This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

in adjustment (9.2%) for interest rate risk movement. at the end of 2022, and the bank’s filing shows that the mark-to-market loss on the HTM portfolio was over $15B, almost equal to the bank’s equity base, thereby, making the bank economically insolvent. The bank’s available-for-sale (AFS) portfolio was $26.1B

Both established markets and emerging vendors on the Dark Web have been actively promoting fresh inventory and steep discounts for holiday sales, including Black Friday and Cyber Monday. Another popular category in the underground is account markets. Lending & Credit Risk. Portfolio Risk & CECL. Learn More.

Political climate, environmental issues, technology innovations, criminal activity, economic volatility/inflation, account diversity, and industry regulatory changes are just a few examples of factors that often spur reputational risk or crises. However, these reputational riskmanagement (RRM) frameworks are still widely underdeveloped.

Representatives from all three lines of defense—operational management, riskmanagement/compliance, and internal audit—attend to present, discuss, and learn about industry shifts that are impacting risk and regulatory compliance. Sessions include a keynote interview with former FBI director James B.

It’s gratifying to see IBM once again positioned in the Leaders Quadrant of the 2019 Gartner Magic Quadrant for IT RiskManagement, released on July 3 rd for its OpenPages with Watson solution.* Digitalization brings along risks like IT security, Cybersecurity, etc. Learn more at ibm.com/RegTech.

Big Data analytics reached a market valuation of $29.87 Banks can even harness external regulatory, trading and socialmedia engagement data, all of which can be processed and analyzed to benefit their operations. One of the most powerful tools in the financial sector is data analytics. Data Analytics Behind the Scenes.

The ABA has a new report out on how banks are using socialmedia, and much of the report focuses on using Twitter, Facebook, LinkedIn and the like to boost customer service, make connections in the community and recruit staff. It often Tweets columns tied to breaking news and statistics. Learn more here.

Socialmedia giant Facebook is looking to grow its blockchain team, according to a report. The company posted on its careers page that it’s looking for data engineers and scientists, software engineers and a product marketing lead for its blockchain team.

Some blame the dilution of the Dodd-Frank provisions, others the lack of oversight by regulators, and others still blame socialmedia for exacerbating the deposit run. The root cause of Silicon Valley Bank’s (SVB) failure is poor riskmanagement – plain and simple.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. or those primarily focused on the domestic banking market. You're not alone. banks and credit unions can be difficult.

While we wrote about the root cause of the failure of Silicon Valley Bank (SVB) HERE , the lessons of the current banking crisis go beyond interest rate riskmanagement. While interest rate risk caused the most significant impact on value, several other factors contributed to the terminality of each bank that was closed.

Austin Burkett, global head of Quant and Feeds at Thomson Reuters, said, “News and socialmedia are driving the investment and riskmanagement process more than ever with the continuing rise of passive and quant-driven trading.”. The recent declines also came as the U.S.

Money Market Funds – With consumers waking up to the differential between bank rates and rates in treasuries, a stunning $469 billion flowed into money market mutual funds in Q1 2023. When COVID-related financial support stopped, consumers sopped up some of their savings in spending.

Two watch sellers are diving into a pilot that will test whether socialmedia and blockchain can power alternatives to Amazon and eBay for e-commerce sales, shopping, payments, riskmanagement and marketing.

Recent bank failures hurting public perceptions, the current market trends of higher rates, Quantitative Tightening, digital banking, socialmedia, and a flight to safety have increased the difference between model and observed liability durations. Unrealized bond losses are also included in the model.

Global growth inevitably means working in unfamiliar territory, whether it be new geographic markets, business partners or otherwise. and China, and between South Korea and Japan, have forced corporates to shift their supplier bases into new markets. The ongoing trade disputes between the U.S. ”

Optimizing risk, compliance and security. In 2019, the financial services industry will continue to be disrupted by new customer experience expectations, market entrants, emerging ecosystems, digital transformation and shifts in a variety of economic and technological trends. Check back often since IBM is adding new sessions each day.

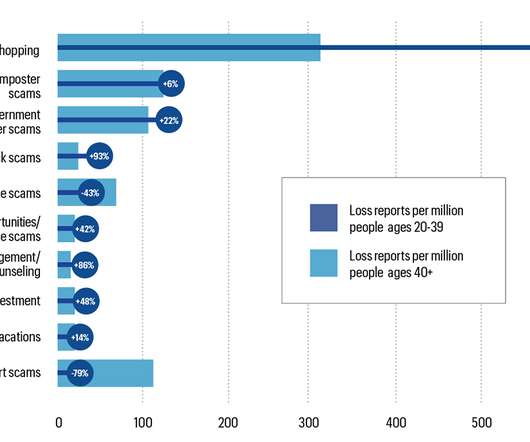

Each generation interacts, understands and uses technology differently, and fraudsters are triggering customers based on this understanding, says Glenn Fratangelo, director of product marketing and strategy at NICE Actimize based in Hoboken, N.J. Socialmedia. A cohesive strategy. Baby boomers. Robo calls. Romance scams.

To build stronger customer relationships, he adds, more banks should distribute more data lower down to their loan sales staff, particularly data on loan growth, loan profitability and risks, and past-due loans and critical loan exceptions. Bob Legters, senior vice president at FIS Global in Jacksonville, Fla., Karan Bhalla, Consultant.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. or largely focused on the domestic banking market. We have webinars , whitepapers , and other resources to make your job easier.

While a product like a certificate of deposit might only have a part-time product manager, a product like treasury management will likely have many. In addition to assembling the team, the product manager needs to take responsibility for the continued training around the problems, the environment, and related solutions.

Alternative data can create an accurate ‘digital fingerprint’ of a consumer, blending trusted online and socialmedia intelligence with conventional offline data for hyper-informed decisions—handled in a way that doesn’t sacrifice the consumer experience for security. CEO of Market Platform Dynamics.

To build stronger customer relationships, he adds, more banks should distribute more data lower down to their loan sales staff, particularly data on loan growth, loan profitability and risks, and past-due loans and critical loan exceptions. Bob Legters, senior vice president at FIS Global in Jacksonville, Fla., Karan Bhalla, Consultant.

How do we elevate our credit and operational risk visibility to ensure capital preservation and demonstrate strength to stakeholders? Are there growth opportunities that would make sense for us to consider at this time – such as entering new markets/M&A? RiskManagement.

Which works better for modeling credit risk: traditional scorecards or artificial intelligence and machine learning? To build the models in Origination Manager Essentials, our data scientists used AI and machine learning algorithms to discover a better way to segment the scorecards. It’s also a bit silly.

Here are seven key areas where bank executives need action plans to address burning challenges: Communication – Bankers have been working to calm their customers and community, but the quantity and quality haven’t yet met the standard in an always-on socialmedia world where the public is sniffing for transparency and authenticity.

Even in the quiet seasons, the online travel market is susceptible to the trade winds, and they don’t always blow in agents’ favor. If agents can’t take payments in a region’s most popular form, they risk losing that market altogether. Globalization also means that agents must navigate uncharted legal and regulatory landscapes.

The team also consists of Rachel Morrissey, executive producer of Fintech5, and Mike King, a fintech socialmedia leader and author of Bankwide. Topics include fintech, riskmanagement, blockchain, fraud detection and more. Bank on IT. BAI Banking Strategies. BankSocial.

This is a classic bank deal – one acronym buys another at a good price and plans to cut the hell out of cost while adding markets. Chris’ public posts including his playbook for dealing with COVID-19 were gobbled up on socialmedia. Market cap in January: $19B. Bank Deal of the Year PNC nabs BBVA USA – paying 1.3

Trust acquired 100,000 customers in just ten days after it launched in September 2022 and exceeded 450,000, equivalent to 9 percent of the Singapore market, within just five months. You can read more about this digital customer onboarding story in the full media release. FICO Platform helps us to deliver that edge.”

Moreover, conduct risk is a moving target: it takes many different forms, and every year the threats become more complex and sophisticated. Risk and compliance investigators have now identified over 100 different market manipulation techniques that employees can use to gain an unfair advantage over their employers or customers.

1: The Marketing and Sales System This system will intelligently collect the top-of-funnel marketing automation and socialmedia activity with a data-driven enterprise lead and sales management capabilities. A GRC system is more than a pure audit system.

Merger of Equals Deal of the Year (Credit Union) – Spire Credit Union and Hiway Credit Union put 2+2 together to make a $4 billion institution in the Minnesota market. While Huntington is down like most bank stocks, the pain hasn’t been as severe, and Huntington doubled down on local markets in 2023 by consolidating business units.

In an industry where the top five institutions control more than half the market share, it amazes me how few of the 6,000 other banks are taking advantage of shared insights and resources to compete. We see the types of content being shared through socialmedia. As consultants , we haunt the halls of industry conferences.

each of these companies made false representations—including on their websites and socialmedia accounts—stating or suggesting that certain crypto–related products are FDIC–insured or that stocks held in brokerage accounts are FDIC–insured.” According to the FDIC’s press release , “[b]ased upon evidence collected.,

My colleague Ryan Rackley summed it up perfectly when he referred to socialmedia as the “new tattoo.”. The company’s marketing message is that their merchant POS devices can be as smart as consumer devices. market will be very far away. Facebook posts, text messages, tweets, etc., Keep your eyes on this innovator.

He is chief of judges for the annual Retail Banker International Awards and lead market advisor for GlobalData's retail banking research division. He maintains an editorial advisory board of leading bank executives and is a regular guest banking analyst with BBC, NBC and other leading media. Burcu Çalıcıoğlu, Akbank (previous winner).

Prosper’s commitment to providing wider access to credit has been impressive,” said Neeti Aggarwal, CFA, senior research manager at The Asian Banker and one of the FICO Decisions Awards judges. Read this blog to understand some of many FICO approches available to help with financial inclusion.

Which works better for modeling credit risk: traditional scorecards or artificial intelligence and machine learning? This allows us to apply AI to improve risk prediction without creating “black box” models that don’t give riskmanagers, customers and regulators the required insights into why individuals score the way they do.

Passengers were left stranded with nothing to do but sit on their phones, pout and voice their frustrations on socialmedia. However, Southwest stepped up and used social networks to communicate with their customers, address concerns and face the crisis head on. Not just for a little bit, but for hours and hours.

No one has been more successful at using socialmedia to generate awareness and a positive image for their bank than Jill (@JillCastilla, @CitizensEdmond). Jill’s use of Twitter is a model for any bank CEO looking to engage on socialmedia. Community bank marketing resources. Freudian Slip Award. C’mon Man!’

recently did a study where we looked into how many banks & credit unions were on socialmedia. Marketing doesn’t have time, compliance doesn’t have time, who has time to manage this? Which of those marketing functions are we going to take time from? What if socialmedia is a fad?

Opening up that market is a priority for lenders. And while many of these people are in developing markets with nascent credit infrastructures, there are so-called “credit invisibles” in the most mature credit markets, people who have no credit and are unknown to the credit bureaus. Social Profile Data. How Much Value?

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content