This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Now that banks have filed their third quarter financial reports , what did the lending picture look like last quarter? However, Q3 commercial lending is down from the beginning of 2014 (quarter ending 3/31/2014) by about $67 billion. Specifically for businesses, are commercial loans on the rise? Nationally, the picture is a fine one.

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny. banking regulations.

But the latest initiatives reveal a growing interest in transforming internal processes, particularly among smaller banks looking to upgrade their core infrastructure and elevate small business lending operations. Equiniti Eyes APIs for RiskManagement. Hawthorn River Eyes Open Banking for Community FIs.

These changes require significant adjustments in riskmanagement, compliance frameworks, and operational protocols. Emerging regions like Asia-Pacific, Africa, and Latin America are key growth areas, with partnerships enabling access to local payment methods.

The Hong Kong Monetary Authority has, as finews.asia reported this past week, amended its credit riskmanagement guidelines in a way that seeks to boost the embrace of analytics when lending to smaller firms.

the embattled bank, is reportedly overhauling its auto lending unit in an effort to control risk. According to a news report in Reuters , citing an internal memo, with the restructuring, Wells Fargo will phase out 57 regional offices in the U.S. and get rid of the regionalmanager positions in the impacted offices.

These FHLBs continued to lend to the member banks despite clear deterioration of their financial status. Capital rules are also being reassessed for members and the FHLB themselves in an effort to ensure greater financial stability and riskmanagement. Need assistance with ALCO reporting and analytical procedures?

This week’s look at the latest in bank-FinTech collaborations and open banking initiatives finds a focus on small business lending: In the U.K., This week’s look at the latest in bank-FinTech collaborations and open banking initiatives finds a focus on small business lending: In the U.K.,

Focus loan reviews on risk in the portfolio Continuous loan review monitoring helps banks and credit unions ensure credit review systems support safe and sound lending. You might also like this webinar, "Return to basics: Asking the right credit risk questions."

It was supposed to be a strong year for lending across the board, after a stumpy 2017, which saw numbers in both consumer and commercial lending tending toward a slump. regional bank executives were gearing up for a bumper year, according to Bloomberg. Bancorp , the largest regional bank in the U.S., Bancorp said.

Last week, I participated in a Finextra webinar on the topic of “Connected Credit and Compliance for Lending Growth” with panelists from ING, Vertus Partners, Misys and Credits Vision. Cost of compliance. Changing client expectations. Competition from new entrants.

“This heavily influences riskmanagement and regional exposure, which comes at the expense of clients abroad.”. lenders, but a senior supervisory official told FT that they can’t “force them to lend.”. BoA, Goldman Sachs and JPMorgan maintain they have upped global lending in recent weeks.

Analysts examined banks with at least 25 percent of deposits held in oil- and gas-dependent counties in order to investigate the impact of direct lending to local oil and gas firms and indirect lending to companies servicing the sector. Lower energy prices have had only a modest effect on banks’ profitability and capital adequacy.”

Grab’s financial services sector currently operates in Southeast Asia, with services like payments offered by GrabPay, rewards with GrabRewards, lending with GrabFinance, and insurance with GrabInsure. The company serves a long list of micro-entrepreneurs, small business owners, driver partners and users in the region.

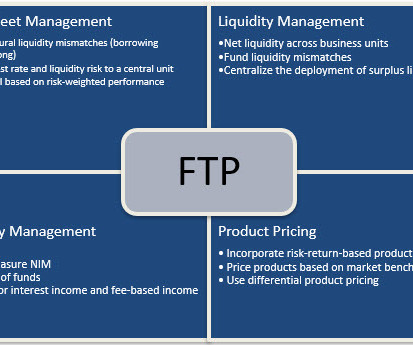

Bank executives that measure and manage the balance sheet based on the fair value of assets and liabilities invariable will change risk behavior, compensation structures, and capital allocation for the long-term benefit of shareholders. At its basic premise, FTP distributes banking profit between lending and deposits.

Bank executives that measure and manage the balance sheet based on the fair value of assets and liabilities invariable will change risk behavior, compensation structures, and capital allocation for the long-term benefit of shareholders. At its basic premise, FTP distributes banking profit between lending and deposits.

Bank executives that measure and manage the balance sheet based on the fair value of assets and liabilities invariable will change risk behavior, compensation structures, and capital allocation for the long-term benefit of shareholders. At its basic premise, FTP distributes banking profit between lending and deposits.

which have been looking into the ways that licenses and charters can be granted to FinTechs to help them offer lending and other services nationwide. Those regulators state that such services can be brought to thus-far underserved areas, and might boost lending to small businesses.

Some of the many specific solutions it provides is point-of-sale (POS) lending, wealth management, personal installment lending, small and medium-sized business (SMB) lending, insurance products and payments solutions. We don’t rely on a single data source or a single segment of demographic areas.

In 2020, we will likely see financial institutions putting more emphasis on automating time-consuming, manual processes that bog down lending decisions. By automating these mundane, laborious tasks, lenders and credit analysts are then able to focus their time on the borrower or member and make faster, more efficient lending decisions.

Both fintech firms and traditional enterprises are on the brink of significant disruption as companies leverage the rapid insights generated by AI in banking to drive demonstrable outcomes in customer experience, riskmanagement and cost efficiency. The caveat: There are winners and losers in this forward-thinking revolution.

With an eye on what could be called a true greenfield opportunity, alternative lending platform Biz2Credit is launching its small business lending products in India.

Eliminate Interest Rate Risk: Eliminate margin compression when interest rates rise. Meet Competitive Pressures : National and larger regional banks are specifically targeting better borrowers for five, seven, ten-year fixed-rate loans. Banks are in the business of keeping loans, not making loans.

Eliminate Interest Rate Risk: Eliminate margin compression when interest rates rise. Meet Competitive Pressures : National and larger regional banks are specifically targeting better borrowers for five, seven, ten-year fixed-rate loans. Banks are in the business of keeping loans, not making loans.

Nonetheless, with the recent collapse of sizeable regional banks, regulators, investors, analysts, accountants, and bankers are now scrutinizing the fair value of banks’ securities and loan portfolios. We believe that prudent riskmanagement is not predicated on trying to predict interest rates relative to the forward curve.

That growth was outpaced by a record number of applications, up 30 percent year on year, as LendingClub looks to spur “awareness” of the benefits of fixed-rate lending in an era where interest rates are on the rise. The company said it had loan originations of $2.9

Some banks with large commercial real estate concentrations are seeing their stock values take a roller-coaster ride as investors discount their assurances about the wobbly asset class.

Building out the ever-important treasury management suite, targeting deposit-rich customer segments, and creating new savings products are all examples of how banks can build deposit balances at low cost, low-rate sensitivity, and high deposit convexity. Lending Focus – Interest Rate Sensitivity and Credit Accuracy. Conclusion.

Then, there is the risk of corporate lending. Banks, it turns out, are willing to take on that risk. But for businesses — especially smaller ones — the risk of taking on new debt, or even the risk for being turned down for a loan, is too much to bear. . That value represents a 23.5

Ant Financial has 450 million customers and services spanning online payments, peer-to-peer lending and wealth management funds. Alipay is already accepted by more than 70,000 offline retailers in more than 70 countries and regions. Ant Financial wants to be accepted by U.S.

The DOJ investigation centered on whether LendingClub had – between January 2009 to September 2010 – misled its FDIC-insured loan originator, WebBank , leading the bank to underwrite over 200 loans that did not conform to the bank’s lending requirements. lending marketplace. Attorney Alex Tse. “We The Response.

Consider a regional bank with a “digital transformation initiative” that rolled out its new “digital user experience” for its retail customers in 2020. Battle complacency – At no time should you roll out a bank product such as digital account opening, lending platform, or even a website and think you are done.

The scenarios can include increases in interest rates, changes in cap rates by regions (this helps when evaluating collateral components), changes in rents, vacancies, or expenses, and CRE collateral stress. Portfolio Risk & CECL. Credit Risk. Portfolio Risk & CECL. Portfolio Risk & CECL. Learn More.

Users will benefit from advanced treasury and riskmanagement capabilities. The combined solution, available in the cloud or on-premise, is available to clients in France and the Benelux region, with the potential to expand into other geographies in the future.

The Cleveland-based regional bank is shedding credit risk in a partnership with the private equity giant Blackstone. It's the latest tie-up between asset managers and regional banks that are looking to free up balance-sheet capacity.

Ensley The experts, who are auditors and CPAs from regional and national audit firms and Abrigo, said communicating throughout implementation can be helpful in areas such as internal controls, model development or selection, and model changes. Ensley said most clients that have implemented CECL had received multiple validations.

The regional bank's stock price again fell by double digits on Tuesday, marking the fourth daily decline of at least 10% in the last week. The latest shoe to drop was the news that Chief Risk Officer Nicholas Munson left the company early this year.

They are very “horizontal” in that the revenue they produce and costs they incur cross cost centers, regions, products and customers/members. The thing about understanding and discussing channel and payments profitability is that these are not topics that tie to traditional cost centers or product lines.

The regional bank announced a leadership shakeup on Wednesday, capping a tumultuous week in which shareholders became spooked about its exposure to the commercial real estate sector.

In the past three blog posts, we have described what is driving open banking, the history of Open Banking, and the current status of Open Banking in different regions. C) RiskManagement. When we talk to people about the opportunities stemming from Open Banking, riskmanagement is usually a topic which comes up.

While one would assume the answer is ‘yes’, the world of FinTechs, P2P lending and online financial services have suffered quite a few stops and starts in China. Jennings spoke about the dual problems of reckless lending and the challenge of improving financial inclusion in China.

Rather than just one predictive model, Grupo Monge and FICO saw the opportunity to produce country-specific models that captured regionalrisk patterns. These models are activated within FICO® Blaze Advisor®, an advanced tool for decision strategy management.

He has held various roles in product development, riskmanagement, software development and consulting for banks, hedge funds and software firms, including Standard Chartered Bank, TCG Group, HCL and Cognizant. Sid’s analyst research is focused on the intersection between riskmanagement and high-performance analytics.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content