This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Now that the cannabis industry is maturing and better understood, is it time for financial institutions to take on the risk of cannabis lending? Cannabis-related businesses (CRBs)spanning everything from cultivation to retailrepresent a market in need of lending services, from working capital to real estate and equipment loans.

Automating the key steps that often occur in the back office leads to faster decisions, stronger customer or member relationships, and more profitable lending to small businesses. This article covers these key topics: Cultivating fertile ground for small business lending Do large lenders have an advantage in small business lending?

While it was once expected and acceptable for lenders to enforce standardized payment due dates and policies, COVID-19 brought the impracticality and ineffectiveness of a “one-size-fits-all” approach to credit and lending to light. IDC’s Take on Lending Digital Transformation Strategies. And for good.

Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. As rates stay high, concerns about credit risk and borrower health are top of mind for bank and credit union leaders, especially as it relates to lending to small businesses. Interest coverage ratios have stayed strong.

Boost your small business lending efforts from the bottom up Small businesses play a crucial role in our economy, and one of the critical factors in their success is access to funding. You might also like this guide for smarter, faster small business lending.

Federal Reserve said that it had launched a multi-trillion dollar lending program that targets smaller businesses, and in a broadened salvo, targets local governments, too. The Fed program is focused on lending. It’s all meant to shore up the U.S. economy, as the fallout from the coronavirus continues.

The recent uncertain shifts in trade policies, particularly increased tariffs on imports from China, Canada, and Mexico, have introduced specific uncertainties for community banks. Trade policies that lead to retaliatory tariffs from trading partners can lead to more severe economic repercussions in inflation, GDP growth, and employment.

Confident Risk Management Begins with Sound Loan Policy A risk-based approach to loan policy can effectively improve your institution's profitability. You might also like this webinar on loan policy best practices. Loan policies make up the foundation for managing that credit risk. . When and how to update your policy.

Develop an MBL program while mitigating risk Credit unions looking for alternate paths to growth in today's rising rate environment may be primed to leverage member business lending. Takeaway 3 The specific policy areas outlined below should be carefully considered by credit unions engaged in member business lending.

Recent data and trends of the small business lending market SMB Lending Insights is a snapshot of current financial trends and metrics that impact small and medium-sized business (SMB) lending and financial institutions. You might also like this guide for smarter, faster small business lending.

Abrigo's most popular whitepapers and checklists on lending and credit risk Abrigo experts' insights on CFPB 1071, loan policies, and risk ratings were popular with banking professionals. Watch NOW Takeaway 1 Abrigo's experts produced many pieces on lending and credit risk to provide strategies and tools to help banking professionals.

When and how to cite credit exceptions A policy on credit exceptions can address many factors that can lead financial institutions to diverge from loan policy and miss signs of potential trouble. Takeaway 3 A credit exception policy should spell out what one is, when it can be used, and how to clear it.

The European Central Bank (ECB) held this year’s first monetary policy meeting, and said in a statement on Thursday (Jan. The central bank’s governing council said that Eurozone interest rates will stay at record lows, as would other policies instituted during the pandemic.

Visualize your data, access benchmarks, and streamline reporting learn more talk with an expert Webinar Commercial Lending Credit Risk Management Lending & Credit Risk When good loans go bad: Managing problem and distressed loans Learn More Webinar Commercial LendingLending & Credit Risk Small Business Lending Answering your top CFPB 1071 (..)

Construction lending from the ground up. During a recent construction lending webinar , lending and credit risk expert Dev Strischek of Devon Risk Advisory Group outlined the keys to construction loan success. If your bank policy allows an LTV of up to 80%, then borrowers’ equity will be 20%. Introduction.

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. Takeaway 2 The top lending and credit blog posts focused on the benefits of banking technology, interest rate management, and developing risk ratings.

How construction administration units mitigate construction lending risk Construction lending involves unique risks and requires specialized processes. WATCH Takeaway 1 The OCC recommends that construction lending risk be managed by specialized real estate and construction lenders who report to the credit department.

And while the project doesnt directly apply to traditional lending portfolios, it nevertheless offers useful insight for community banks and credit unions. Implications for community financial institutions The proposed changes are narrowly targeted and not directly applicable to traditional lending portfolios. We can help.

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

Credit and Lending Software Overcome Common Lending Problems Banks and credit unions that leverage an integrated lending and credit platform reap the benefits of a consistent, efficient and defensible lending program. Lending and Credit Software. Would you like other articles like this in your inbox?

Over the past decade, several central banks have cut policy rates below zero. In a recent paper we explore the effect on bank lending by combining data on exposure to negative rates with banks’ balance sheets, the Spanish credit register and firms’ balance sheets. Why might negative rates work differently?

Loan Decisioning Allows Small Business Lending to Grow Community financial institutions can leverage automated loan underwriting to increase small business lending and achieve consistency. . Takeaway 2 Loan decisioning allows institutions to efficiently allocate credit analysts’ time for profitable small business lending.

Develop better ag lending workflows before demand picks up. A better ag lending process makes applying smoother for borrowers and can allow efficient ag loan growth without adding a lot of staff. Takeaway 1 Now is the time to plant the seeds for harvesting growth in the ag loan portfolio by creating a better ag lending process.

In recent remarks at the CRA & Fair Lending Colloquium, Grovetta Gardineer, Senior Deputy Comptroller for Bank Supervision Policy at the Office of the Comptroller of the Currency, discussed the OCC’s current fair lending initiatives. Her remarks were intended to.

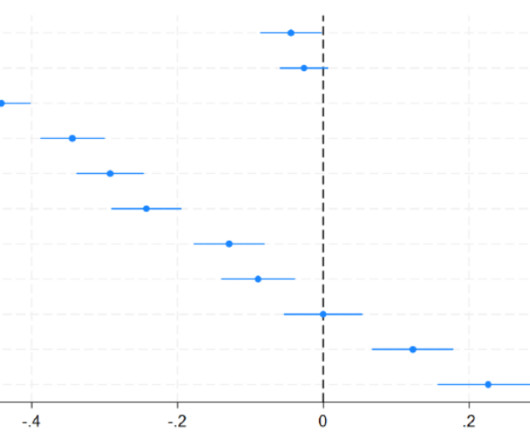

Interventions in corporate credit markets have featured prominently in the policy response to crisis episodes over the last two decades. Framework for policy evaluation We analyse the policy in four steps. We plot the estimated effects of the policy on average loan interest rates in Chart 1.

Personalized Touch with Efficient Service Can Boost Lending Banks and credit unions can boost business lending by combining a relationship focus with transaction-oriented processing. . This competition can only increase as the lending landscape continues to shift.

The Concepts Lending Curve: A yield curve shows interest rates associated with different contract lengths for a particular interest rate instrument. While economists may use the shape of the yield curve to gauge future economic strength, bankers should pay particular attention to the lending curve.

Julia Giese, Michael McLeay, David Aikman and Sujit Kapadia Central banks have been using a range of monetary policy and macroprudential tools to maintain monetary and financial stability. Financial crises and macroprudential policy The global financial crisis of 2007–08 highlighted major deficiencies in macrofinancial policy frameworks.

Mortgage lenders use this collateral valuation to determine how much they will lend on a property. The CFPB noted that courts have already held that an institution’s decision to use AI as an automated decision-making tools can itself be a policy that produces bias under the disparate impact theory of liability. Fraud screening.

Credit abuse: An employee manipulates credit lines for unauthorized use, perhaps leading to the bank lending more than the borrower can pay. Here are key strategies to mitigate internal fraud risks: Set the right tone at the top Leadership should communicate a strong culture of compliance and a zero-tolerance policy for fraud.

After reviewing numerous complaints, Google India said it will remove any apps relating to personal lending that are found to be in violation of its terms of service. The policy requires transparency by financial services apps that extend personal loans. . 14) blog post. “In

The CFPB recently issued its annual fair lending report covering its fair lending activity in 2021. . Small business lending—assessing whether there are disparities in application, underwriting, and pricing processes, redlining, and whether there are weaknesses in fair lending-related compliance.

The liquidity and funds management process should be very clear in terms of policies and procedures, she added. Make sure that your ALM policy, liquidity policy, and contingent policies have been updated. They’re required to be done annually, but if you’re even close [to that timeframe], I’d get it done now.”

How financial institutions deal with problem loans Problem loans are a natural outcome of the risks banks and credit unions take when lending, and they should be expected over the long run during the ups and downs of the business cycle.

For the past 14 years, the monetary policy in the U.S. This regime is now changing, and community banks need to position their lending and deposit portfolios for a period of monetary tightening. This regime is now changing, and community banks need to position their lending and deposit portfolios for a period of monetary tightening.

Stand-ou t bank business strateg ies for lending success These bank business strategies will help you market, target, add value to your lending services and build lasting relationships with your borrowers. Lending is a competitive and challenging industry, requiring constant innovation to attract and retain customers.

Though traditional financial institutions have faced a surge in market pressure to digitize as new FinTech competitors emerge, there are still plenty of areas in which banks hold the upper hand, commercial lending included. But an overwhelming surge in demand painfully exposed traditional banks' biggest shortcomings in business lending.

Michael Kumhof and Mauricio Salgado-Moreno While ‘unconventional’ balance-sheet policies like quantitative easing (QE) and quantitative tightening (QT) appear to have been successful, it is difficult to separate their macroeconomic and financial stability implications from those of other polices.

‘Zombie lending’ occurs when a lender supports an otherwise insolvent borrower through forbearance measures such as repayment holidays and temporary interest-only loans. In a recent paper , I examine whether these lending practices contributed to the subsequent low output experienced by the euro area. Belinda Tracey.

On the lending side, loan rates are expected to follow prime rates down, but the spread over prime may remain higher due to lingering credit risk concerns. Many examiners expectations include more sophisticated stress testing and more information on how lenders are complying with policy limits.

Sangyup Choi, Tim Willems and Seung Yong Yoo How does monetary policy really affect the real economy? What kinds of firms or industries are more sensitive to changes in the stance of monetary policy, and through which exact channels? ’), which is why we are interested in creating a broad database of such shocks.

Why Use Swaps, Caps, Floors, and Collars in Lending. A cap, floor, or collar is purchased as an insurance policy that is better not used. Just like a homeowner may be relieved but not happy to have to claim on a home fire policy, a cap or floor purchaser is always economically ahead if the cap or floor expires worthless.

To facilitate the creation of an entrepreneurial and innovative ecosystem, the Government of India, through its premier policy Think Tank called the Niti.Read More. INV Fintech, Bank Innovation’s accelerator arm, has seen an increase in applications from India, and currently has two Indian companies in its accelerator.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content