This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Big data, mobility, socialmedia and cloud computing are changing the way people live, work and think – and forcing banks to develop new strategies to meet ever-shifting customer expectations. New, powerful digital innovations and operating models can also drive a bank’s efficiency to higher, more profitable levels.

Viacom Media Networks. Wharton FinTech , the first student led FinTech initiative, has published two whitepapers on Millennials’ relationship with banks ( June 2015 and May 2016 ). Banking apps should operate seamlessly, design should be attractive and security should be a given. Prioritizing key life moments.

Big data, mobility, socialmedia and cloud computing are changing the way people live, work and think – and forcing banks to develop new strategies to meet ever-shifting customer expectations. New, powerful digital innovations and operating models can also drive a bank’s efficiency to higher, more profitable levels.

Big data, mobility, socialmedia and cloud computing are changing the way people live, work and think – and forcing banks to develop new strategies to meet ever-shifting customer expectations. New, powerful digital innovations and operating models can also drive a bank’s efficiency to higher, more profitable levels.

Big data, mobility, socialmedia and cloud computing are changing the way people live, work and think – and forcing banks to develop new strategies to meet ever-shifting customer expectations. New, powerful digital innovations and operating models can also drive a bank’s efficiency to higher, more profitable levels.

That’s easy to see as 2017 had its share of scandals and mishaps ranging from socialmedia blunders to poorly planned advertising spots, as well as a host of poorly executed responses to the many natural disasters that occurred last year. In today’s fast-paced, business environment, it’s not if a company will face a crisis, it’s when.

Increasingly in today’s age, terrorist organizations and dangerous criminals finance their operations by laundering money in global financial institutions, presenting a huge public policy problem for regulators and policymakers. For more information, see our whitepaper on Advancing AML Compliance with Artificial Intelligence.

He explains that his team operates with a data-oriented mentality. From public relations and trade shows to webinars or whitepapers – each member has an eye on the results of what gets created, how it quantifiably impacts the company and what type of qualified feedback is received along the way.”. Socialmedia.

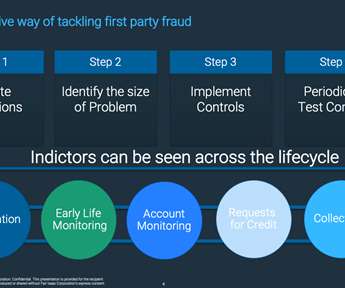

This tricky and often very large problem can be easily missed as it lurks somewhere between the risk department, operations and the fraud team; in other words, first-party fraud frequently does not have a direct owner. Siloed fraud and collections departments further reduce the chance for fraudulent patterns to be discovered. Matt Cox.

This tricky and often very large problem can be easily missed as it lurks somewhere between the risk department, operations and the fraud team; in other words, first-party fraud frequently does not have a direct owner. Siloed fraud and collections departments further reduce the chance for fraudulent patterns to be discovered. by Matt Cox.

Mobile Operators and Coronavirus: Ideas To Help Slow The Spread. Mel Prescott noted several ways that mobile operators could use their network data to potentially help fight the virus. For more information on this topic, read our whitepaper on Agile Decisioning in an Unprecedented Downturn. #5.

Download our latest whitepaper that discusses what it really takes to develop a successful Fintech startup. Silver 6 operates as Software as a Service (SaaS), so that means no IT and no infrastructure required. ^SR. She manages all digital and socialmedia efforts on behalf of agency clients. This is great.

Diana Chin (HR & Operations). The account has a tie into socialmedia and sharing. This is the integration of mobile socialmedia with trading. Download our latest whitepaper that discusses what it really takes to develop a successful Fintech startup. Virtual reality? Richard Ting (Sales and Bus.

Socialmedia is a special challenge since socialmedia was not created with compliance in mind. I can see how some other socialmedia channels may be more prevalent and important in the U.S. Juvo makes it easy for mobile operators to find them. They record automatically on digital channels.

operation of Russian-based company. Product Development and Operations are headed by Anu Shultes who is a well-known and highly respected gift card industry expert. From their web site: Modo provides a COIN® operated Digital Payments Hub that connects new digital experiences to payments systems worldwide. I think they do.

Note for you damn haters: yes, it’s down from a frothy high of $66,0000, but look at the normalized return over the past 15 years since Satoshi Nakamoto’s whitepaper.) The Holy Crap Operational Risk Award – goes to the growing threat of ransomware with bank technology vendors. The poor payroll and benefits coordinator!

Sustained low interest rates and the ongoing operational costs – in particular the cost of compliance – are compressing profit margins. At the highest level, it allows banks to switch from tactical cost-cutting to begin operating at what I like to call a strategically lower cost. And it’s a much needed influx of innovation.

With revenues challenged, many banks have been focusing on operational efficiencies to drive financial performance. Banks continue to simplify operations, strive for scale, and right-size their branch structure. To wit, we believe that further cost efficiencies will be difficult to attain from existing operating models.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content