This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Payment system types, trends, and fraud risks Understanding how payment systems function, the different types in use, and the associated risks is critical for financial institutions to be able to balance innovation with security. Key topics covered in this post: What is a payment system?

According to Ossama Soliman , chief product officer at open banking provider TrueLayer , the very fact that there are so many payment options pushes new entrants to differentiate themselves from the pack. “It But actually, it raises the bar for what it takes to add a new payment method into the checkout.”. 26) in the U.K.,

Consumers keep demanding a better, more convenient, seamless, secure user experience that makes their lives better. And this is happening across many verticals,” Mastercard ’s Senior Vice President of Digital Payments Silvana Hernandez told PYMNTS in a recent conversation. Hernandez said. “We

Corporate buyers are quickly shifting their purchasing habits online, and seeking more efficient experiences from product sourcing through to checkout. With B2B eCommerce proliferating, the market is rapidly evolving to make way for new business and payment models in response to customer demand. Tying Payments With Loyalty.

Online account opening remains the wild west for most community banks. And naturally I was keenly interested in how to solve this problem, or even diagnose what exactly is the problem, for community banks and online deposit account opening, either retail or business. In so many strategy sessions, I hear from bankers that it is a bust.

The 2020 holiday shopping season is picking up, and consumers are heading online or to reopened brick-and-mortar stores to shop and pay for gifts. They are using everything from cash to mobile wallets to complete these transactions, requiring retailers to race to accommodate a wide variety of payment methods.

Popular use cases include request for payments using the instant payment rails (above), loan payments and transaction verification to prevent fraud. Secure Authentication: RCS offers stronger security features compared to SMS, making it a viable option for two-factor authentication and other bank security measures.

While video streaming services remain popular, research indicates more consumers are also turning to online gaming and gambling platforms. The Tracker also examines how both fraudsters and online gaming platforms are employing new emerging technologies to muscle bad actors out of these services. Skillz Takes Offline Bowling Online.

Square is offering merchants in the beauty and wellness industry a point of sale (POS) tool that integrates appointments, payments and checkout for a streamlined, secure process. . Square Appointments is a front desk solution that works with the business payments processing tool Square Register.

Tim Horton , head of global merchant security and fraud solutions at Fiserv , told a recent PYMNTS Masterclass that online purchases have more than doubled year on year in the general retail segment, while online grocery sales have surged by 250 percent. But put the same consumer online and the story is very different.

As cyber attackers develop more sophisticated methods of attacking online sites, security experts and retailers are increasingly focused on protecting mobile shopping and payment platforms to ensure a safe holiday season.

A new Mastercard initiative aims to improve online transaction clarity so that customers can know exactly who they purchased from, according to a press release Tuesday (Sept. This can lead to consumers contacting their banks, which could incur costs and waste time with unnecessary chargebacks.

TSYS , a payment processing company, has suffered a ransomware attack and had some data posted online, according to a report from Krebs on Security. based TSYS, the third-largest third-party payment processor for financial institutions in the U.S., The company was acquired by Global Payments Inc. Columbus, Ga.-based

Building a secure customer journey is always a bit of a balancing act. It has to be secure first and foremost, particularly when payments data is on the line. If you look at the customer journey from end to end, the fraud starts not just around payments. Winning The New War With Account Takeover.

While credit is an important part of millennials’ shopping lives, this generation has unique spending priorities, particularly when it comes to online shopping — and these priorities are looming even larger since the pandemic shifted much of commerce online. consumers, that were conducted in March and September.

Atlanta payments encryption firm Bluefin is partnering with New York mobile payments processor PAAY to advance eCommerce security. Most online merchants rely solely on SSL/TLS to encrypt the data being sent from their websites. This leaves payment data vulnerable while inside the web page before it is transmitted.

COVID-19 has shifted consumers away from card-based payments experiences, while P2P has accelerated a change enabling merchants to own the payments experience itself, Debbie Guerra , executive vice president of merchant and payments intelligence solutions at ACI , told PYMNTS in a recent interview. Payments Flexibility .

When it comes to B2B payments fraud, it’s not a matter of if it happens, but when. While eliminating paper is a much-needed first step to combatting B2B payments fraud, electronic payments aren’t immune to the risk, either. Fraud Captures Faster Payments Council Attention. ” $4.13 ” $4.13

Waze, the popular GPS navigation app owned by Google, has introduced contactless payments for ExxonMobil and Shell card holders in the U.S. When drivers pull into participating stations, they will see a notification on Waze prompting their Android or iOS device to securely pay through each company’s app.

The IoT [ Internet of Things ] digital explosion is changing everything that happens around us,” Mastercard Executive Vice President of Security and Cyber Innovation Johan Gerber noted in a recent conversation with Karen Webster. Security is a big deal because vulnerabilities no one has ever even thought of will pop up.

Visa saw more growth in payments in November, including a 27 percent spike in onlinepayments, a filing from the Securities and Exchange Commission (SEC) stated. Meanwhile, declines could be seen for credit payments and in-person payments, the filing stated, while growth in spend by merchant categories fell from October.

Brazil’s Central Bank has suspended WhatsApp’s payment feature in the country, citing antitrust concerns, according to Bloomberg on Tuesday (June 23). Mastercard and Visa have been requested to stop payments and money transfer services through the app in Brazil as well, the bank said.

The shift to digital commerce means that long after the pandemic is over, merchants across all verticals will have to offer a range of payment choices in order to boost conversion rates. As PYMNTS research has detailed, as much as $158 billion in brick-and-mortar commerce will move online.

Artificial intelligence (AI) can improve the eCommerce experience – not just in terms of warding off fraud, but also in making sure payments can be processed efficiently and that the most effective payment gateways are accessed. Consider the fact that just a few years ago, alternative payment rails Zelle and Venmo didn’t even exist.

Real-time payments are imperative for running successful operations in today’s global ecosystem. Digital payments sent internationally are expected to move past $1 trillion in 2025, but getting to that point will require support from payment providers, regulators and other such firms still building out the necessary infrastructure.

Higher volumes of consumers are continuing to shop online even as brick-and-mortar stores reopen. The expansion of digital banking and payments has also contributed to a rise in cybercrime — 32 percent of consumers noted in one study that they had been the targets of COVID-19-related fraud, for example.

Real-time payments continue to gain traction around the world. The country’s banking system is giving an upgrade to its instant payments system. Called PIX , the new payment rails have been in the works for some time and launched last week. Case in point: Brazil. It will be fully operational starting Monday (Nov.

The database works with other payment processors, verifying payments to make sure there is no fraud going on for outside vendors. A security researcher, Anurag Sen, accessed the files and estimated around 2.5 Paay is not alone in the pool of companies that have seen security lapses even this year so far, with two U.S.-based

The pandemic has exposed the pain points of all verticals when it comes to payments, and especially when it comes to transacting in person, in a tactile environment, with cash, and where banking conduits are limited. Those benefits can extend to users in the form of cost savings tied to payments and processing, or speedier processing times.

As virtual marketplaces displace (and replace) the physical variety at a dizzying pace, payments speed and security are paramount concerns. When transactions and payments occur cross-border, those concerns are doubled. As actual marketplaces are plagued by pickpockets, so online marketplaces have their own crooks.

Buy now, pay later (BNPL) is a type of point-of-sale installment loan that partners with retailers to allow consumers to pay for their purchases in multiple equal payments. which is a huge draw to using BNPL as a non-cash payment method. What Are Some Buy Now, Pay Later Companies? Which one is best for me?

Accelerating The Real-Time Payments Demand Curve: What Banks Need To Know About What Consumers Want And Need. This study showed that consumers display significant interest in real-time payments once they fully understand them. percent of millennials believe it is “very” important to receive payments in real time. percent and 20.3

The pandemic has drastically affected how consumers are shopping and paying for even routine purchases, and this in turn has altered how businesses are accepting their payments. The health crisis has brought about changes to this rule, however, and these may have long-term implications for payment standards and regulations.

Only 26 percent of all consumer payments are made in the U.S. Beyond the wholesale shift to digital payments, Cole told PYMNTS in a recent interview, there are pockets of growth that are seeing more digital acceleration than others as lockdowns linger and businesses reopen on a staggered basis. The Demographics .

And where consumers go, businesses are following — including companies that have never (or barely) transacted online before, and those that have but never at the scale they are currently being called to provide. Retailers, merchants are realizing they can actively utilize those channels because for a lot of them it’s survival.

India has seen a steady stream of digital payments since it locked down to prevent the spread of COVID-19 , but the nation of 1.3 billion suffers from either a lack of internet or low-speed service, preventing many residents from taking part in touchless payments. Four years ago, India launched its Unified Payments Interface (UPI).

As has historically been the case with commerce security upgrades that roll in by government mandate, the path to European Union adoption of 3D Secure 2.0 That’s a path that McCutcheon said will have challenges, but perhaps fewer than we’ve seen in the recent history of security upgrades. also known as “3DS 2.0” Why 3DS 2.0

Stripe is acquiring Paystack , a company that says it processes more than half of onlinepayments in Nigeria. More than 60,000 businesses in Nigeria and Ghana use Paystack to securely collect online and offline payments, launch new business models, and deepen customer relationships.

23) that they have entered a strategic partnership to launch Visa Commercial Pay, billed as a suite of B2B payment solutions for enterprises making the shift to digital transactions, and, specifically, virtual cards — and away from paper-based manual processes. The shift to digital payments has been gaining momentum.

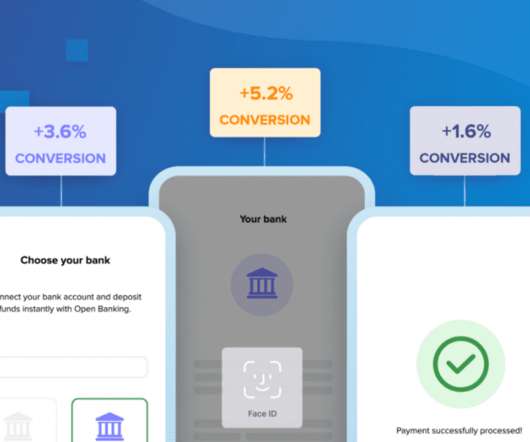

Offering Digital Consumer and Commercial Accounts Benefits Financial Institutions Banks and credit unions that enable online/digital account opening win new customers and members and retain existing ones. . Takeaway 1 Many financial institutions are adding or improving online or digital account opening capabilities. .

With the increasingly high numbers of online shoppers in the wake of COVID-19 , we are committed to providing solutions that lay the groundwork for the next generation of simple, secure and better ways to pay,” Stacey Madge , president and country manager of Visa Canada, said in the announcement. 15) announcement.

Payments technology startup Shift4 Payments has acquired eCommerce firm 3dcart to create a global, “unified commerce ecosystem,” the company announced in a Thursday (Nov. Shift4 Payments services businesses with its suite of multichannel payment products. “We 5) press release. “We

That’s because paper becomes the default method of payment when something goes awry — such as when banking credentials can’t be authenticated or identity cannot be verified. The payments ecosystem, of course, is not and will not be immune to the seismic impact and aftershocks of the coronavirus. “The According to J.P.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content