This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Recommended Approach : GenAI can assist various payment processes by creating personalized and tailored payment experiences through loyalty programs, discounts, and curated product recommendations. Additionally, AI can enhance accessibility and mobile development through voice and conversational payments, improving userexperience.

Intimidated by the scale and cost of a massive technological overhaul, large financial institutions (FIs) may approach their digital transformation (DX) journeys gradually, targeting various areas of operations to modernize one-by-one. “Banks are technology companies,” Rio Tinto recently told PYMNTS. Preparing For The Future.

Or that, on average, 15 percent of an FI’s annual operating costs go toward maintaining core banking systems that are outmoded? From global customer acquisition efforts to real-time personalization of the userexperience to infrastructure technology management, the opportunities are endless.”. It’s true, but not for long.

According to an August study of digital banking by PYMNTS, banks are closing physical branches, reducing hours of operation and encouraging customers to use their websites or mobile apps to conduct transactions and reduce face-to-face interactions between customers and staff. On Monday (Oct. 5) NCR Corp.

Whether you are B2B, B2C, or a strategic blend of the two operating models, your consumers expect seamless userexperiences powered by custom technology solutions. Nearshore software delivery regions boast convenient geographic proximity and time zone alignment to the U.S. The digital world is global, now, more than ever.

The benefits of taking a digital-first approach to banking go beyond offering an improved in-person banking experience. It is also crucial to improving back-office operations, and enabling bank employees to put the right products in front of the right customers.

As Davis noted, larger banks, including regional players, tend to have their own technology platforms — and direct integrations into their own networks — to enable mobile and contactless payments. They are not always fast followers of newly introduced products and services from their larger banking brethren who operate on a national scale.

For instance, the ability to transfer data and various assets can help firms keep track of, and improve, operations. Yet, corporate finance especially is “operating, more or less, the same [way] it has for 20 years prior. Much of the operations are limited by the time zone/region and cutoff times for various markets,” he said.

In a press release, Grab said the launch of the remittance offering marks a “significant milestone” toward the company’s vision for on ASEAN eWallet that will improve financial inclusion for the growing middle class and micro-entrepreneurs in the region. Grab made the announcement during the 33rd ASEAN Summit.

For other companies, GDPR is the main concern as they move to expand operations within Europe. Social media giant Facebook is facing yet another batch of complaints around its practices in the region, with more claimants asserting it is not meeting GPDR requirements under the law.

It is reportedly keeping an eye on the virus situation throughout different regions to ensure that it is safe to operate its stores. The tech company operates 510 stores throughout the world, per news at the time. .” On May 27, news surfaced that Apple was looking to open approximately 100 U.S.

Its Getaround Connect device now operates in the United States, as well as in seven European countries: Norway, France, Germany, Spain, Austria, Belgium and the U.K. In April, Getaround announced its acquisition of Drivy , a Paris-headquartered car sharing startup that operates in 170 European cities.

Particularly amid the continuing uncertainty surrounding Brexit, FinTechs are turning to Lithuania to retain their European footholds and operate in a country that supports their innovative ambitions. SatchelPay announced last week that the central bank has given the company the green light to resume operations.) Resuming Operations.

However, in the case of visual and image-based authentication processes, Trulioo Chief Operating Officer Zac Cohen told PYMNTS, the emerging picture is a bit cloudier. Onboarding processes, as well as identity verification and authentication processes, are not homogenous vertical to vertical or region to region, he noted.

Founded in 2015, Nabobil has built a strong user base in Norway. The acquisition will boost growth, and improve the userexperience in the Nordic region through the integration of Getaround’s connected car technology.

But the bitcoin and blockchain technology is only used as the interoperability layer of the social payment platform, which means it only comes into play if funds are being exchanged with a digital wallet in a market where Circle does not operate. “Our vision doesn’t end just with social payments.

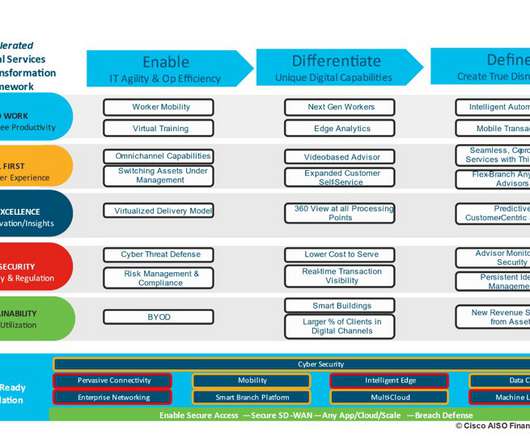

It’s an excellent way to solidify the optimal operating model mix for hybrid work, digital first engagement, operational excellence and process automation, sustainability, and cybersecurity. Also, it creates an opportunity to unite internal stakeholders all across the C-suite to different lines of business.

Consumers around the globe have moved their purchasing online during the pandemic, and those in the Middle East and North Africa (MENA) region are no exception. The region’s financial institutions (FIs) and merchants have needed to work swiftly to support unprecedented levels of digital payment and shopping growth.

IP recognition technology is just one of many features merchants can employ to help streamline the cross-border payment experience for their visitors, however — and not all of these features are equally effective when it comes to enhancing their userexperience (UX).

We will be working with Qupital to further utilize the technologies to enhance risk management, userexperience and operational efficiency”. “We look forward to working with Qupital to broaden its source of capital base and create unparalleled investment opportunities for CreditEase.

Even so, the model can be a bit more challenging for operators: They have to concern themselves with ensuring that the vehicles stay within the rental zone and are parked in locations that are legal as well as appropriate. Nabobil, which was started in 2015, has built a strong Norwegian user base.

When it comes to expanding operations internationally, making payments to sellers and vendors is often an uphill battle for cross-border marketplaces. Companies need to partner with acquiring banks and a host of other vendors in the region, in addition to setting up a treasury operation for managing risk and keeping the business afloat.

FIs and FinTechs are busy agreeing on standards for digital-only operations, and as things are tightened up on the back end, front end userexperience is the promised land of personalization. “As Banks and credit unions collect an enormous amount of data for each of their users. APIs Accelerate Digital-First Adoption.

For businesses that operate within the payments ecosystem, playing the long game also means, on occasion, retooling — proactively. focused direct-to-consumer (DTC) operations tied to Whitepages.com. He noted, too, that the businesses, including the B2B operations, had traditionally been funded by the DTC side of the firm.

Things aren’t so straightforward for those who create those innovations — which, as NovoPayment CEO Anabel Pérez told Karen Webster in a recent conversation, is a challenge for many banks in the Latin America (LATAM) region to fully grasp. That’s how a bank goes about offering a digital experience that isn’t just beautiful (i.e.,

Dubai, UAE – April 13, 2022 – Finastra today announced that Banque Misr, the second largest national bank in Egypt with international presence, has selected Fusion Trade Innovation and Fusion Corporate Channels to digitalize its trade finance services and provide a premium userexperience.

Emailage , the online fraud prevention startup that uses email addresses to assess risk, is expanding its operations in the Canadian market. Startups are nimble and quick to react, and as they reach a critical mass, they see companies like Emailage as a crucial element to their experience. Emailage can serve various verticals.

Nonetheless, it’s a clear statement that when friction is removed from the userexperience, people respond.”. Telemedicine services like Doctor on Demand — which now operates in 50 states — connect patients with physicians, psychiatrists and mental health workers entirely across digital channels. 5G Healthcare.

Uber, after all, may have dozens of people staffing the payments side of the operations, but smaller firms simply do not have comparable resources. SaaS firms, he said, tend to follow a pattern as they leverage data (with insight into regional or local payment preferences) to expand beyond the U.S.,

Looking at the regional breakdown, the U.S. Other regions notched only single-digit percentage rates. Additionally, the volume of SDKs required to effectively attribute mobile app marketing efforts occasionally caused slowdowns in userexperiences. held sway with 83 percent of the investments for the week.

What happens when a thriving on-demand marketplace operating in one country wants to expand into new international markets? Hyperwallet, for example, tends to see marketplaces start up in regions where the population is heavily banked. To these workers, said Ting, “the pinnacle of the userexperience is getting paid.

Its Getaround Connect device now operates in the United States, as well as in seven European countries: Norway, France, Germany, Spain, Austria, Belgium and the U.K. In April, Getaround announced its acquisition of Drivy , a Paris-headquartered car sharing startup that operates in 170 European cities. That’s hardly all.

Its Getaround Connect device now operates in the United States, as well as in seven European countries: Norway, France, Germany, Spain, Austria, Belgium and the U.K. In April, Getaround announced its acquisition of Drivy , a Paris-headquartered car-sharing startup that operates in 170 European cities. That’s hardly all.

The complexity of mobile payments shows up when looking at the entities involved in the entire process, and where these entities will be operating. The regional variations of the payment flow make for a massive amount of complexity in the ecosystem as there are also regulatory and compliance guidelines that will shift depending on the region.

As the open banking business model permeates into the B2B financial services market, FinTechs and traditional financial institutions continue to find new use cases for API integrations and connectivity to elevate the business-userexperience. Eika Group, EedenBull Team for Banks.

It’s exciting to see how Cisco is building the most powerful, innovative, and secure operational platform to enable enterprises, including those in highly regulated industries like financial services, to move confidently to the cloud. If branches are currently closed in your region, they will be opening back up.

This week we welcome Marc Gilman , General Counsel and VP of Compliance at Theta Lake for a Q&A on a key topic for compliance, operational risk, and security leaders – ensuring that robust controls are in place for regulatory, cybersecurity, and privacy of collaboration platforms.

The Libra Association was created specifically to demonstrate that the network will operate separately from Facebook. . “We A lot of it comes down to the infrastructure that is available [and] the userexperience being designed for men, rather than women,” Jones said.

No word has been given on the anticipated release dates for future expansions to other world regions. Along with Google Voice, there’s Google Hangouts, which can be used across a number of smartphone and desktop operating systems. Pre-orders began on Jan. 16 with a targeted delivery date in mid-February, the company said.

While there is still some way to go for banks in SE Asia when it comes to utilizing real-time digital identity capture and verification, they are out in front of some other regions. Many types of account openings still rely on verifying identity separately through physical challenges. www.fico.com/identity. by Subhashish Bose.

And the platform, operating in California and Texas, could inevitably become more convenient and affordable than car ownership. “I ” But even if Americans are slow to adopt this convenient, affordable, and personalized experience, other regions may do so out of necessity. I don’t rent a car anymore,” he disclosed.

These startups “challenge” the traditional incumbent business model by charging customers transparent low fees, providing faster services, and delivering a better userexperience through always-available digital interfaces. Branch operating costs (OPEX) now exceed the revenue they generate.

The innovative pay-as-you-go solution allows Dock’s clients, including banks, fintechs, and retailers, to intercept fraudulent transactions and protect their operations, while also improving the userexperience. The fraud prevention solution is based on FICO® Falcon® Fraud Manager and FICO® Customer Communication Services (CCS).

In 2014, I joined Tonbeller as Head of Sales & Channel Operations and became Management Board member shortly thereafter. It is the culture that ensures that employees operate within the prescribed risk appetite and limits and conduct in a way that will neither cause damage to the client nor the institution’s reputation.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content