounts and then the agent could successfully complete the opening of a single account.

said it plans to put many of its retail staffers on leave. Chief Executive Officer Mary Dillon said in the announcement, “As we navigate this very fluid situation, our teams are evaluating all new information, including recently passed legislation, to ensure we can make the best decisions for our associates, our guests and our business.”.

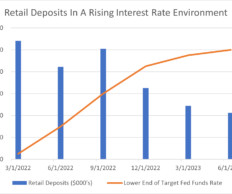

Now, we will delve into the stability of retail deposits from the same bank over the same timeframe, determining whether they were resilient compared to transaction accounts. As illustrated in the table below, retail deposit balances experienced a decline in every quarter, albeit not as sharply as transaction accounts.

In a roundup of today’s top retail stories: The automotive market continues its comeback with a digital spin, conversational commerce is the next big pandemic-fueled trend, and Tiffany said that its preliminary sales results for August and September 2020 are positive. Conversational Commerce Finds Its Voice in Digital Retail.

This is a customer account and contact information plus two years of information about transactions, costs, charges, and usage related to consumer deposit accounts, credit cards, and payment services. This data set includes account numbers, routing numbers, fees, rates, yields, and balance information.

Content that is relevant to channels and accurate, along with being supported by digital assets helps buyers greatly in making informed decisions. Feeling confident in making informed decisions then also leads to placing more orders online. The Right PIM and Commerce Platforms.

Amid the great digital shift , retailers and financial institutions (FIs) must walk the fine line between challenging transactions and letting the consumer journey proceed frictionless. That’s driven the retailer to require merchandise, risk-driven signatures that can be dynamically altered, said Thompson. The Scope Of The Problem.

The use of QR codes is growing more popular in the United States, enabling consumers to instantly access information and easily pay on their smartphones without going through a URL entry. Some countries are catalyzing this growth through national mandates rather than leaving retailers to their own devices. Retail Environment.

Move Retail Stores Online. Organizations are moving from relying on physical retail stores to omnichannel options such as buy-online, pick-up-in-store (BOPIS), ship-from-store, or curbside pick-up to fulfill consumer orders. Most consumers are staying at home, meaning fewer are heading into stores and more are shopping online.

In our last post , we talked about how curbside pickup or “click and collect” is expected to remain a popular channel for retailers to connect with their customers in a post-COVID-19 environment. Some examples of information that could be gathered from the customer include: the make and model of the customer’s car.

The latest CRA framework categorizes banks (CRA requirements are not extended to credit unions) into three tiers based on asset size, with differing compliance requirements: Small banks (assets under $600 million) Can opt-in to the new CRA tests or remain on a streamlined lending test that focuses on retail activities.

This same shift has been occurring within retail for over a decade and has taken precedence over building storefronts. A digital network is a platform that is dynamic enough to handle a variety of transactions; in healthcare, this would include virtual care, digital engagement, consumerism and retail offerings.

At some point after the COVID-19 crisis passes, retailers will need to reckon with artificial intelligence (AI). But if data is the new oil for retail competition, AI is the jet fuel. And if the retail comeback from COVID-19 contains order and purchase spikes, ignoring AI could come at a price. to increase sales.

A hacker is reportedly selling information from hundreds of C-suite executives' Microsoft -based email accounts, according to a report from Engadget. apparel maker and the CFO of a European retail chain," according to Engadget. The ZDNet tipster has also gone about notifying others whose account information is known to have leaked.

The reminder is intended for banks with clients that include marijuana retailers or individuals that grow, process, or manufacture pot. Among the rules: Banks must obtain identifying information, including a copy of licenses, as they would for any customer. Hemp Inc.,

ITMs and VTMs are popular retail banking innovations among community banks. What’s on the horizon for retail banking? According to a new report from PwC titled “Retail Banking 2025 and Beyond” (see sidebar), the retail banking industry is undergoing tremendous change—but, of course, community bankers already know that.

retailers CVS and Walmart are readying to begin distributing COVID-19 vaccines, according to published reports. In addition, the company said it is getting ready to inform people about when to receive the first and second doses of the vaccine. Meanwhile, Walmart said in a news release that it is also preparing to administer vaccines.

The bill mandates that tech firms get authorization from New Jersey consumers before collecting and selling information to third parties. The New Jersey bill mandates that any firms collecting personal data tell people in plain language how the information will be used.

Retail has been among the sectors most dramatically impacted by the pandemic, though it’s impossible to paint the industry with a broad brush. With widespread furloughs and a growing wave of bankruptcies , many retailers were hit hard. “Flexibility and agility are the common factors among the retail winners,” said Orr. .

Biometric authentication has always been a challenging subject with consumers, who are accustomed to using the technology to unlock their phones but are still wary about how much personal information they share with retailers and card issuers.

The ability for intelligence automation tools to be able to quickly and accurately grab the most relevant and accurate information regarding a customer’s inquiry, sales deal, or more is based on many data-readiness factors. Data completeness – Various data sources typically exist within an organization.

Stores that were affected could have had consumer data exposed, including email addresses, names, addresses and other pertinent information, according to the post. Shopify confirmed that complete card information and other sensitive personal financial information weren't part of the scheme. The breach took place Sept.

Tim Horton , head of global merchant security and fraud solutions at Fiserv , told a recent PYMNTS Masterclass that online purchases have more than doubled year on year in the general retail segment, while online grocery sales have surged by 250 percent. In fact, it’s becoming more valuable than card information itself.

consumers are now grocery shopping using a variety of connected devices, while 46 million (38 percent) are shopping for retail products — without ever leaving the confines of their homes. consumers are now doing their routine grocery shopping during the week as well as 153 million (51 percent) doing their retail shopping.

He praised financial inclusion, with microloans and mobile payments bridging a gap for rural residents but said protecting peoples' private information is still challenging. In August, PYMNTS reported that China's testing of the digital yuan was focused on retail, specifically on small transactions and excluding much larger ones.

And now, thanks to a global pandemic that has pushed more business online, tightened wallets and compressed delivery times, the retail landscape has undergone huge changes in a relatively short amount of time. “So Then came unbundling, followed not long after by the introduction of “rundles,” or recurring revenue bundles.

Retail, real estate, travel, hospitality and manufacturing — those are what we're seeing that are impacted and are in need of having a cash-flow infusion in order for them to stay afloat,” So said. Information Asymmetry. Another problem keeping SMEs from getting the financing they need is what So calls “information asymmetry.”

Fidelity National Information Services ( FIS ) and Global Payments were in talks to merge in a $70 billion deal, but it didn't end up happening, according to The Wall Street Journal (WSJ). eCommerce transactions increased 30 percent in the quarter, with a boost as FIS had begun processing those transactions at giant retailers like Walmart.

Amazon has launched a new program to gain information about users' purchasing activity beyond on its own website, a post from the eCommerce giant states, through monetary incentives. Named the Amazon Shopper Panel, it will pay users in exchange for the data and answering some short surveys.

Managing inventory, B2B payments and a plethora of food and beverage vendors can be a headache for any kind of restaurant, bar or retailer. Retailers that sell alcohol must be able to understand exactly which products they have in stock, and which products are generating the most revenue for the business.

Many retail or consumer goods businesses have had to switch from traditional, in-person shopping experiences to digital buying. Modern consumers hyper-adopt and hyper-abandon brands because many of the products they shop for are available at another retailer.

The agencies collectively announced a request for information (RFI) to gain input from stakeholders including financial institutions, trade associations, and consumer groups. These technologies are also used to better target marketing in retail and customize trade recommendations in wealth management. Credit Decisions.

Can Financial Institutions Bank CBD Retailers? Should an Institution Participate in Section 314(b) Information Sharing? This popular article highlights the pros and cons of registering with FinCEN Information Sharing and Section 314(b), and how to avoid potential pitfalls after registering. Did the Farm Bill Legalize CBD?

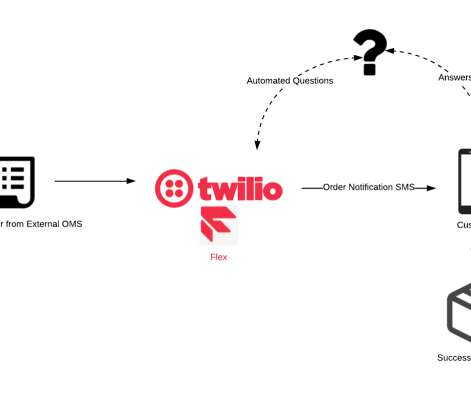

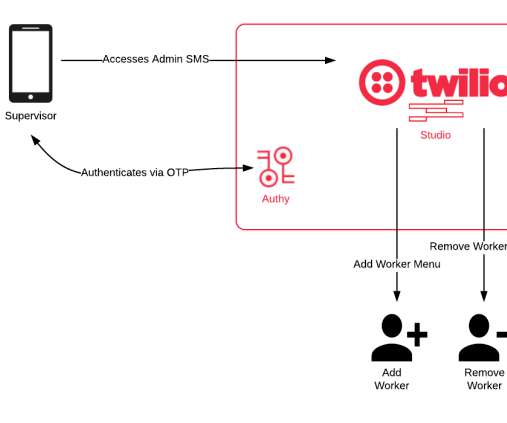

In our previous posts , we discussed the increasing popularity of curbside pickup and click and collect as a retail channel and demoed a pickup solution powered by Twilio Flex, Twilio’s cloud-based contact center platform. Protecting Personal Information Using Twilio Proxy.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content