This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Avanti Financial Group said in a press release that it has received permission from the Wyoming Division of Banking to begin operating in the state as a bank as early as October and plans to offer a real-time settlement solution for corporate treasurers. Avanti made its Wyoming intentions clear in February.

Earlier this year, Wyoming became the second state to create a financial technology (fintech) sandbox by enacting the “ Financial Technology Sandbox Act ” (Sandbox Act). The provisions requiring Wyoming’s Banking Commissioner and Secretary of State to adopt implementing regulations became effective on February 19, 2019.

Government Accountability Office (GAO) said that financial regulators should look more closely at the role of non-bank tech companies in the small business (SMB) lending and consumer lending markets. Closer to home, in Wyoming, a bill has debuted in the state legislature to create a FinTech sandbox. Late last week, the U.S.

The Commodity Futures Trading Commission ( CFTC ), Federal Deposit Insurance Corporation ( FDIC ), Office of the Comptroller of the Currency ( OCC ), and the Securities and Exchange Commission ( SEC ) have announced that they are joining the Global Financial Innovation Network ( GFIN ). Colorado’s bill does have support from some lawmakers.

The price of the marquee name in cryptocurrencies dipped as low as $9,450 in intraday trading when the Securities and Exchange Commission (SEC) announced there were “potentially unlawful” systems operating that allow the trading of cryptocurrencies. As a result, digital currencies can be regulated by the U.S. As of 7:48 p.m.,

Indian regulation requires all payments data be processed in-nation — instead of on Facebook’s servers. Warby Parker additionally reported it will continue investing in technology that will continue to protect customers’ privacy and security when using the site. Whole Foods’ Expanding Footprint.

ICBA also is pressing regulators to use their oversight discretion to exempt community banks without legislation. Kim DeVore, chief financial officer for Jonah Bank of Wyoming, in Casper, Wyo., There are a lot of opportunities we are essentially prohibited from offering because of regulation,” Zaback says. “So

This generated a good $6 billion of revenue in 2016, though that number is likely further compressed given attempts at regulating this sector. It doesn’t have an ILC charter from Utah, or a crypto bank charter from Wyoming, or a straight-up bank charter like Varo, nor has it acquired any banks like Lending Club or Jiko. No shenanigans.

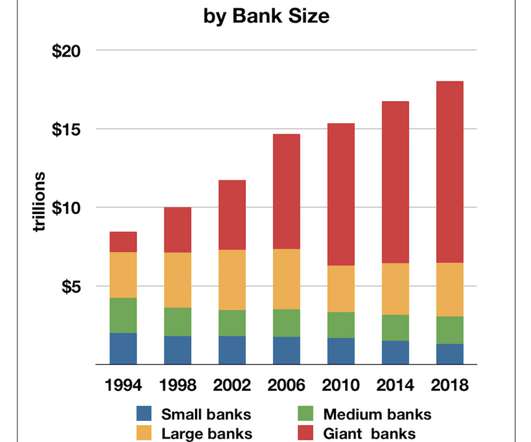

Instead, they have either (1) been directly owned by retail investors through crypto exchanges or decentralized apps, or (2) been packaged and secured for safe handling by newly buy-side funds for the largest endowments and family offices in the world. Assets at the giant, federally regulated banks like Citi and JP Morgan, are ballooning.

Instead, they have either (1) been directly owned by retail investors through crypto exchanges or decentralized apps, or (2) been packaged and secured for safe handling by newly buy-side funds for the largest endowments and family offices in the world. Assets at the giant, federally regulated banks like Citi and JP Morgan, are ballooning.

Drug Supply Chain Security Act requirements will help us do just that.”. In other news, Wyoming — America’s least-populous state — has turned its focus on blockchain, attracting a slew of new businesses as a result. However, while these companies might be legally based in Wyoming, most aren’t located in the state.

Cryptocurrency regulation is on the horizon The ups and downs of the cryptocurrency scene have illuminated a need for guidance for traditional financial institutions. Takeaway 1 Cryptocurrency has been able to offer good interest rates on high-yield savings accounts and secured loans with no credit check. . DOWNLOAD WHITEPAPER.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content