This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Risk brings rewards. Riskmanagement professionals are comfortable with ideas about growth curves and early versus late investment. Riskmanagement demands a lot of data from many different sources, and traditional database management systems are too slow for the granular analytics needed today.

Riskmanagement is complex territory for many businesses, especially those with complex partnerships, vast supply chains and global footprints. For fund investors, active riskmanagement is of particular importance for treasurers, Hazeltree noted.

Explore these ideas in more depth in the IBM whitepaper A new era of technology-enabled financial riskmanagement. Also see our related blog post, A new era of technology enabled financial riskmanagement. Learn more about IBM regulatory technology at ibm.com/RegTech.

Topics will include riskmanagement and strategic planning, financial inclusion, consumer protection, supervisory expectations, and regulatory concerns. In March 2016, the OCC released a whitepaper: “Supporting Responsible Innovation in the Federal Banking System: An OCC Perspective.” Registration is free.

The rule change is the subject of a recent whitepaper published by GIACT. The purpose of the new rule, according to NACHA , is to “enhance quality and improve riskmanagement within the ACH network by supplementing the fraud detection standard for internet-initiated (WEB) debits.”. New NACHA Rule.

The firm’s latest movement in real-time fraud analysis comes as the company also offers insight, via a whitepaper, into “10 Fraud Myths” commonly held by risk professionals. The new offering is built into the Sift Science Digital Trust Platform. In other words, historical data, cogently presented, makes all the difference.

Recently, IDC published a whitepaper, sponsored by IBM, outlining the ten hard realities that FIs and payments services providers must overcome to benefit from modernization, and how they can turn these perceived threats into opportunities. With this change comes new business opportunities. Payments modernization has arrived.

Riskmanagement, compliance and security : incorporating enterprise riskmanagement is already a key concern and it will only grow more important. Analytics : applying predictive analytics based on big data and cognitive computing, in particular, will enable banks to deepen and scale workforce capabilities.

We’ve been quite vocal about our own transition to a riskmanagement microservices architecture. To enhance the user experience of each of these services, a separate microservice was built to manage financial data to remove the often heavy burden of doing so. Our experience with microservices. Don’t have data?

“Clarification and harmonization of regulation are fundamental to mitigating the serious threat that de-risking poses to the financial system,” ICC Director of Finance for Development Olivier Paul said in a statement.

Recently, IDC published a whitepaper, sponsored by IBM, outlining the ten hard realities that FIs and payments services providers must overcome to benefit from modernization, and how they can turn these perceived threats into opportunities. With this change comes new business opportunities. Payments modernization has arrived.

Analysis of FICO® Resilience Index data by Tom Parrent, former chief risk officer for Genworth Financial, shows that from 2010 to 2015, nearly 600,000 additional mortgages could have been originated to consumers with FICO® Scores between 680 and 699, had the FICO® Resilience Index been available to lenders at the time.

We’ve been quite vocal about our own transition to a riskmanagement microservices architecture. To enhance the user experience of each of these services, a separate microservice was built to manage financial data to remove the often heavy burden of doing so. Our experience with microservices. Don’t have data?

The FICO® Score 10 suite provides lenders with market-leading riskmanagement capabilities for a wide variety of business applications, with more flexibility than ever before. The FICO® Score 10 suite supports more predictive consumer credit riskmanagement. Conclusion. by David Binder.

A whitepaper released Thursday said the agency might issue new guidance on fintech product development, third-party riskmanagement and new products targeting the underbanked; streamline its licensing procedures; and appoint experts on "responsible innovation."

Riskmanagement, compliance and security : incorporating enterprise riskmanagement is already a key concern and it will only grow more important. Analytics : applying predictive analytics based on big data and cognitive computing, in particular, will enable banks to deepen and scale workforce capabilities.

For more information on this topic, see our whitepaper on Advancing AML Compliance with Artificial Intelligence. This episode of Tomorrow’s World Today also included an interview with Gordon Cameron, EVP of Independent RiskManagement at PNC, which uses the AI in FICO Falcon Fraud Manager to protect its customers.

Riskmanagement, compliance and security : incorporating enterprise riskmanagement is already a key concern and it will only grow more important. Analytics : applying predictive analytics based on big data and cognitive computing, in particular, will enable banks to deepen and scale workforce capabilities.

Riskmanagement, compliance and security : incorporating enterprise riskmanagement is already a key concern and it will only grow more important. Analytics : applying predictive analytics based on big data and cognitive computing, in particular, will enable banks to deepen and scale workforce capabilities.

Along with our partners Equifax, we launched a product to address the combined issue of credit and affordability risk , initially in the UK market. This product stems from extensive research into affordability risk, summarized in a recent whitepaper written by my colleague, Dr. Andrew Jennings.

For more information on this topic, see our whitepaper on Advancing AML Compliance with Artificial Intelligence. This episode of Tomorrow’s World Today also included an interview with Gordon Cameron, EVP of Independent RiskManagement at PNC, which uses the AI in FICO Falcon Fraud Manager to protect its customers.

The references are vague, however: “centralized fraud and riskmanagement capabilities” are referenced but the nature of this protection is not defined. The ‘ Modernization Target State’ lays out Payments Canada’s vision for the future and it does talk about fraud prevention. The post Will Real-Time Rails in Canada Bring More Fraud?

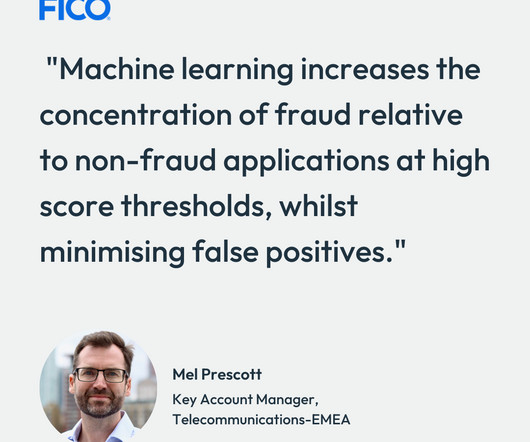

Read our whitepaper on Fraud in the Digital Experience Era – Telecommunications. Mel has held credit riskmanagement positions at EE, Orange and Bank of America. He holds an MSc in Analytical Credit RiskManagement from Sheffield Hallam University.

Rather than weakening our riskmanagement measures, the more impactful goal for the industry is to find ways to help consumers improve their financial picture through legitimate credit counseling so that they qualify for a mortgage. Read our whitepaper Can Alternative Data Expand Credit Access?

Sally notes that analysis of FICO® Resilience Index data by Tom Parrent, former chief risk officer for Genworth Financial, shows that from 2010 to 2015, nearly 600,000 additional mortgages could have been originated to consumers with FICO® Scores between 680 and 699, had the FICO® Resilience Index been available to lenders at the time.

Note for you damn haters: yes, it’s down from a frothy high of $66,0000, but look at the normalized return over the past 15 years since Satoshi Nakamoto’s whitepaper.) The Holy Crap Operational Risk Award – goes to the growing threat of ransomware with bank technology vendors.

In 2015, our industry woke up to changes in payments, delivery, marketing and riskmanagement that are more serious than the typical conference chatter. Take this brief survey (5-7 minutes) and receive: “Insights into 2016,” a free whitepaper with study results and recommendations for 2016.

Riskmanagement for cryptocurrencies, including addressing indirect risk faced by clients’ crypto activities and evolving global regulatory considerations. Read FICO’s Crypto AML WhitePaper. The opportunity landscape for traditional banks and financial institutions to offer new and enhanced services .

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content