This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Credit, interest rate, liquidity, optionality, legal and operational risk all interplay with each other to expose the bank, and the borrower, to a set of risk that can be visualized as a three-dimensional area. Given the current state of the economy, this risk is near an all-time high. Another way to look at this is the pricing output below.

What is ServiceNow Financial Services Operations (FSO): Financial Services Operations (FSO) is an out-of-box offering by ServiceNow utilizing its existing platform custom-tailored to the use cases for Financial Institutions providing a comprehensive solution for managingoperations end-to-end.

Likely trends are shaped by a dynamic rate environment The top issues facing executives managing credit portfolio risk and the balance sheet at financial institutions are shaped largely by the dynamic rate environment, according to Abrigos outlook for major trends in the year ahead. Navigate rate environment uncertainty with confidence.

A couple of weeks ago, we delved into the origination and operating costs of manufacturing commercial loans ( HERE ). Cost of Deposit Sales and Marketing. To derive the foundation of deposit profitability, you start with your sales and marketing costs. The final takeaway is that bankers usually spend too much on marketing CDs.

Learn the seven must-have features that you can press vendors to showcase, and discover the secrets to accelerate your time to market while maintaining compliance controls and risk management standards.

The expanded executive leadership team will drive continued growth and operational excellence across Perficient while delivering superior solutions for clients. “As ” Prakash Chembai, AVP of India global delivery operations. She will provide resources to scale client projects and speed time to market. Ostasz, AVP of U.S.

There have been few times in modern memory when small businesses and middle market companies faced so much uncertainty in the market. These conditions not only impact business operations but also raise critical questions about liquidity, creditworthiness, supply chain stability, and growth strategies.

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence.

Their flexibility, low premia and underlying leverage appeal to all market participants ranging from conservative investors hedging against intraday market volatility to aggressive traders speculating for quick profit generation. The improved market conditions have encouraged both market participation and innovation.

The front office is screaming down to the Settlement Office, “Operations, we need more capital!” Any operations team that has dealt with a stock loan trading desk can contest the inherent friction between providing more available securities to the desk and reliance on settlement cycles and market constraints.

The product generates significant fees and helps drive deposit balances, yet debit cards rarely get a mention in strategy, marketing, or customer profitability circles. To support debit card operations, a bank gets charged a myriad of transaction charges and maintenance fees from the card rails (Visa, Mastercard, Discover, etc.),

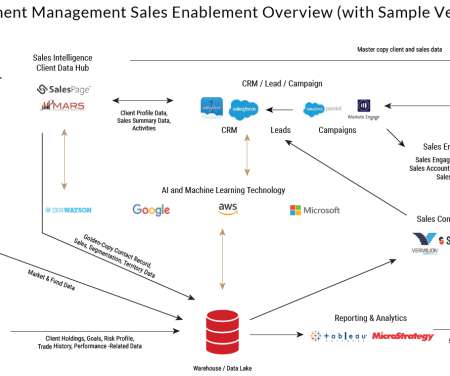

Sales enablement is a strategic approach to align sales, marketing, and operations around the common goal of equipping salespeople with the right resources, tools, and processes to sell effectively and support clients. marketing) and those charged to leverage these resources in deals (i.e.,

Expand access to all clinical specialties virtually, deploying a clinical operating model that seamlessly provides both virtual and physical care as needed/demanded. The New Challenge: Creating A Pluralistic Clinical Operating Model. The Essential Dimensions of the Pluralistic Clinical Operating Model.

The move shook the markets, threatening to upend much of the architecture of the global economy and fueled broader trade wars. Rising production costs led some companies to downsize or relocate operations outside the U.S. Volatility will surely spike and markets will be unsettled. China could devalue its currency again.

Digital transformation will remain a powerful force, with advancements in AI and machine learning enabling unparalleled operational efficiencies and hyper-personalized customer experiences. By integrating financial services into non-financial platforms, banks can tap into new markets and customer bases, generating additional revenue.

Wealth management is evolving rapidly, driven by generational shifts, changing advisor roles, new business models, regulatory demands, and a growing preference for low-cost passive products. This powerful capability equips wealth management partners to support clients more efficiently and build a competitive advantage.

Amid market volatility, organizations are finding it imperative to accelerate their accounts receivables while extending accounts payables and still maintaining positive buyer-supplier relationships. The biggest barrier to cash flow management is putting together the data in a consumable way for executive teams," he said.

However, in this blog, we will discuss the regulatory landscape surrounding cryptocurrency from an asset manager or fund manager perspective. New York’s BitLicense requirement therefore applies to investment managers who issue digital coins or otherwise act as an exchange platform regardless of where the buyers are located.

Manufacturers face a common challenge when trying to respond to unplanned market events that may impact business financial forecasts as well as sales and operations planning processes: having a single view of the business plan, with the right indicators can improve timeliness of key decisions.

Two-plus years later, banks and credit unions continue to feel the pressure to transform their credit and lending operations. The IDC Market Glance offers an overview of the landscape for consumer and small business digital lending. And for good. A Pathway to Improved Loss Rates and Happier Customers.

Lesson 1: Generate Operating Leverage to Produce Capital If there is a single lesson in banking that decides success in all areas of performance, it is this sell more profitable products to more profitable customers to the point where your bank generates a consistent risk-adjusted return above its cost of capital.

These reliable customers provide a stable, low-cost funding source that is critical for financial institutions operations. Higher interest rates reflect a higher cost of borrowing from the market relative to the cost of maintaining cheaper deposits, which can make the value of deposit relationships soar.

At present, we track 150+ AI agent platforms that households and business can use right now to manage banking products. With the rise of autonomous agents acting on behalf of userswhether individuals using AI assistants or businesses employing agents to manage financesbanks need to rethink their digital architecture. The solution?

As noted at the time by the OCC, advances in computing capacity, increased data availability, and improvements in analytical techniques have significantly expanded opportunities for banks to leverage AI for risk management and operational purposes. The evolution of electronic trading provides a valuable case study to consider.

We are witnessing the integration of AI, the rise of hyper-personalization, and the adoption of advanced digital platforms, all of which are revolutionizing operations and client interactions. Our experts have identified the most impactful trends across banking , wealth and asset management , and payments.

Understanding the drivers of banking consolidation is imperative when managing bank performance. Germain Depository Institutions Act of 1982 enabled thrifts to offer money market accounts and expand lending powers, fostering competition with banks. These two acts took the governors off around how banks managed deposits.

In an interview with PYMNTS, Avi Cohen , co-founder and CEO of FinTech company The Floor , said boosting digital offerings and bringing new ones to market demands quick decision making as banks seek to improve user experience and user engagement. Launching Into New Markets. That’s the end game for many of the banks: the time to market.

This connectivity enhances interoperability, allowing for streamlined operations and improved data flow across various platforms. Azure Integration Services provide the scalability required to handle varying workloads, ensuring businesses adapt quickly to changing market conditions without compromising performance.

Likely, you do not have a common management framework at your bank. However, it is doubtful you utilize a complete operating system. This article discusses using EOS in banking – the Entrepreneurial Operating Model. You need to manage multiple product lines across different customer bases and geography.

If passed as-is, the Japanese government would designate the AI systems and developers that are subject to regulation; impose obligations on them with respect to the vetting, operation, and output of the systems; and require periodic reports concerning AI systems.

In a previous article [ here ] we discussed why community banks need product managers to ensure that financial products and services are effectively developed, launched, and managed to meet customers’ evolving needs and the bank’s risk and profitability goals. This makes the product easier and faster to implement.

Cannabis-related businesses (CRBs)spanning everything from cultivation to retailrepresent a market in need of lending services, from working capital to real estate and equipment loans. With this regulatory risk and associated operational complexities, there is plenty for financial institutions to consider before diving into cannabis lending.

If one product is the future of banking, it is treasury management. In this article, we detail the five steps to building a treasury management strategy, provide some tools to execute those steps, and then provide a complimentary survey to assess your strengths and weaknesses. It starts by targeting the right customers.

By focusing on these key areas, companies can effectively manage the challenges and opportunities presented by the widespread adoption of real-time payments. These changes require significant adjustments in risk management, compliance frameworks, and operational protocols. As embedded payments become mainstream, U.S.

It segments each vendor by market presence and capabilities. The report names Perficient as a small (<$200 million in Oracle apps services revenue) consultancy with vertical market focus in energy, healthcare, and manufacturing. Manage business disruption. Foster innovation.

The treasury or cash management customer is usually a bank’s most profitable customer on a risk-adjusted basis ( HERE ). In this article, we discuss cash management profitability and rank the most profitable industries for banks to go after. As such, operating accounts have low-interest rate sensitivity.

Achieving these commitments will require clinical, marketing, and operations teams partnering more closely together and in a way they never have before. Revenue recovery efforts offered a necessary but insufficient first step – we urge you not to be complacent if you’re fortunate to have managed through a first wave.

Approvals is a newer capability in Teams that allows you to quickly create, manage, and share an approval workflow directly in Teams! Operator Connect. Looking to connect your current operator to Teams without the need to worry about managing new hardware? Operator Connect Conferencing. Image provided by Microsoft.

trillion (USD) in 2023 with outsourcing contributing to 60% of market growth. In the same way, Perficient leverages our more than 1,000 full-time employees in our fully owned and operated global and domestic delivery centers to deliver quality with every client engagement.

Something might be getting lost in the tribal knowledge of managing time deposits. In this article, we highlight how to better manage time deposits to prevent banks from destroying value. The CD market was born and managing time deposits was a new banking skill.

With loans, it’s hard to discern expert-level skills unless you know the market and the credit. Non-Expert Deposit Pricing Management – How To Destroy Bank Franchise Value The best way to quickly destroy value is to peg a deposit product to an index such as SOFR, Prime, Fed Funds, or Treasuries. Deposits, however, are pure.

Previously , I discussed the role of sales enablement in investment management. You need an effective cross-functional team with representation from sales, marketing, analytics, financial operations, and technology, all working in stride with the company’s technology teams.

Why change management is vital for banks and credit unions Regulators promote change management to manage risk, but banks and credit unions can also achieve important benefits when they manage change. This article describes recent comments by financial regulators about managing change.

With the current flat or slightly inverted yield curve, plus the current volatility of the market, borrowers have a pricing advantage to lock in long-term, fixed-rate loans, leaving lenders with the interest rate risk without appropriate compensation. Without this minimum staff, we believe that is difficult to create a viable B2B program.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content