This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Develop better ag lending workflows before demand picks up. A better ag lending process makes applying smoother for borrowers and can allow efficient ag loan growth without adding a lot of staff. Takeaway 1 Now is the time to plant the seeds for harvesting growth in the ag loan portfolio by creating a better ag lending process.

While short-term lending in general has a pretty rough reputation, the pawn loan is the most ill-regarded arena in an already unloved category of consumer lending. The loan amount a borrower can get from a pawnbroker is determined solely by the value of the item itself; as in most forms of short-term lending, there is no credit check.

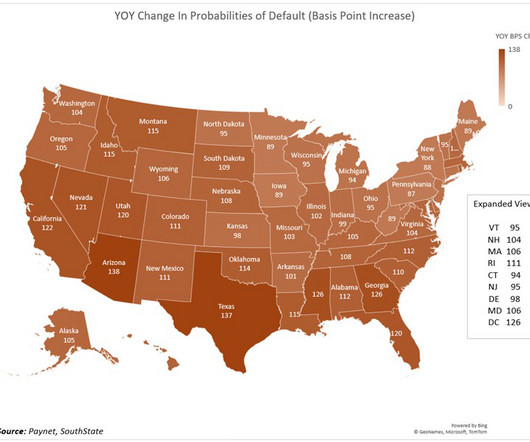

Lending is getting riskier. As can be seen, the consumer is starting to feel the credit shock first while commercial lending is still performing. The operative question is when commercial PODs will show a spike. Minnesota, North Dakota, and Iowa were the least risky states to lend into. This quarter, it is 2.58%.

Here, we highlight some of last year’s most successful loan producers in the areas of agriculture, commercial and consumer/mortgage lending. The score combines the average of the bank’s percentile rank for lending concentration and for loan growth over the past year in each lending category. By Ed Avis. Methodology. AGRICULTURE.

8), the AGs focused on Facebook include Colorado, Florida, Nebraska, North Carolina, Tennessee, Florida, Iowa and the District of Columbia. Operators of digital platforms, according to other recommendations, would also be required to adhere to codes of conduct, and to make pricing a bit more transparent. At this writing (Sunday, Sept.

and New York had the lowest increases in credit risk, while North Dakota, Iowa, and Minnesota had the lowest volatility and were the most stable. As such, office buildings are still undergoing a net operating income (NOI) reset, with the value of the properties dropping in a corresponding fashion.

This kind of small business is a dying breed: recent stats from the RUPRI Center for Rural Health Policy Analysis at the University of Iowa found more than 16 percent of independent pharmacies shuttered their doors between March 2003 and March 2018, according to Washington Post reports.

Iowa Superintendent of Banking Jeff Plagge offers ideas for long-term solutions to get struggling businesses back on their feet after the lockdown. Memorial Day signified the beginning of summer in many parts of the country, and the slow but steady reopening of business activity in the wake of the coronavirus pandemic.

million farms and the community banks that lend to them each growing season, Scanlan points out. I assume that will continue,” adds Larry Winum, president and CEO of Glenwood State Bank, a $170 million-asset agricultural lender in Glenwood, Iowa. A total of 300 million acres are covered by crop insurance. Rural housing loans.

Across the US, well-funded companies are rethinking how the financial system operates. California-based lending unicorn SoFi is the most well funded fintech company with just over $2B raised since 2011. We excluded companies that have not raised equity funding since 2015 and excluded funding from debt as well as lines of credit.

According to the CFPB, the new members “include experts in consumer protection, financial services, community development, fair lending, civil rights, consumer financial products or services, representatives of community banks and credit unions, and scholars with relevant methodological and subject matter experience.”

The bank was founded in 2006 and operates 19 full-service branch locations in multi-ethnic communities in Alabama, Florida, Georgia, New York, New Jersey, Texas and Virginia. and equipment lending and asset based lending through Triumph Commercial Finance. MetroCity Bankshares, Inc. Nasdaq: MCBS) MetroCity Bankshares, Inc.,

The bank operates thirteen branches, eleven in northern California and two in Nevada. It also operates four loan production offices, three in California and one in Oregon. They do have a traditional community bank with only 10 branches sprinkled in and around either Sioux Falls or Des Moines, Iowa. They are a $6.2

Several sectors in the economy run significant asset-liability mismatch that makes them vulnerable to rapid interest rate changes: pension funds and insurers have short-term cash flows and long-term liabilities, while banks follow a lend-long-borrow-short approach. or leave a comment below.

Lending Club provided investors with plenty to think about in its Q2 2015 earnings conference call this week. Here are a few of the highlights from a second quarter that saw Lending Club reach $11.2 Opened to investors in Texas, Arizona, Arkansas, Iowa, and Oklahoma. billion in total originations. Renaud Laplanche is CEO.

SoFI gets a commercial bank that brings deposits, compliance, AND business lending. Goes to MoneyLion for lots of obvious inappropriate behavior including violating the Military Lending Act regarding capped lending rates. Goes to Lincoln Savings Bank – Iowa (LSBX). The Appropriate CFPB Target Award. talent market.

and Operations center in a building they recently purchased as they look to double in size over the next five years: Cornerstone: Do you think you should build out your I.T. In its heyday the check digit was used to keep proof operator keying mistakes from causing downstream process issues in the form of rejected and non-posted items.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content